How are advisors using sector data to understand market trends and inform investment decisions? S&P DJI’s Anu Ganti joins Fairlead Strategies’ Katie Stockton to discuss practical applications for sector indices.

The posts on this blog are opinions, not advice. Please read our Disclaimers.A Tactical Look at Sectors

An Elevating Effect on Equal Weight?

The Magnificent Seven: A Taxing Question

Measuring Fixed Income Opportunities in Asia with Indices

Material Change in a Material World

A Tactical Look at Sectors

An Elevating Effect on Equal Weight?

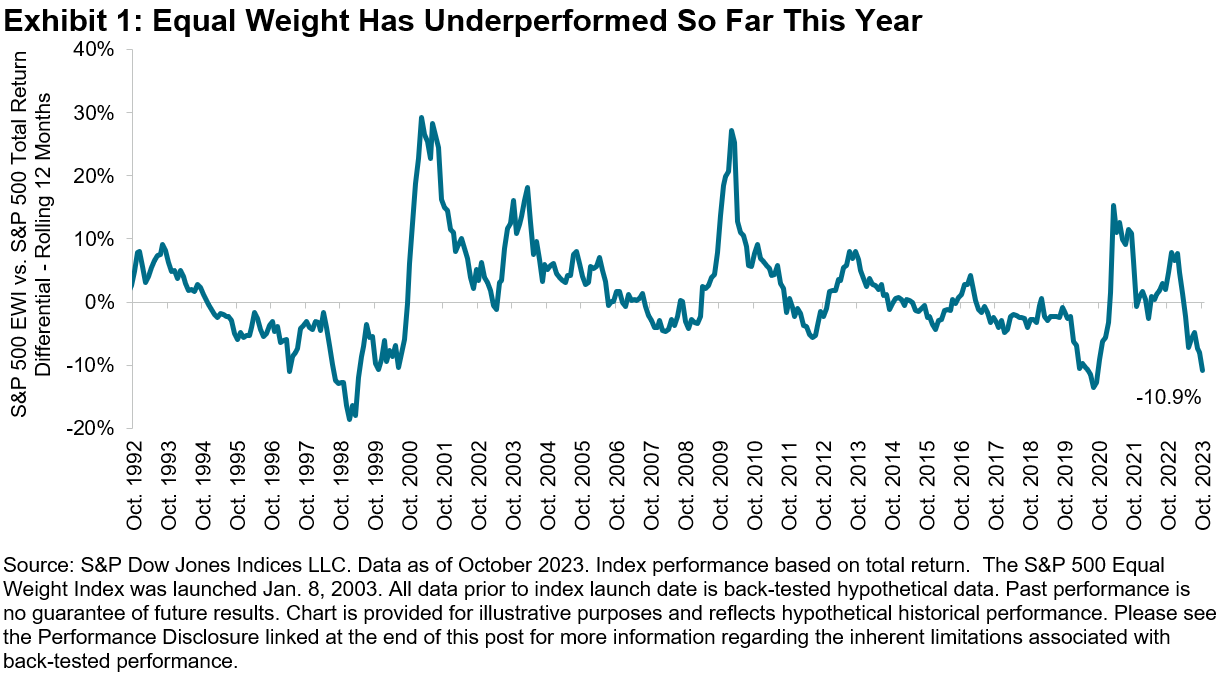

The trouncing of smaller caps by mega-cap stocks has been one of the hallmark market themes of this year, with the S&P 500® Top 50 outpacing the S&P SmallCap 600® by 30% YTD.1 As a result of its inherent small-cap bias, the S&P 500 Equal Weight Index (EWI) has suffered accordingly, underperforming the S&P 500 by 11% in the twelve months through October. But as we observe from the troughs and peaks in Exhibit 1, Equal Weight has always managed to recover from deep losses. February 2001, February 2010 and March 2021 are three prime examples, post major events like the tech bubble, financial crisis and COVID-19 recession.

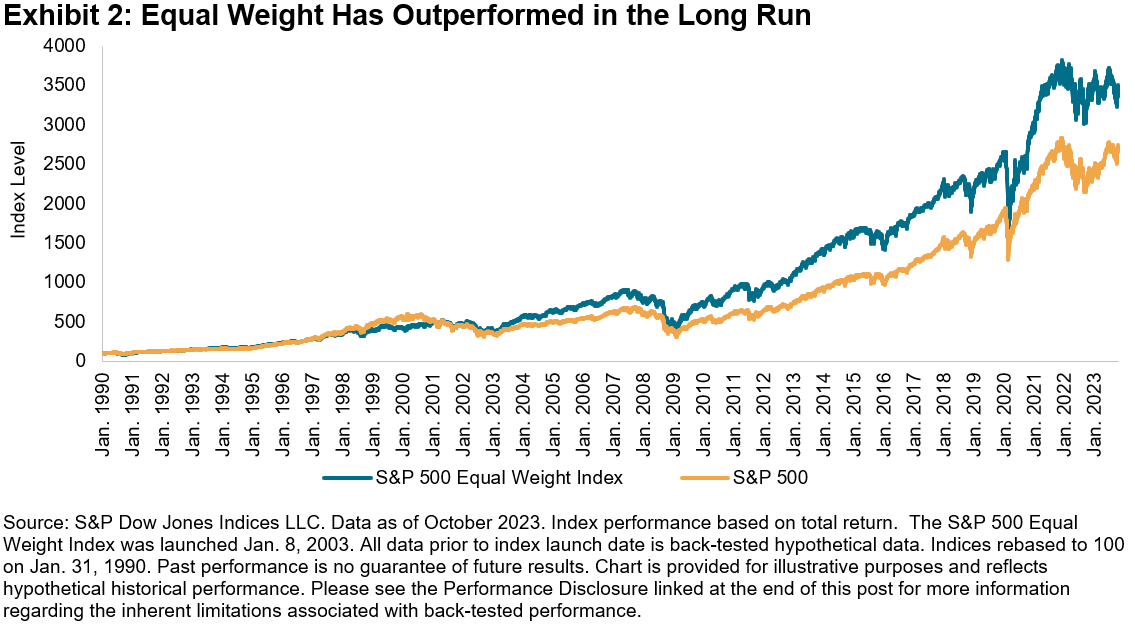

While the strategy has weakened so far this year, we know from Exhibit 2 that Equal Weight tends to outperform over the long term. The strategy’s small size, anti-momentum and value tilts are key performance contributors. Further, Equal Weight’s innate rebalancing mechanism of selling the winners and buying the losers is an important benefit of the mean reversion we observe in Exhibit 1.

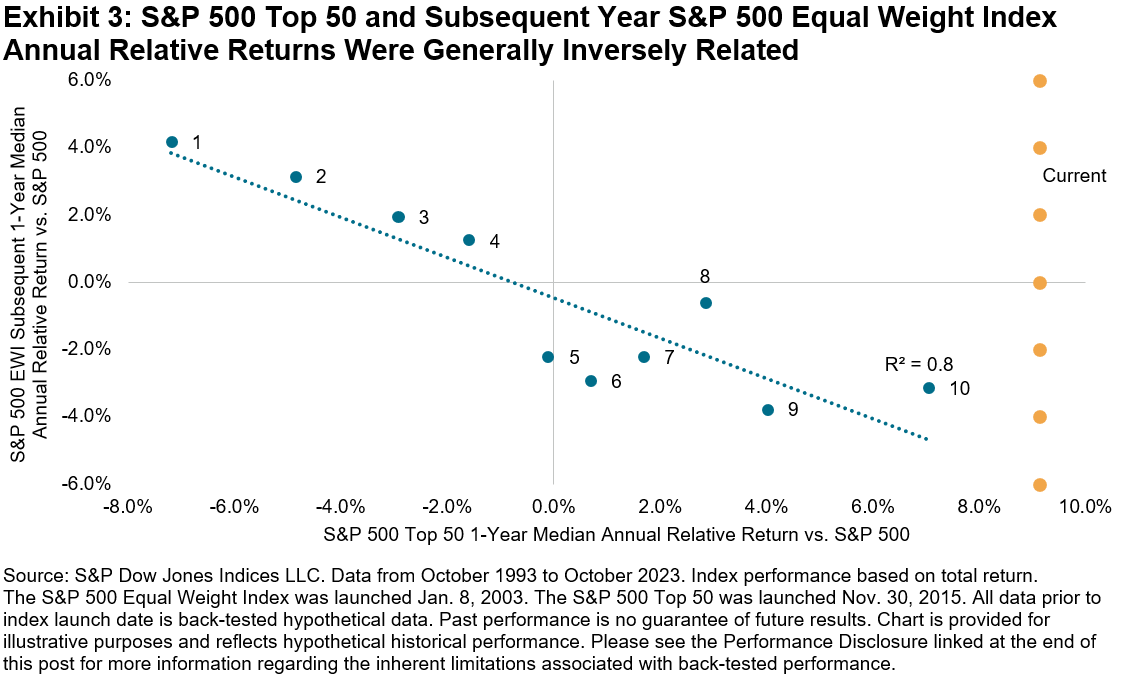

The quandary at hand is that it’s difficult to know in advance when the inflection point of outperformance for Equal Weight will occur. Historically, we have seen that turning points have coincided with extremes in mega-cap outperformance. We can visualize this relationship by ranking the months in our database by the 12-month relative performance of the S&P 500 Top 50 and dividing them into deciles. Next, we analyze the median subsequent 12-month performance of Equal Weight in each of these deciles. We observe that lower decile S&P 500 Top 50 months tended to be followed by Equal Weight outperformance in the next year, while higher deciles tended to be followed by Equal Weight underperformance.

Currently, thanks to the dominance of the Magnificent Seven stocks, we are at high levels of mega-cap outperformance relative to history, with the S&P 500 Top 50 outperforming the S&P 500 by 9% in the 12 months through October, beyond the 10th decile by a margin of 2%. Historically, we have seen that a retreat toward a lower decile tended to follow, accompanied by Equal Weight outperformance. Whether we experience a pullback in mega-cap strength or a continuation in mega-cap momentum remains to be seen.

1 Performance as of Nov. 17, 2023.

The posts on this blog are opinions, not advice. Please read our Disclaimers.The Magnificent Seven: A Taxing Question

“The Magnificent Seven” term has transcended its cinematic roots to become the collective moniker for a select group of U.S. mega-cap stocks responsible for over 90% of the S&P 500®’s YTD gains to October’s end. Their stellar performance has, naturally, elevated their valuations. It has also increased their already-hefty collective weight in the equity benchmark. Some might be wondering whether, rather than slavishly sticking to capitalization weights, is it now time to adopt an active approach, taking profits and avoiding further concentration?

Sharp rises in stock prices have been somewhat frequent historically, even among the market’s relative giants. Unfortunately, such occasions do not appear to present easy ways to outperform—at least judging by the collective evidence of 20 years of S&P DJI’s SPIVA® Scorecards. But even if the time is right to sell, many investors holding positions in the “Magnificent Seven” will have made a profit on them. Over and above any potential regret for their haste, selling out may invite another unwelcome consequence: a tax bill.

Recently, we published a major extension to the traditional SPIVA library with the first SPIVA After-Tax Scorecard. The report shows that, to put it bluntly: taxes matter. For example, Exhibit 1 (reproduced from the report) shows the impact of taxes on three-year underperformance rates by actively managed broad U.S. equity funds through December 2022.

Is it different this time? The current situation is not unusual. In most recent years, the top seven contributors1 ended the year looking relatively expensive (see Exhibit 2). A particularly intriguing comparison is seen in 2017. At that time, the so-called “FAANGs” faced a similar degree of market skepticism, with P/E ratios averaging nearly three times that of the index itself.

As it turned out: the seven top contributors in 2017 went on to contribute nearly 40% of the S&P 500’s 9.9% annualized return from December 2017 through October 2023. Five of them (including four of the FAANGs) are in today’s Magnificent Seven.

If it were simple to know when to sell seemingly overvalued stocks (as well as when to buy undervalued ones), actively managed funds might boast a better record. The inclusion of tax considerations only makes the evidence more emphatic. And while individual tax circumstances differ, the SPIVA After-Tax Scorecard highlights that taxes could have made a significant impact on the average returns of actively managed U.S. equity funds. They also show that, in recent times, the task of selecting an outperforming active fund net of poorly timed trades, fees and taxes was almost (if not completely) impossible.

1 We recognize that 7 is somewhat arbitrary; why not 6 or 8? For the sake of consistency and with a nod to the contemporary discourse, we stick with the top 7 contributors in each historical period and their trailing P/E ratios at that time.

The posts on this blog are opinions, not advice. Please read our Disclaimers.Measuring Fixed Income Opportunities in Asia with Indices

How are indices helping investors track the continued development of Asian Bond markets? S&P DJI’s Randolf Tantzscher and SSGA’s Kheng Siang Ng discuss how indexing is helping market participants track the evolving fixed income opportunity set across currencies in Asia.

The posts on this blog are opinions, not advice. Please read our Disclaimers.Material Change in a Material World

As our climate changes, so do our ways of producing and consuming energy. A global effort is underway to replace fossil fuels with renewables in our energy matrix.1 This planned energy transition’s speed, scope and scale of impact on the global economy is unparalleled in our history.2 North America’s unique position of contributing nearly 18% of global greenhouse gas emissions, while only housing 5% of the world’s population, puts it under the spotlight. This region of the world is mostly self-reliant for its energy needs derived from carbon-based fuel sources. However, the transition to more renewable energy sources will likely see a higher dependence on the global supply of materials required for a successful energy transition.3

Capturing Relevance from Revenue and Exploration Datasets

To track possible opportunities related to changes in energy production and delivery, we launched the S&P/TSX Energy Transition Materials Index in August 2023. This index provides exposure to North American-listed companies involved in the exploration, mining or manufacturing of materials linked to the energy transition. The index is constructed using input from diverse datapoints—revenue breakdown across various categories from FactSet Revere Business Industry Classification System (RBICS), along with revenue earned, production value and exploration budget segments associated with each of the transition materials for individual companies provided by S&P Global Commodity Insights.

Economics would dictate increased capital spending by mining companies4 on exploration activities to capture the opportunity of rising demand for these transition-related materials. Including the exploration budgets of firms (sourced from S&P Global Commodity Insights) in determining their importance to the energy transition process is a key for a robust index grounded in the economics of supply and demand.

Transition-related materials are very similar to the metals group (aluminum, cobalt, copper, lithium, manganese, molybdenum, nickel, palladium, platinum, silver, rare earth elements and zinc) highlighted in the S&P Global Essential Metals Producers Index, another energy transition-focused index that was launched in August 2023.

The S&P/TSX Energy Transition Materials Index includes all twelve metals covered by the S&P Global Essential Metals Producers Index along with Uranium—which supports a view that nuclear power is a beneficiary of the push toward reduced fossil fuel dependency.5 These thirteen materials are categorized into core and non-core segments. Materials that are expected to see high demand growth specifically from energy transition-related changes are bucketed into core, while the remaining metals fall into the non-core group. The index construction process closely resembles that of the S&P Global Essential Metals Producers Index,6 where an exposure score calculation determines the relevance of each constituent to the theme. There is, however, one important difference.

The S&P/TSX Energy Transition Materials Index also includes companies based on the exploration budget (not just revenue segments) dedicated to these transition materials. Of the current 68 index constituents, 34 constituents (about 28% of the index weight) are included due to their exploration budgets. Of these 34 constituents, 24 do not have tagged revenue segments, underscoring the need for the S&P Global Commodity Insights exploration budget data to complete the index’s well-rounded exposure to the transition metals ecosystem

Index Composition

The index also has a minimum 50 stock count and each stock’s weight is initially set proportional to the product of its float market cap and its corresponding exposure score. Appropriate capping mechanisms are then applied to enhance the liquidity profile and diversification of the index.

The index’s North American-listed requirement puts 60% of the weight in Canadian listings, with the remaining weight in U.S. listings. A GICS® sub-industry breakdown of the constituents highlights the use case for RBICS and S&P Global Commodity Insights datasets to achieve the granularity needed for this index creation. Roughly half of the index exposure to core revenue segments of RBICS is grouped under the GICS sub-industries of Diversified Metals & Mining and Coal & Consumable Fuels.

![]()

1 https://www.spglobal.com/en/research-insights/articles/what-is-energy-transition

2 https://www.imf.org/en/Publications/fandd/issues/2022/12/bumps-in-the-energy-transition-yergin

6https://www.spglobal.com/spdji/en/documents/education/education-fueling-the-energy-transition.pdf

The posts on this blog are opinions, not advice. Please read our Disclaimers.