Planes are interesting places, airborne aluminum tubes stuffed with strangers from all walks of life, including seatmates prodding with the proverbial ice-breaker, “So, what do you do?” Overhearing many such conversations, I’ve found complicated job descriptions elicit blank stares and subsequently lead to higher-level answers such as “Well, I’m in tech,” or “I work in finance,” or “Been in energy my whole career,” followed by the “Ahhhh, OK!” of understanding. That’s because every profession, truly everything, falls into an industry that ultimately rolls up into one of the 11 GICS® sectors, and after frequently observing the ups and downs of sectors as they gather mileage over the years, we all know what they “do.”

We also know sectors are globally relevant, immense in size and important to nearly every economic discussion and investment strategy. That’s why we continue to research their application, including in our recent paper: Natural Selection: Tactics and Strategy with Equity Sectors.

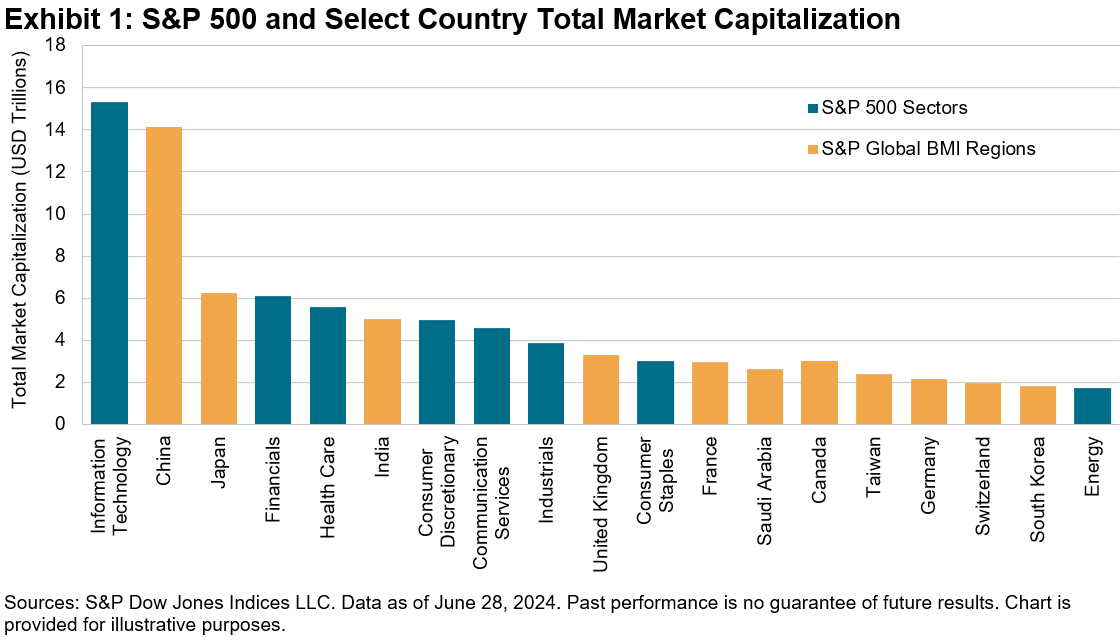

While the S&P 500’s USD 45 trillion total market cap reflects the U.S.’s position as the largest equity market in the world, individual S&P 500 sectors are also prominent, with many surpassing the total market cap of major single-country equity markets, as shown in Exhibit 1.

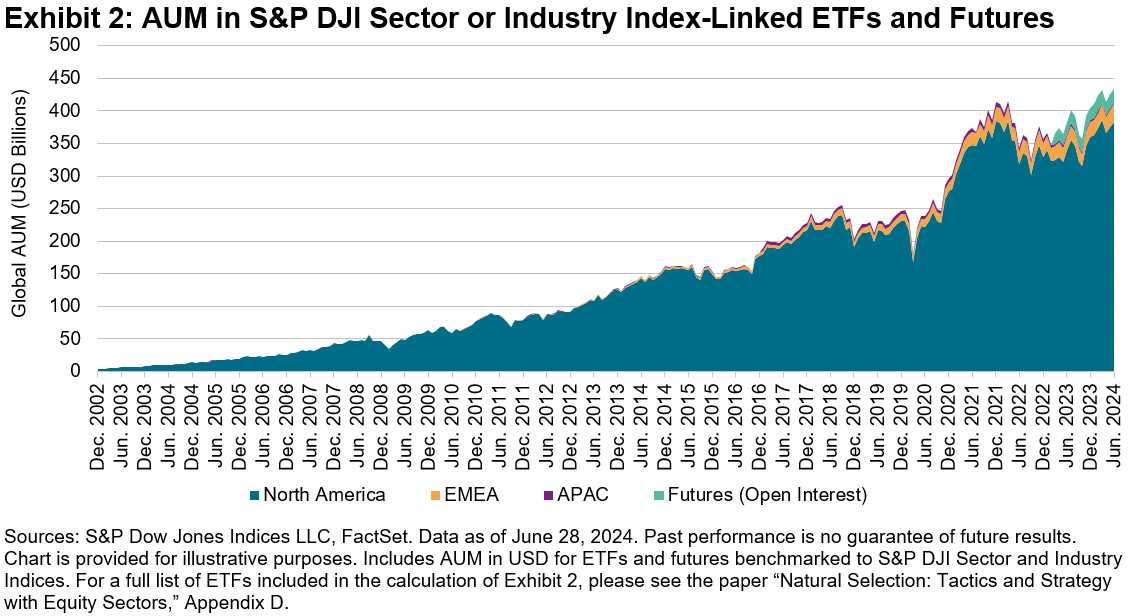

Since their inception, the use of S&P 500 Sector Indices as benchmarks for products has become increasingly widespread around the world. From the Middle East to the U.K., Japan and beyond, possible applications of S&P 500 sectors range from avoiding home bias and diversifying sector exposures to driving performance through tactical and strategic sector tilts. For evidence of the continuing growth of sector applications, one need not look further than the aggregate assets under management (AUM) in globally domiciled sector and industry index instruments (exchange-traded funds [ETFs] and futures), as shown in Exhibit 2.

Growth in sector assets could be a byproduct of investors worldwide understanding not only what each sector includes, but also how each sector historically tended to perform in different phases of the economic cycle. The differentiated holdings and low correlations of excess performance among sectors and industries has offered the possibility of seeking outperformance through sector tilting or rotation.

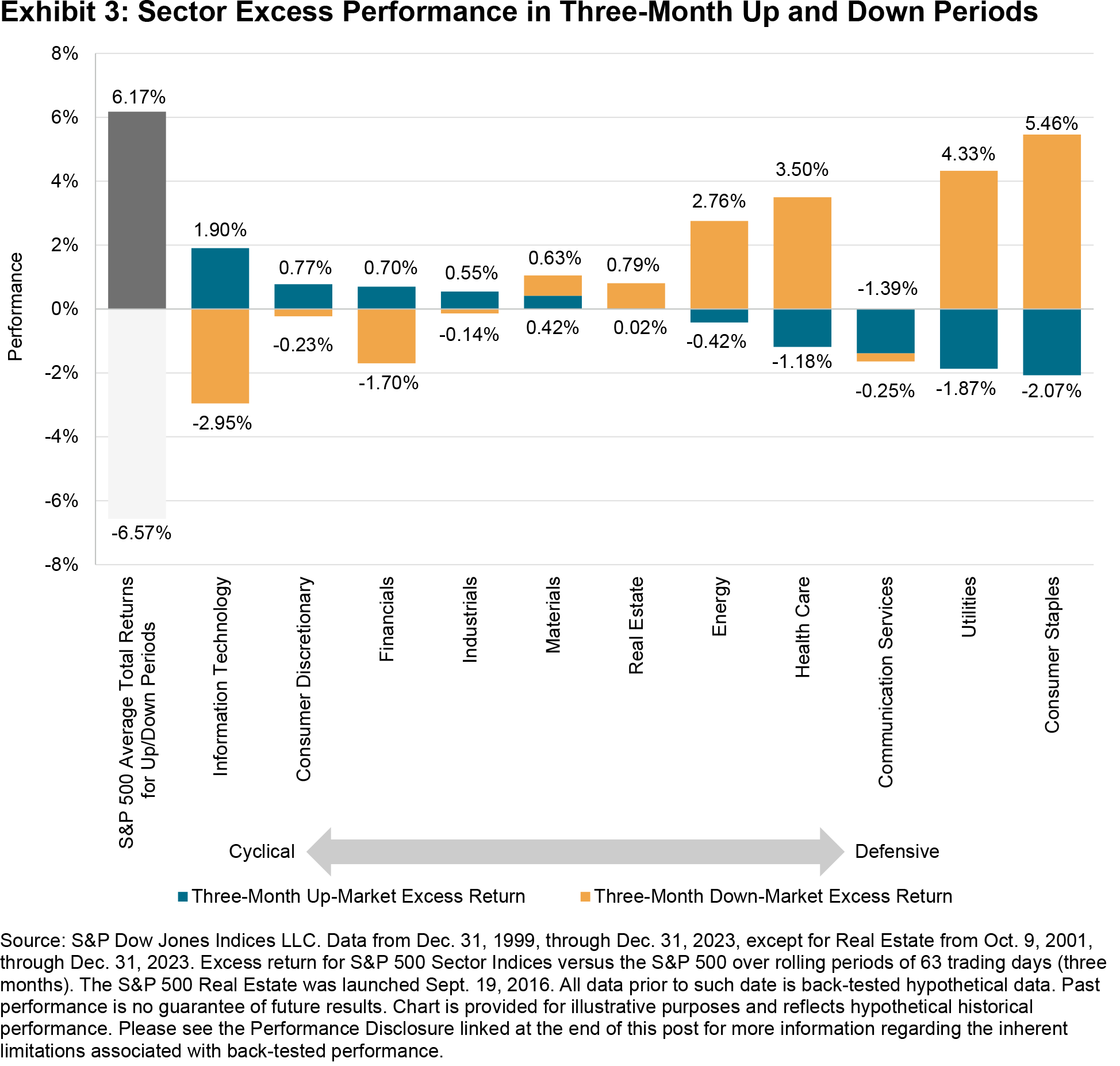

For example, categorization of sectors into cyclical groupings (those that have historically tended to exhibit higher beta and outperform during expansions) and defensive groupings (those that have tended to exhibit lower beta and outperform during declines) can also be effective. Categorizing sectors into defensive or cyclical groups based on ranking their risk attributes and their excess returns during rising or falling markets can offer insight into the potential outcome of sector tilts that historically achieve relatively better performance in each environment. Exhibit 3 illustrates this point, showing the average rolling three-month excess performance of S&P 500 sectors during periods when the S&P 500 was rising or falling.

While the eventual rise and fall of markets seems inevitable, no one can perfectly predict how much turbulence we’ll encounter during the journey. Fortunately, sectors are one tool to understand and navigate through whatever bumps are encountered along the way.

The posts on this blog are opinions, not advice. Please read our Disclaimers.