It’s well known that as the U.S. consumer goes, so goes its economy. Various estimates suggest that around 67% of U.S. GDP depends on consumer spending. At the macro level, all this consumer spending translates into the consumption of goods and services. The U.S. economy, like most developed economies, comfortably falls into the category of a service-driven economy. Although manufacturing’s contribution to nominal U.S. GDP is small, the manufacturing segment is a closely tracked macroeconomic metric that forms part of the Leading Economic Indicators (LEI) basket to track the economic cycle.

Manufacturing in Policy Crosshairs

On the global stage, the manufacturing segment has come under increased scrutiny in the current geopolitical climate, as approximately 50% of the world’s population heads to the voting booth. The peak pandemic supply chain disruptions exposed the fault lines around the Just-In-Time manufacturing framework, which was optimized for low cost above all else. There is now a reassessment of these supply chains with increased emphasis on resilience to global disruptions (e.g., the COVID-19 pandemic) and perceived national security threats.

Tariffs have increasingly been used as a policy instrument by governments even before the pandemic, as part of a carrot-and-stick approach to rejuvenate domestic manufacturing. While not all tariffs induce growth in local manufacturing, both the previous and current U.S. administrations have cited increased domestic manufacturing as a major factor in applying tariffs. On the carrot side of this approach, the current administration’s fiscal spending programs also allocate a sizable amount to incentivize local manufacturing. Companies and financial markets have also responded to this evolving trend, with references to “reshoring” and related terms in the earnings calls soaring in the last couple of years.1

Fabrication with a Focus

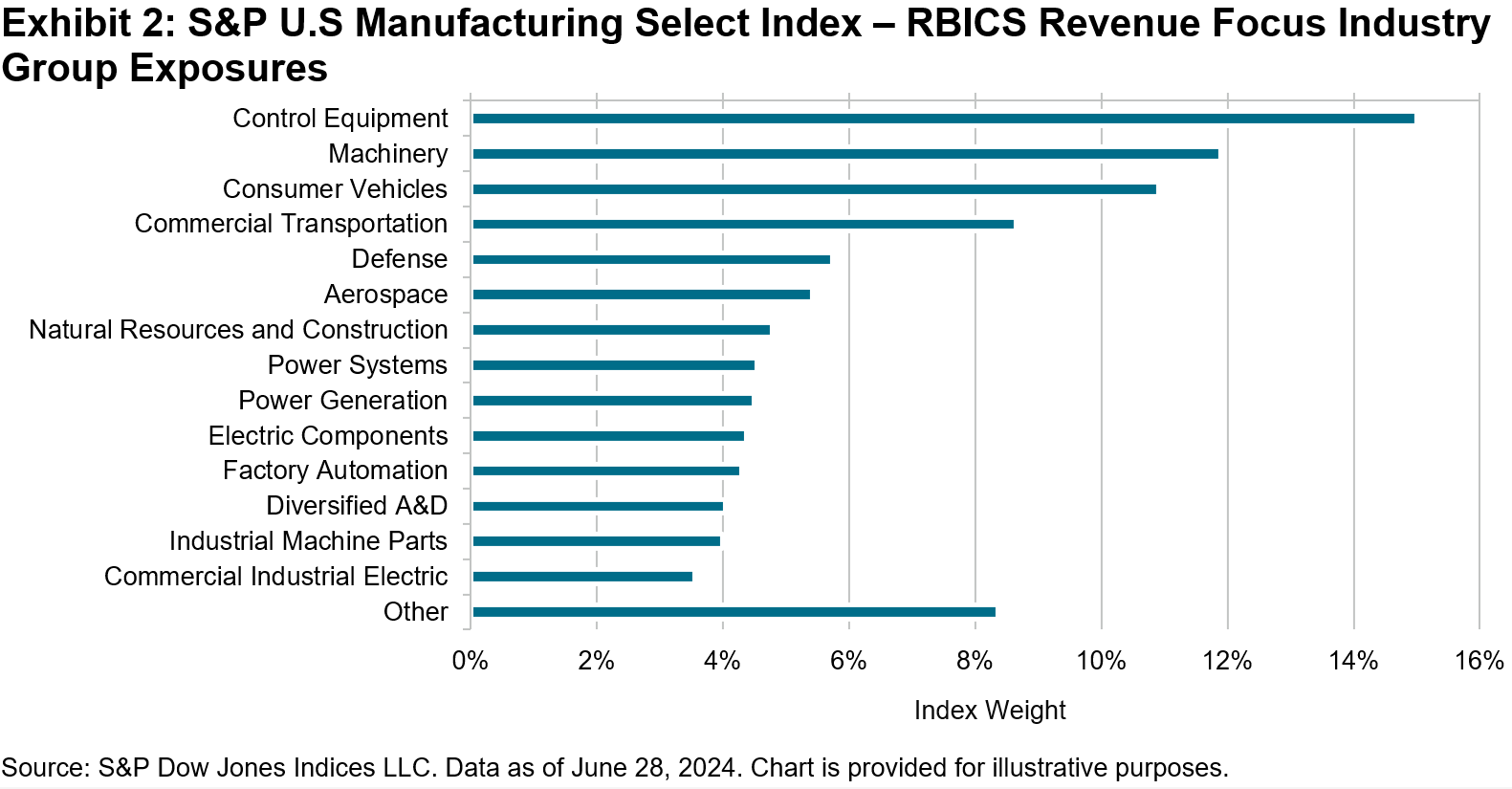

The S&P U.S Manufacturing Select Index was launched in April 2024 and tracks U.S.-listed companies that have a significant portion of their revenue sourced from U.S. markets, and whose revenue streams fall into one of the 11 industry group categories as defined within FactSet’s Revere Business Industry Classification System (RBICS) Focus framework. The index is weighted using an adjusted float-market-cap approach, optimized for constraints to provide constituent-level and RBICS category-level diversification.

The 11 revenue categories for this index are spread across three main RBICS Focus sectors—Industrial Manufacturing, Consumer Vehicles and Parts, and Electronic Components and Manufacturing. These categories are selected based on their direct relevance to U.S. tariffs and legislations targeting a U.S. manufacturing resurgence. Fractious geopolitics are expected to bring about a new era of increased defense spending, and some of the selected revenue categories also align with U.S. strategic priorities around building a “resilient industrial base.”

FactSet’s Geographic Revenue data categorizes approximately 67% of the index constituents’ revenue being sourced from the U.S. As expected, the latest basket is heavily tilted toward the Industrials sector (approximately 75%), with Machinery, Electrical Equipment, and Aerospace & Defense as the primary industries. The index is balanced across the RBICS industry groups, with the 5 biggest groups accounting for 52% of the index weight.

The index’s five-year performance has been robust, slightly outperforming its starting universe of the S&P United States BMI, as well as the S&P 500 Industrials.

Conclusion

The world’s largest economy is pushing to reimagine its manufacturing sector for greater resilience in an environment of increased supply chain risks, coupled with attention to national security concerns. The S&P U.S. Manufacturing Select Index tracks a subset of companies belonging to a curated list of RBICS revenue focus categories, which we believe are closely aligned with industries at the forefront of these manufacturing shifts—sometimes characterized as “reshoring.” This multifaceted approach leads to index constituents not only from the Industrials sector, but also from Information Technology (Semiconductors segment) and Consumer Discretionary (Consumer Vehicles segment) sectors.

1 Sources: ETFStream, The Wall Street Journal, Yahoo Finance and Bank of America Institute.

The posts on this blog are opinions, not advice. Please read our Disclaimers.