Despite recent sharp U.S. market declines after the Federal Reserve signaled fewer than expected rate cuts, much of recent year-end market commentary has been focused on U.S. exceptionalism and the divergence of U.S. equities compared to the rest of the world. The S&P 500® was up 24.8% YTD through Dec. 18, 2024, reaching 57 all-time closing highs so far this year, propelled by robust economic growth, AI-related enthusiasm and optimism surrounding President-elect Trump’s return.

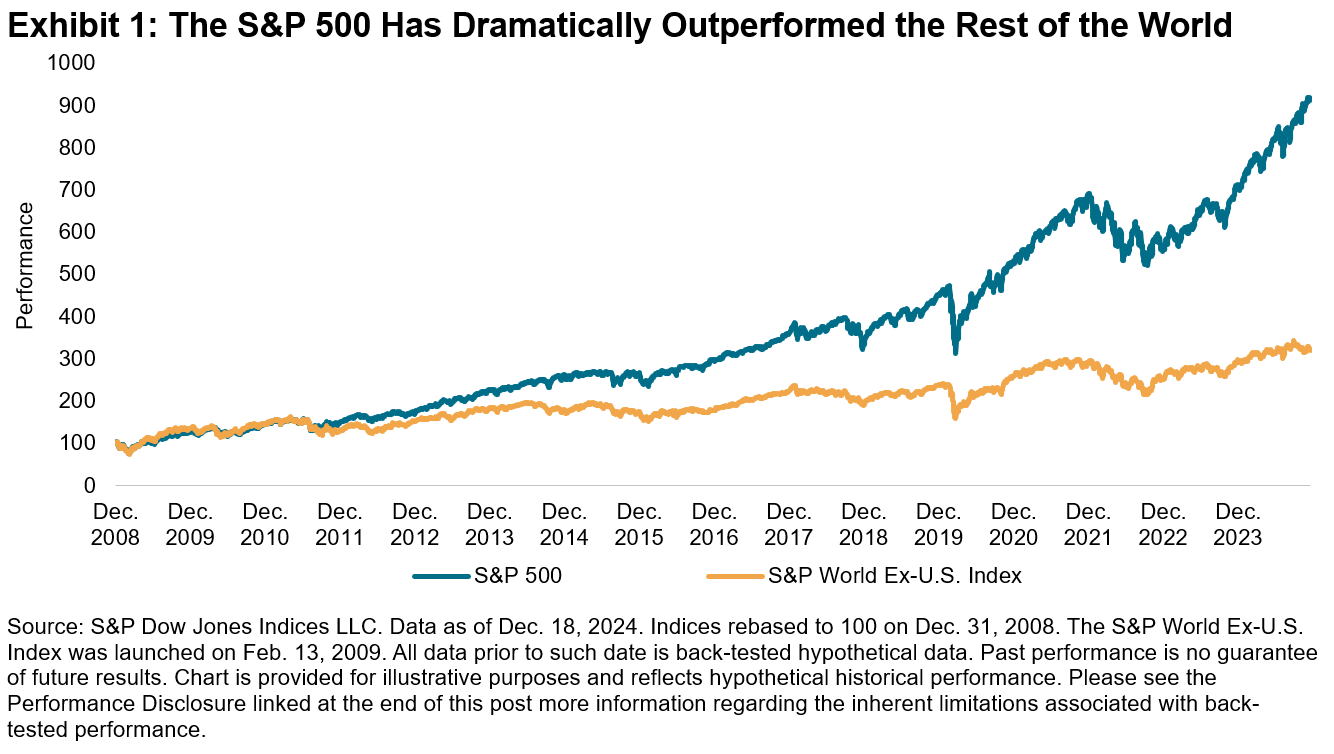

Exhibit 1 shows that U.S. outperformance is not a new phenomenon. The S&P 500 has significantly outperformed the rest of the world over the past fifteen years, with a cumulative return of 887% since Dec. 31, 2008, compared to an equivalent return of 320% for the S&P World Ex-U.S. Index.

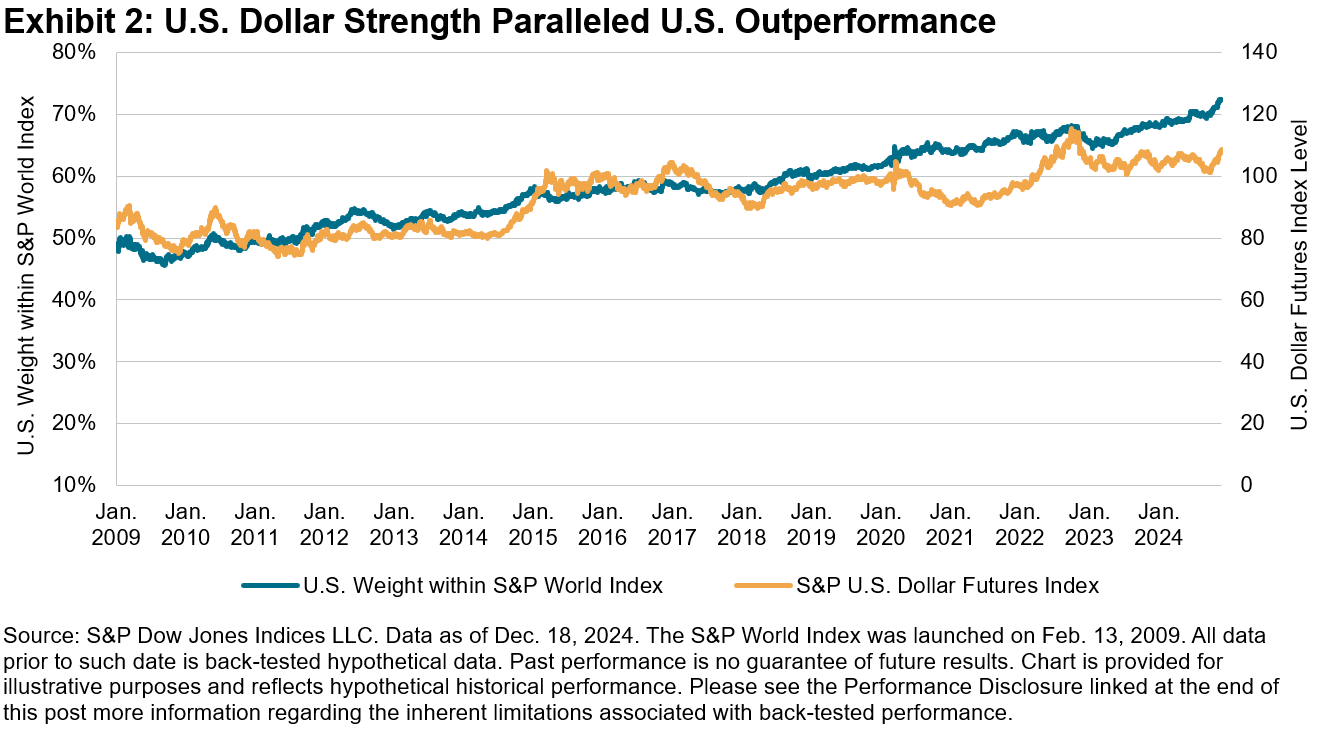

We’ve noted previously that concentration trends can manifest at a country level. As a result of its outperformance, the weight of the U.S. component of our S&P World Index has risen accordingly from roughly 50% in 2009 to over 70% currently. Meanwhile, the U.S. dollar has strengthened in tandem, as illustrated by Exhibit 2, which may create potential headwinds for large-cap multinational companies that tend to have more overseas revenue exposures and tailwinds for smaller, more domestically sensitive stocks.

Turning our attention across the capitalization spectrum, the outperformance of U.S. equities broadened beyond large caps during the second half of the year, thanks to additional catalysts beyond dollar strength, including Fed rate cuts and post-election enthusiasm for potential impending tariff policies that may benefit smaller caps. Although mega caps have returned to favor so far in December, the S&P MidCap 400® and the S&P SmallCap 600® have outperformed the S&P 500 by 2.6% and 5.2%, respectively, since July 9, a key turning point for U.S. markets, as investors began to shift away from the Magnificent 7 and other mega caps toward smaller companies.

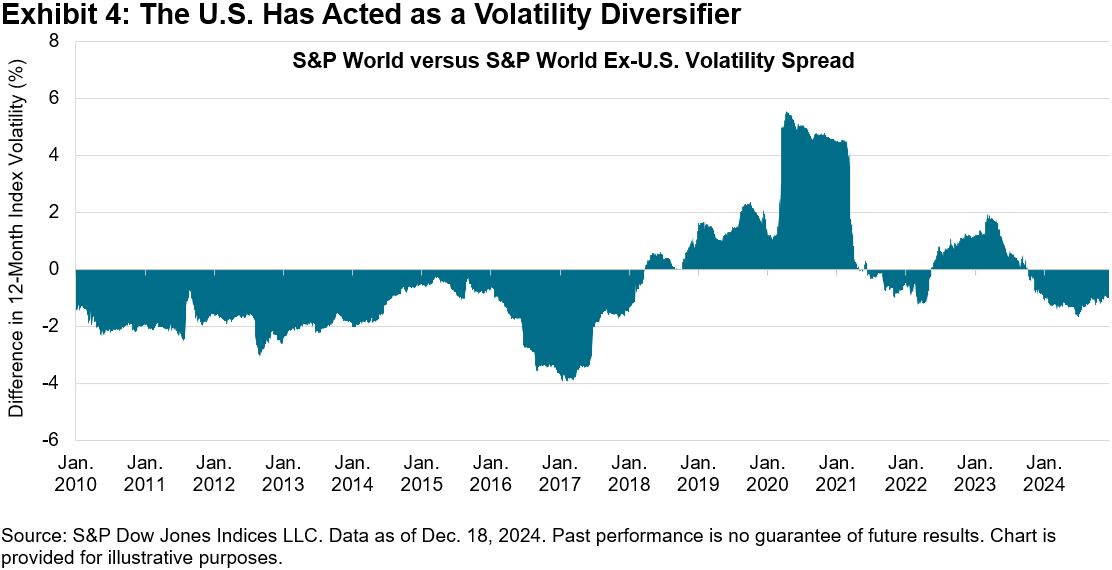

In addition to their stellar outperformance, U.S. equities are interesting to analyze for their diversification potential. In Exhibit 4, we calculate the spread in trailing 12-month volatility between the S&P World Index and S&P World Ex-U.S. Index. When this spread is positive, the inclusion of the U.S. increases volatility in the benchmark; when negative, the country acts as a diversifier. The negative spread that has occurred so far this year is an indication that the U.S. has become a volatility diversifier,1 consistent with the divergent performance observed earlier.

As we look ahead to 2025, while we do not know whether the U.S. market rally will be sustained or if smaller caps will maintain their momentum, we can acknowledge that if the outperformance of the U.S. compared to the rest of the world continues, the associated diversification properties may have important consequences for asset owners globally.

1We do acknowledge that the U.S. makes up more than 70% of the weight in the S&P World Index, but caveat that the U.S. component includes exposure to large multinational companies that have a diverse revenue base across geographies.

The posts on this blog are opinions, not advice. Please read our Disclaimers.