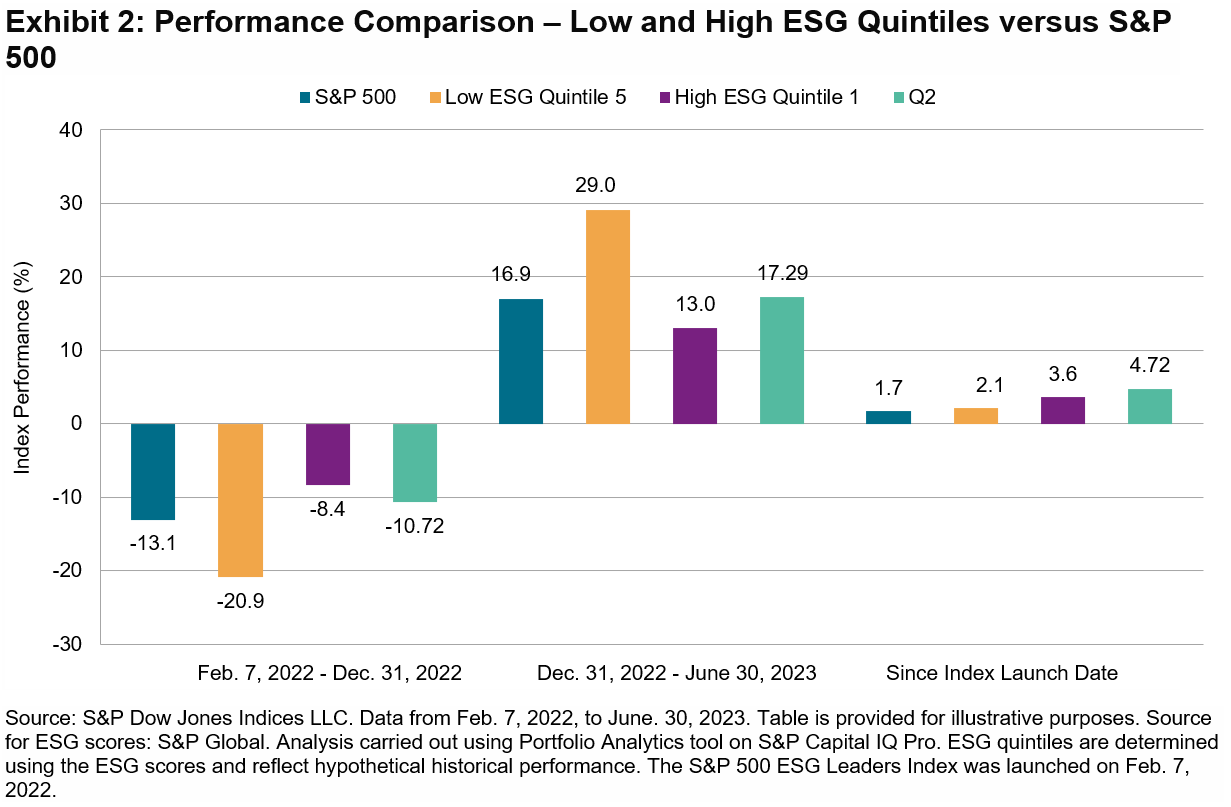

On Sept. 17, 2020, S&P DJI’s Indexology blog shared a post I wrote titled “Comparing Defensive Factors During the Last 3 Bear Markets.” This blog is a continuation of that study, examining the results of the same factors during the 18-month period around the 2022 market correction that led the S&P 500® officially into bear market territory.

As explained in the September 2020 post, Low Volatility and Quality have been commonly referred to as defensive factors. One reason is they have historically exhibited less volatility, as measured by standard deviation, on a consistent basis. Another reason is that over the long term, the maximum drawdown of each of these indices has not matched the extent of the maximum drawdown experienced by the S&P 500. A third reason is that, on average, the S&P 500 Quality Index and the S&P 500 Low Volatility Index have outperformed the S&P 500 during the worst equity market regimes.

In the 2020 post, the bear markets of 2002, 2009 and 2020 were compared by examining the performance of the S&P 500, S&P 500 Low Volatility Index and the S&P 500 Quality Index over an 18-month period that included similar time frames pre and post equity market low. Specifically, the 2002 analysis included 88 days of recovery after the low of 2002, the 2009 analysis included 116 days of recovery after the low of 2009, and the 2020 analysis included 102 days of recovery after the most recent low. This update examines an 18-month period from June 30, 2021, to Dec. 31, 2022, including 80 days of recovery after the 2022 closing low of the S&P 500, registered on October 12.

As a refresher here are the three bear market comparisons from the 2020 report.

The three periods examined above showed the consistently reduced volatility associated with the S&P 500 Quality Index and the S&P 500 Low Volatility Index compared to its benchmark, the S&P 500, during those three bear markets. When it comes to returns, the S&P 500 Low Volatility Index and the S&P 500 Quality Index both outperformed in 2002 and 2009. However, in 2020, while the S&P 500 Quality Index outperformed the S&P 500 again, the S&P 500 Low Volatility Index underperformed.

How did the S&P 500 Quality Index and the S&P 500 Low Volatility Index fare during the most recent challenging equity market environment?

Over the 18-month period from June 30, 2021, to Dec. 31, 2022, the defensive nature of the two indices held up relatively well versus the S&P 500. Both generated superior relative returns over the measurement period, but only the S&P 500 Low Volatility Index experienced lower volatility versus the S&P 500, while the S&P 500 Quality Index was generally in line with the S&P 500.

Whether we are still in the midst of a prolonged bear market or in the early stages of a new bull market is not part of the discussion of this analysis. However, what is interesting to note from this update is that defensive factors continue to show some relative strength during poor equity environments.

The information contained herein has been provided by Andrew Neatt, Senior Portfolio Manager and Senior Investment Advisor of TD Wealth Private Investment Advice is for information purposes only. The information has been drawn from sources believed to be reliable. Graphs and charts are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual’s objectives and risk tolerance.

Index returns are shown for comparative purposes only. Indexes are unmanaged and their returns do not include any sales charges or fees as such costs would lower performance. It is not possible to invest directly in an index.

TD Wealth Private Investment Advice is a division of TD Waterhouse Canada Inc., a subsidiary of The Toronto-Dominion Bank.

The posts on this blog are opinions, not advice. Please read our Disclaimers.