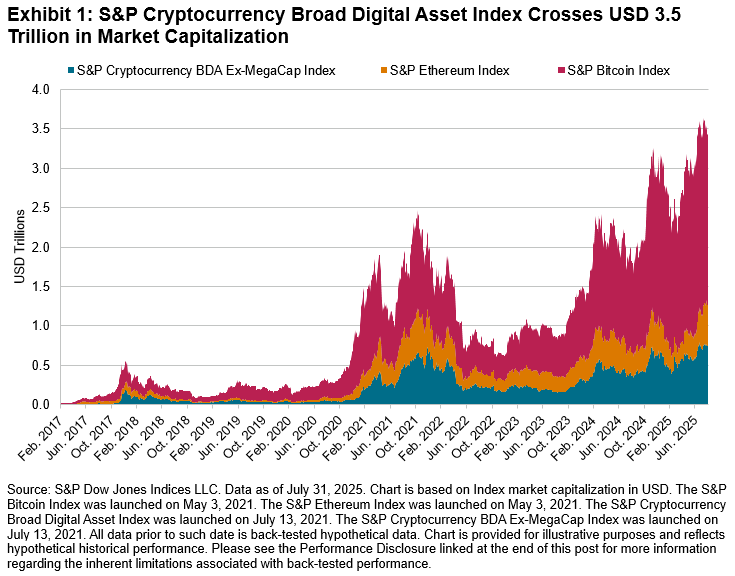

Two decades ago, crypto didn’t exist, and even a decade ago, it was still an emergent asset class. In the last few years, crypto has increased in maturity, crossing USD 1 trillion in market capitalization in 2021 and currently sitting at USD 3.5 trillion at the end of July 2025 based on the S&P Cryptocurrency Broad Digital Asset (BDA) Index. Its increased size is not the only indicator of its increasing maturity; market participants have been offered additional tools to help in their asset allocation decisions with a growing network of associated exchange-traded products, such as futures, options, ETFs and other wrappers. The crypto product ecosystem is expected to continue growing, with a robust pipeline of ETF filings globally. In addition, a shift in the global regulatory landscape for DeFi-related products is helping to create a framework for market participants in this asset class.

Crypto ETF filings followed a similar path as the underlying cryptocurrencies, with Bitcoin (BTC) and Ethereum (ETH) representing the first spot ETF filings. Bitcoin launched in 2009 as the first cryptocurrency and Ethereum launched in 2015, ushering in a second wave of crypto innovation introducing smart contracts and decentralized apps. It is not surprising that early ETF filings across various regions followed the same path, shown in Exhibit 2. In 2025, there is a growing list of single coin ETPs on a multitude of other coins outside of the mega-caps of BTC and ETH (S&P Cryptocurrency MegaCap Index) with other large-cap coins like Solana and Cardano (which are included in the S&P Cryptocurrency LargeCap Index) expected to have their own ETFs in the U.S., and XRP being recently approved in the U.S.. Recent changes to Crypto ETP SEC Filing guidelines on Sept. 17, 2025, may potentially pave the way for more crypto spot ETFs according to Reuters.

Looking further into ETF data in Exhibit 3, according to ETFGI,1 there were only two digital asset ETPs in 2015, but there are now over 300 products as of July 2025, with a collective AUM of 220 USD billion, a figure that was only at 3 USD billion in 2020. This exponential rate of growth shows the heightened demand for crypto-related products.

Over the past two years, it’s not just the number, but the variety of crypto-focused ETFs that has expanded dramatically. While single-coin ETF products based on Bitcoin and Ethereum led the adoption of cryptocurrency, we are also starting to see multi-coin, diversified “crypto basket” products looking at the top 5 and 10 largest crypto assets. The start of non-market-cap-weighted products and capping on the largest coins like Bitcoin and Ethereum has also been a recent trend, with indices and products applying principles of diversification from traditional finance. Crypto is also being increasingly thought of as a diversifier in asset allocation decisions with the launch of more multi-asset strategies that combine crypto with traditional asset classes such as equities and commodities.

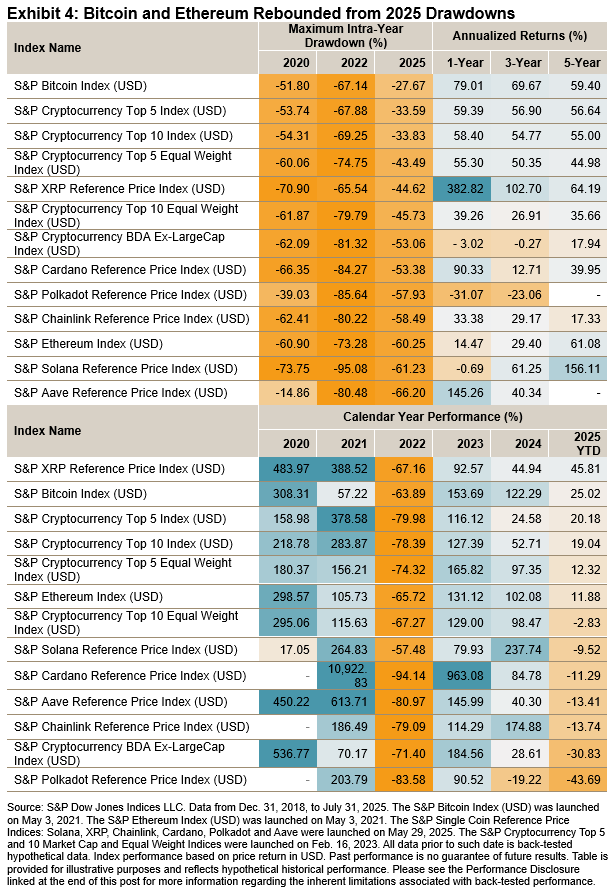

However, the journey to get there hasn’t been smooth. The resilience of the AUM growth is even more impressive against the backdrop of the crypto drawdowns at the start of 2025, which was marred by uncertainty and risk-off undertones due to geopolitical tension, tariffs and concerns around whether U.S. exceptionalism would hold. At the end of March, the S&P GSCI Gold was in positive territory, sporting a return of 18%, whereas the S&P Bitcoin Index, S&P Cryptocurrency MegaCap Index and S&P Ethereum Index were down 12%, 18% and 45%, respectively, in Q1 2025 and had an even more severe drawdown compared to their peak.

Despite this market turbulence, the largest cryptocurrencies have shown resilience, with Bitcoin and Ethereum nearing all-time highs as of July 2025. However, there remains some underperformance, with smaller coins still lagging.

While crypto remains a highly volatile asset class, its increased institutional adoption is expected to continue, with highly anticipated regulatory milestones expected to be a key part of shaping crypto for years to come. Regulatory developments, like the GENIUS Act and Clarity Act in the U.S. and MiCA in Europe, as well as expected changes in APAC adoption, could be determinants of where crypto goes next.

1“ETFGI reports Crypto ETFs listed globally gathered 3.69 billion US dollars of net inflows in April.” ETFGI. May 30, 2025.

The posts on this blog are opinions, not advice. Please read our Disclaimers.