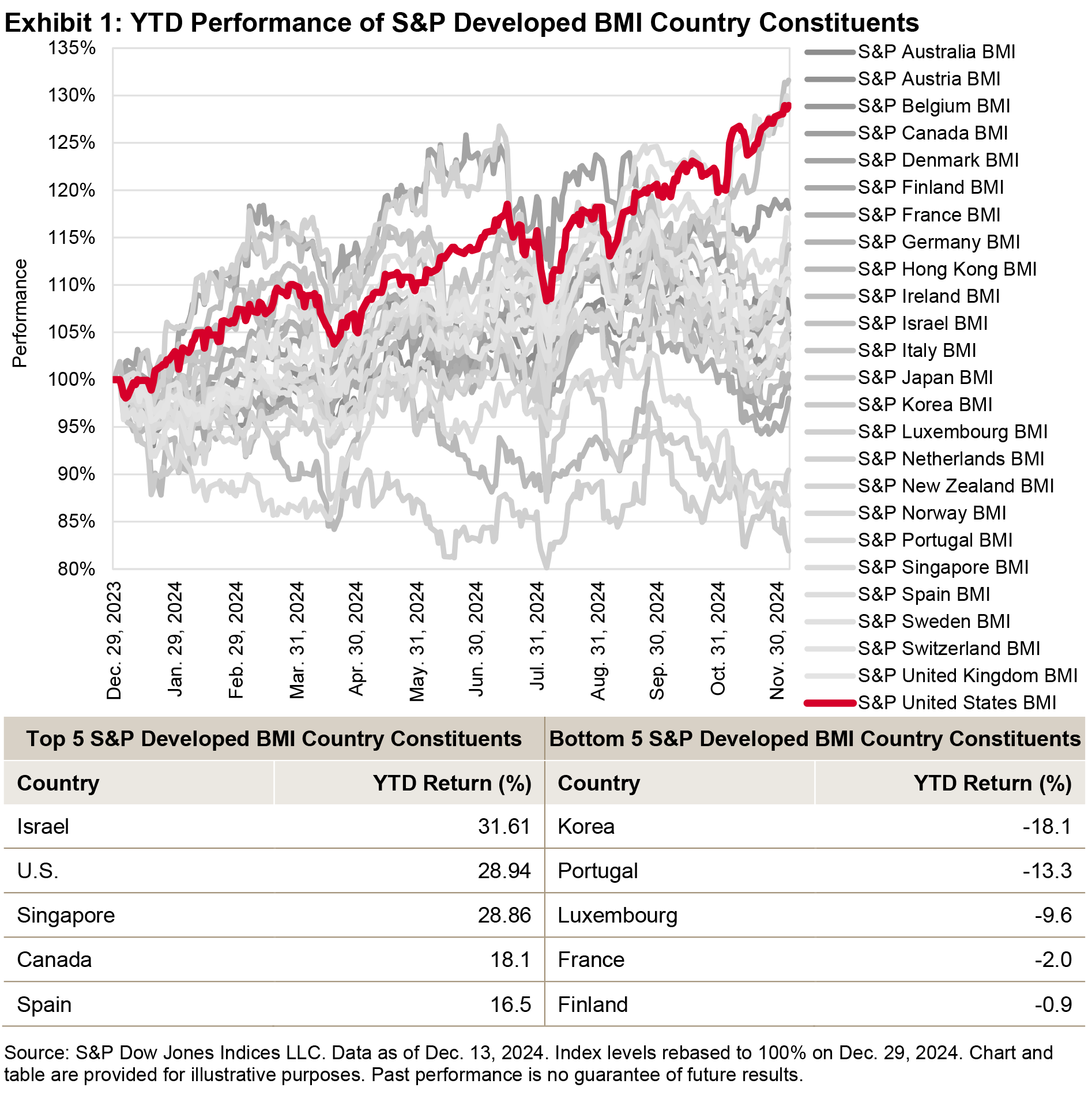

U.S. equity markets enjoyed a great year in 2024, but the returns in many developed equity markets were found wanting in relative terms and, in many cases, absolute terms as well.

With just a few trading days left in 2024, the S&P Developed BMI has gained 22% YTD as of Dec. 13, 2024, with all but 3 of its 25 members lagging the benchmark. Five regions produced outright losses YTD, with Korea at the bottom of the list, down 18%. Of the remaining 20 markets, 10 produced returns in the single-digit percentages, and only 3 (the U.S., Singapore and Israel) were up over 20%.

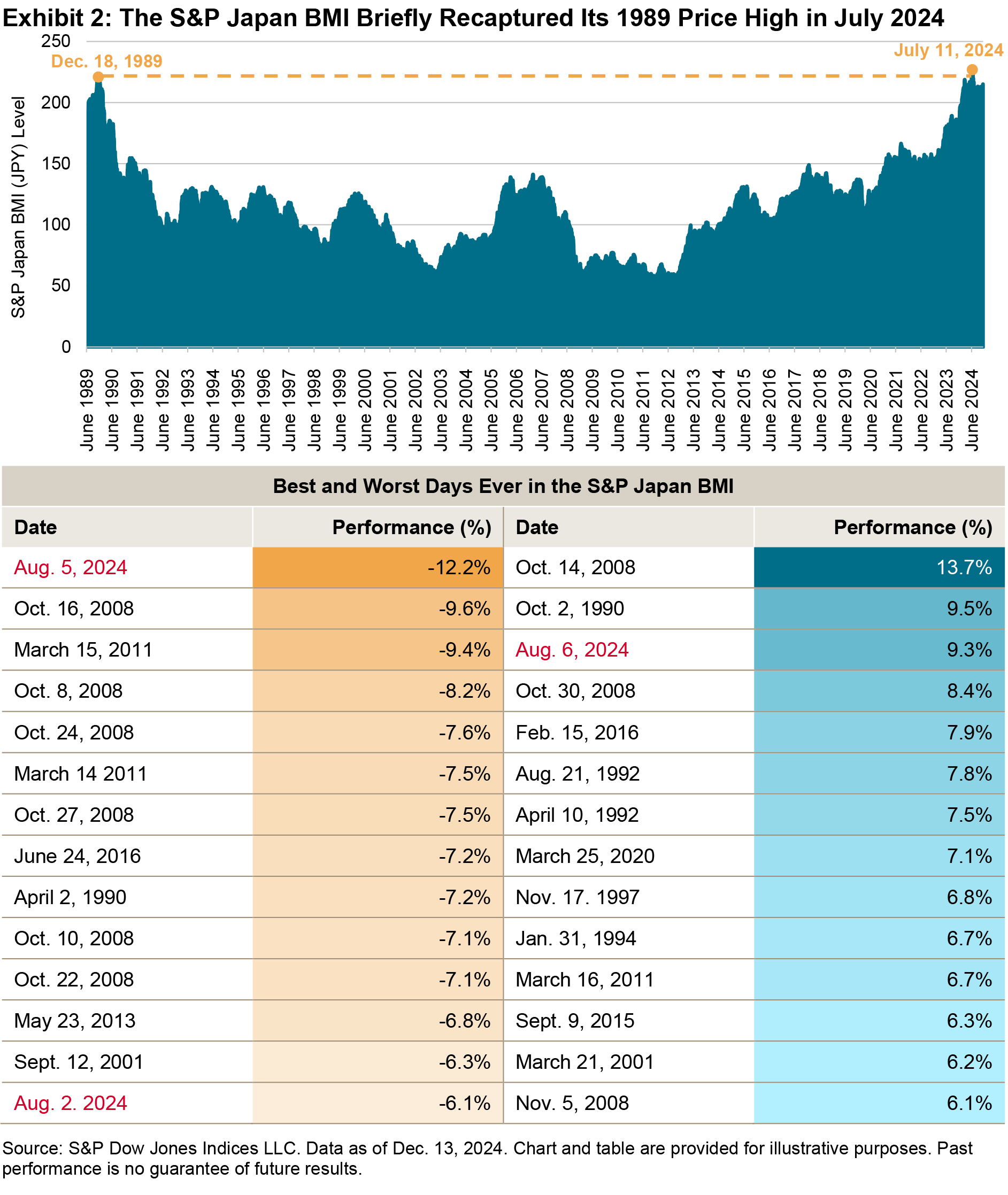

Among developed markets, Japan not only kept up with the U.S. until the beginning of August, but it was even ahead until early May. On the back of this year’s gains, the local currency version of the S&P Japan BMI finally surpassed its prior all-time high recorded on Dec. 18, 1989. However, investors in the local market didn’t have long to celebrate.

In the beginning of August, the Bank of Japan surprised market participants with an unexpected monetary tightening at a time when the world’s other major central banks were already in easing mode. The Bank of Japan’s action triggered turmoil in capital markets around the world, with Japan at the epicenter. The Japanese yen had aggressive moves in both directions, and so did the S&P Japan BMI, which had its worst one-day loss ever on Aug. 6, 2024, falling over 12%, followed by its third-best day ever the next day as the Bank of Japan made a policy U-turn. Markets have calmed since the early August volatility, and the Japanese benchmark rebounded 24% from its Aug. 5 lows to show a YTD gain of 18%.

Investors in emerging markets had to contend with generally lower returns than those in developed markets, with the S&P Emerging BMI lagging the S&P World Index by 8% YTD. Emerging market investor attention this year has been focused on Asia’s two giants and their diverging economic and stock market fortunes. On the one hand, Chinese equities had been grinding steadily lower until mid-September, with the S&P China BMI PR down for the year as recently as Sept. 23, as the country’s economic growth sputtered.

The S&P India BMI, on the other hand, soared 26% over the same horizon, and, consequently, came within a whisker of overtaking China as the region with the largest weight within the S&P Emerging BMI. Since then, China’s weight in the emerging market benchmark rebounded together with local equities, which rose over 20% on the back of the government’s latest round of stimulus measures. However, doubts still remain about whether the latest policy actions will produce a lasting recovery in 2025 and beyond.

As we approach the end of 2024 and head into 2025, the contrasting performance patterns of various developed and emerging markets around the world underscore the complexities that investors may face, highlighting the need for careful analysis and strategic positioning in an ever-evolving global landscape of equity markets.

The posts on this blog are opinions, not advice. Please read our Disclaimers.