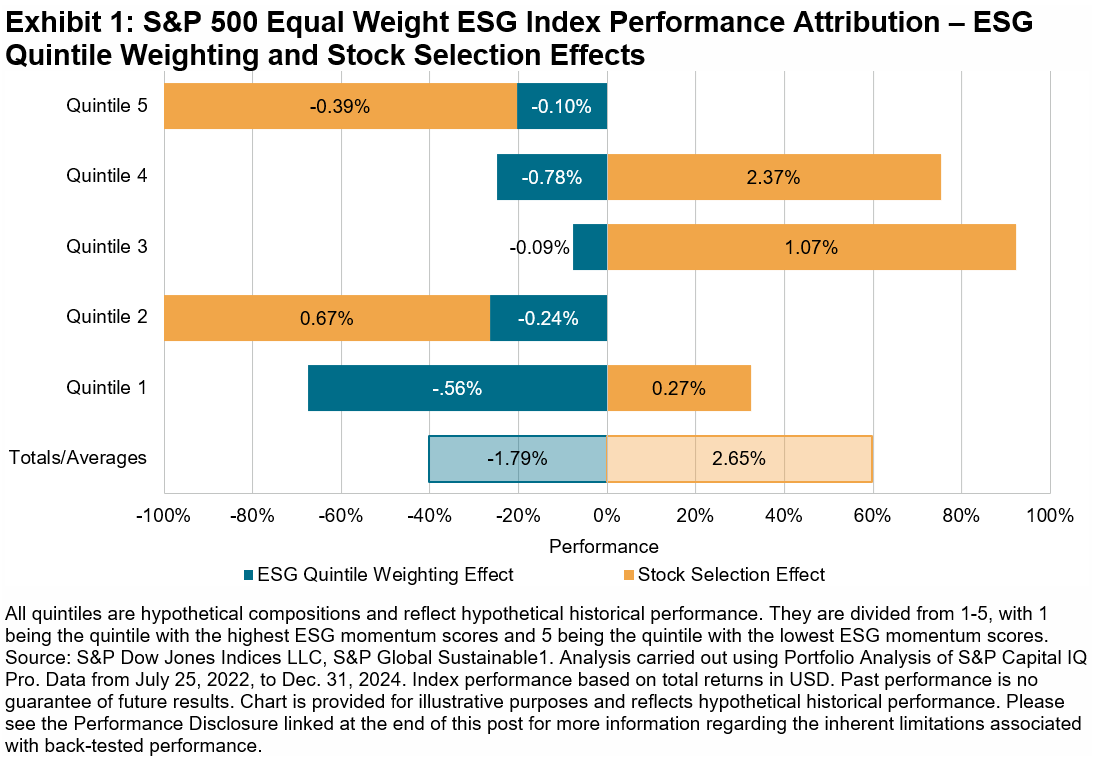

S&P DJI recently launched a new family of indices known as the S&P Quality FCF Aristocrats which includes the S&P 500® Quality FCF Aristocrats® Index and the S&P Developed Quality FCF Aristocrats Index. A more comprehensive introduction to this family of indices can be found in this blog post.

Gaining insights into the historical performance of factor strategies across various macroeconomic environments is essential for risk mitigation and informed investment decisions. In this blog, we will begin by analyzing the performance of these two newly launched indices across different economic regimes. Following that, we will compare the performance of the S&P 500 Quality FCF Aristocrats Index with that of another Aristocrats-branded index, the S&P High Yield Dividend Aristocrats, across the same four economic scenarios.

Macroeconomic Framework1

To assess performance across different economic environments, we use a framework that defines four distinct regimes based on whether growth2 and inflation3 are rising or falling. These regimes are organizing into four quadrants which are illustrated in Exhibit 1.

Considering the longer back-tested history available for the U.S. market compared to other developed markets, we present two distinct time horizons in our analysis (see Exhibit 2). The first time horizon spans 282 calendar months from May 31, 2001, to Oct. 31, 2024 for U.S. markets, while the second covers 222 calendar months from May 31, 2006, to Oct. 31, 2024, for developed markets. Exhibit 2 displays the number of months and relative frequency across each regime.

Performance Across Growth and Inflation Regimes

The historical risk/return characteristics of the S&P Quality FCF Aristocrats Indices and their respective benchmarks across the four economic regimes are illustrated in Exhibit 3. Historically, all the indices presented demonstrated highest absolute returns and risk-adjusted returns in the Rising Growth and Falling Inflation regime, followed by the Rising Growth and Rising Inflation regime. Conversely, these indices experienced much lower returns in the Falling Growth and Falling Inflation regime, with the worst returns—often negative—occurring in the Falling Growth and Rising Inflation regime.

Excess Returns4 in Four Economic Regimes

In this section, we analyze the macroeconomic performance of the S&P Quality FCF Aristocrats Indices in terms of their excess returns (ER) relative to their benchmarks (see Exhibit 4).

The S&P 500 Quality FCF Aristocrats Index consistently outperformed the S&P 500 in a Falling Growth environment, regardless of inflation trends. In the Rising Growth and Falling Inflation regime, its performance was comparable to that of the S&P 500. However, in the Rising Growth and Rising Inflation regime, it underperformed. This behavior indicates that the S&P 500 Quality FCF Aristocrats Index exhibits strong defensive characteristics whilst still meaningfully participating in market upside.

The S&P Developed Quality FCF Aristocrats Index consistently outperformed the S&P Developed LargeMidCap index by a wide margin in a Falling Growth environment, regardless of inflation trends. In the Rising Growth regime, its performance was slightly better than its benchmark. The results indicate that the S&P Developed Quality FCF Aristocrats index outperformed S&P Developed LargeMidCap in all economic regimes, meaning it was defensive in down markets while keeping pace strongly in up markets.

Comparison with the S&P High Yield Dividend Aristocrats

In a previous blog, we compared the S&P 500 Quality FCF Aristocrats Index with the S&P High Yield Dividend Aristocrats, demonstrating that these two indices provide differentiated exposure and track companies with distinct profiles. Now, let’s examine how they perform across the defined macroeconomic regimes.

Overall, the indices have differentiated exposure across these regimes. The S&P High Yield Dividend Aristocrats achieved its highest excess returns during the Falling Growth and Rising Inflation environment. In contrast, the S&P 500 Quality FCF Aristocrats led the way during both Falling Growth regimes, regardless of the inflation regime. However, both indices underperformed relative to the broad market during the Rising Growth and Rising Inflation regime.

In conclusion, the S&P Quality FCF Aristocrats Indices have historically outperformed during periods of falling economic growth, regardless of the inflation regime. In times of rising growth, both indices performed in line with the benchmark during falling inflation; however, the S&P 500 Quality FCF Aristocrats lagged when inflation was rising. Furthermore, our analysis shows that the S&P 500 Quality FCF Aristocrats offer differentiated exposure compared to the S&P High Yield Dividend Aristocrats, highlighting their potential as complementary tools.

1 Hao, Wenli Bill and Rupert Watts, “A Historical Perspective on Factor Index Performance across Macroeconomic Cycles,” S&P Dow Jones Indices LLC, Nov. 14, 2024.

2 Rising growth is defined as a positive monthly change in the U.S. Composite Leading Indicator (CLI) compared to the previous month, while falling growth is defined as a negative monthly change.

3 Rising inflation occurs when the three-month average of U.S. Consumer Price Index (CPI) exceeds that of three-year moving average, while falling inflation occurs when falling below.

4 Excess return measures how much the average monthly total return of each index exceeds that of its corresponding benchmark in each regime.

The posts on this blog are opinions, not advice. Please read our Disclaimers.