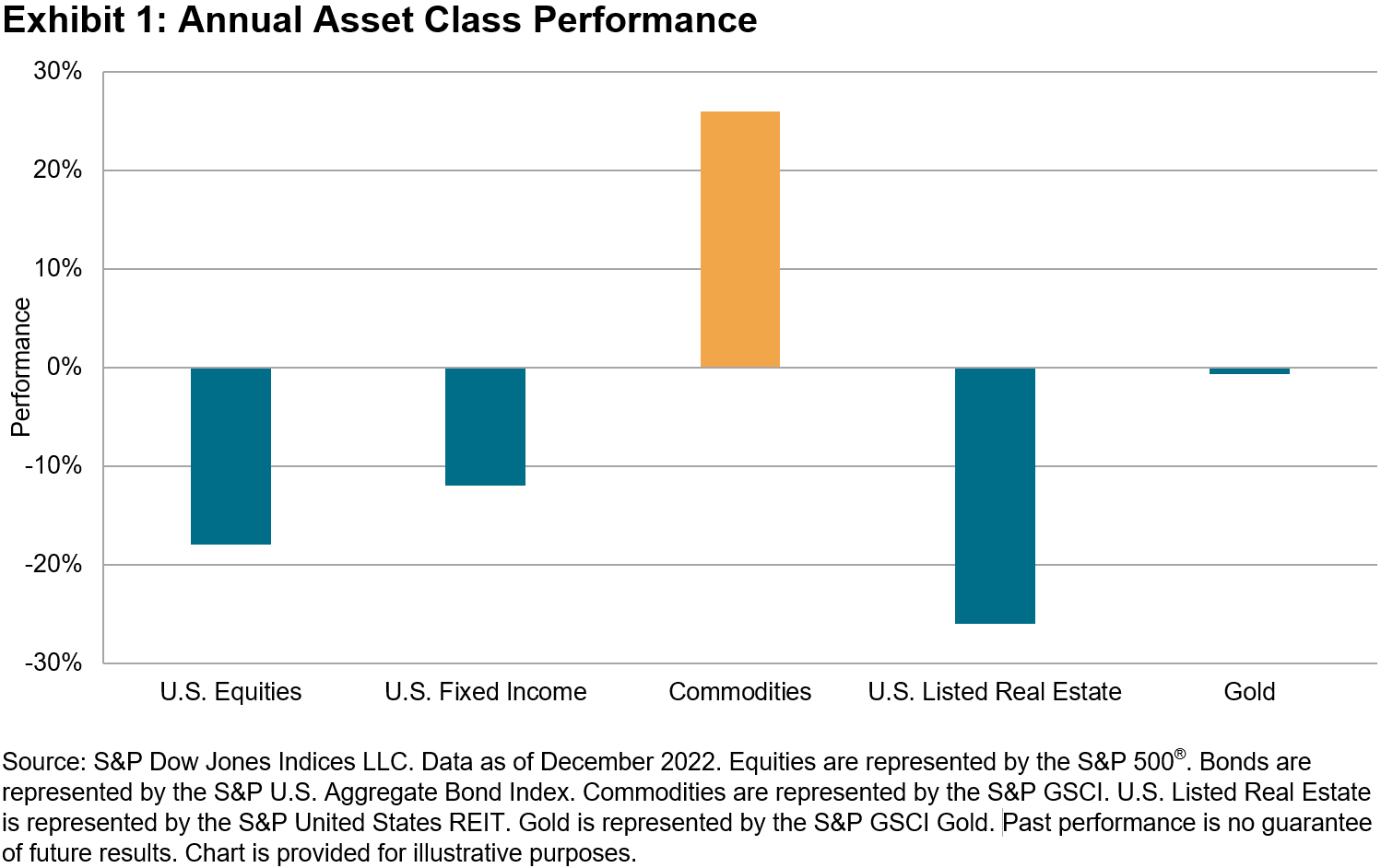

2022 was a difficult year for equity investors as rising interest rates, increasing geopolitical risks and slowing economic growth put downward pressure on equities. However, factors such as dividend yield and value fared much better than the broader equity market due to their shorter durations. Despite this challenging economic environment, the S&P 900 Dividend Revenue-Weighted Index posted an impressive 7.57% in 2022, representing 25.39% outperformance versus its benchmark. In this blog, we will analyze this index’s methodology and examine the dividend yield and value tilts, all of which contributed to its outperformance.

Methodology Overview

To avoid value traps, the methodology begins by excluding the top 5% of stocks based on: (1) the average 12-month trailing dividend yield in the universe; and (2) the last 12-month dividend payout ratio in a GICS® sector. Additionally, only stocks that currently pay a dividend and have had positive revenue over the last 12 months are eligible.

Next, the index selects the top 60 stocks with the highest dividend yield within the eligible universe. These constituents are then weighted by their revenue for the trailing four quarters, with an individual constituent weight cap of 5%. This fundamental weighting approach, rather than a market-cap approach, gives the index a value tilt.

Historical Impact of Dividends on Total Return

Exhibit 2 shows the performance from June 30, 2003, to Dec. 31, 2022. Over this period, the S&P 900 Dividend Revenue-Weighted Index posted a total return of 540.75% and a price return of 159.35%. Over the same period, the S&P 900 generated a total return of 489.32% and a price return of 303.49%.

As of Dec. 31, 2022, the S&P 900 Dividend Revenue-Weighted Index’s trailing one-year dividend yield was 3.99%, versus 1.74% for the S&P 900. Such dividend yield advantage, compounded and reinvested over many years, is a key determinant for the long-term total return outperformance of the S&P 900 Dividend Revenue-Weighted Index compared with its benchmark.

Historical Performance in High-Inflation Environments

Given the current inflationary environment, it is important to understand how the S&P 900 Dividend Revenue-Weighted Index has historically performed relative to its benchmark in similar economic climates. High-inflation periods are defined as at least 10 consecutive months where the year-over-year CPI rate exceeds 3%. Exhibit 3 shows that the S&P 900 Dividend Revenue-Weighted Index outperformed its benchmark in all four recent inflationary environments.

Sector Composition

Over the long term, Exhibit 4 shows that the S&P 900 Dividend Revenue-Weighted Index was overweight in the Utilities and Communication Services sectors (driven by the Telecommunication Services and Media industries) and underweight in Information Technology, Industrials and Health Care.

Factor Exposure

From a long-term factor perspective, the S&P 900 Dividend Revenue-Weighted Index has demonstrated a value tilt, as shown in Exhibit 5. Using Axioma Risk Model Factor Z-scores from June 30, 2003, to Dec. 31, 2022, the S&P 900 Dividend Revenue-Weighted Index had higher exposure to the book-to-price and dividend yield factors, similar exposure to earnings yield and lower exposure to growth factors such as sales and earnings growth when compared with the S&P 900.

Conclusion

The S&P 900 Dividend Revenue-Weighted Index has demonstrated solid outperformance over the long term, as well as in previous and current inflationary environments. Additionally, its emphasis on dividend yield and value could offer investors more protection against rising interest rates relative to its benchmark. For market participants who believe that the current economic environment may persist, the S&P 900 Dividend Revenue-Weighted Index might be an option worth considering.

The posts on this blog are opinions, not advice. Please read our Disclaimers.