Take a deep dive into the low volatility anomaly as S&P DJI’s Craig Lazzara explains what the anomaly is, when and why it outperforms, and the role of dispersion in identifying potential opportunities.

https://youtu.be/KyLkQPxtSi4

The posts on this blog are opinions, not advice. Please read our Disclaimers.

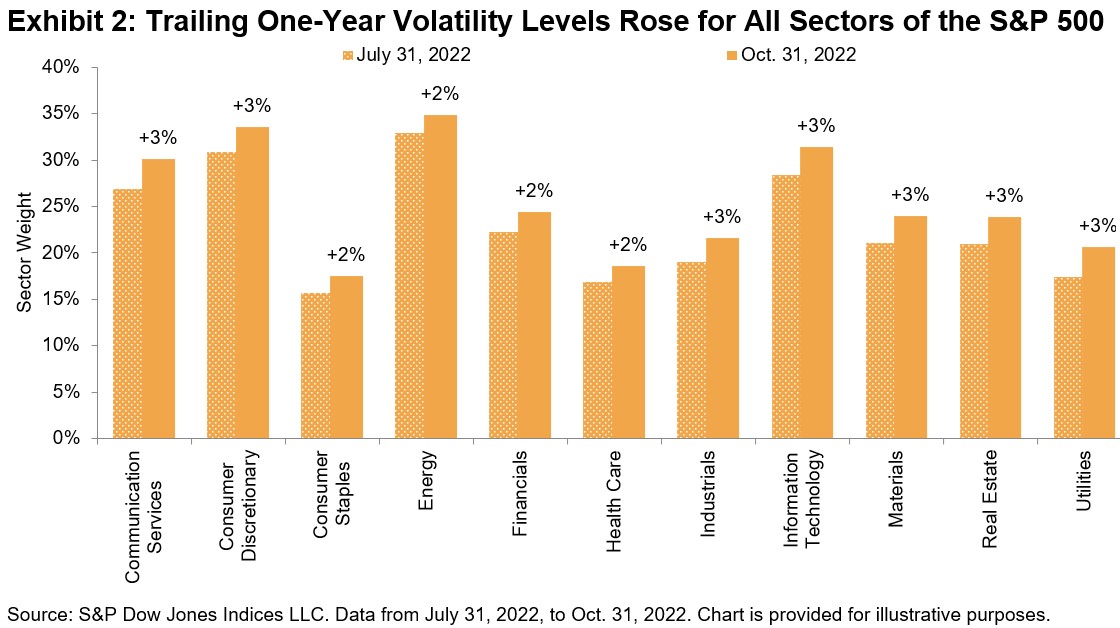

Since August, volatility has risen for all S&P 500 sectors, with Consumer Discretionary and Energy maintaining their status as the most volatile sectors.

Since August, volatility has risen for all S&P 500 sectors, with Consumer Discretionary and Energy maintaining their status as the most volatile sectors.

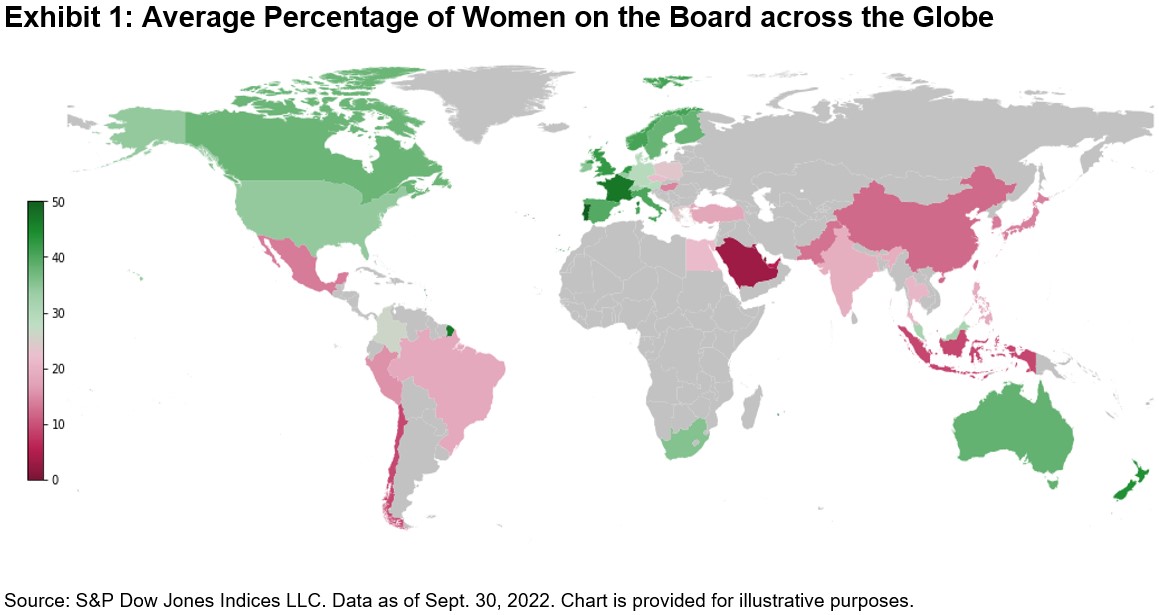

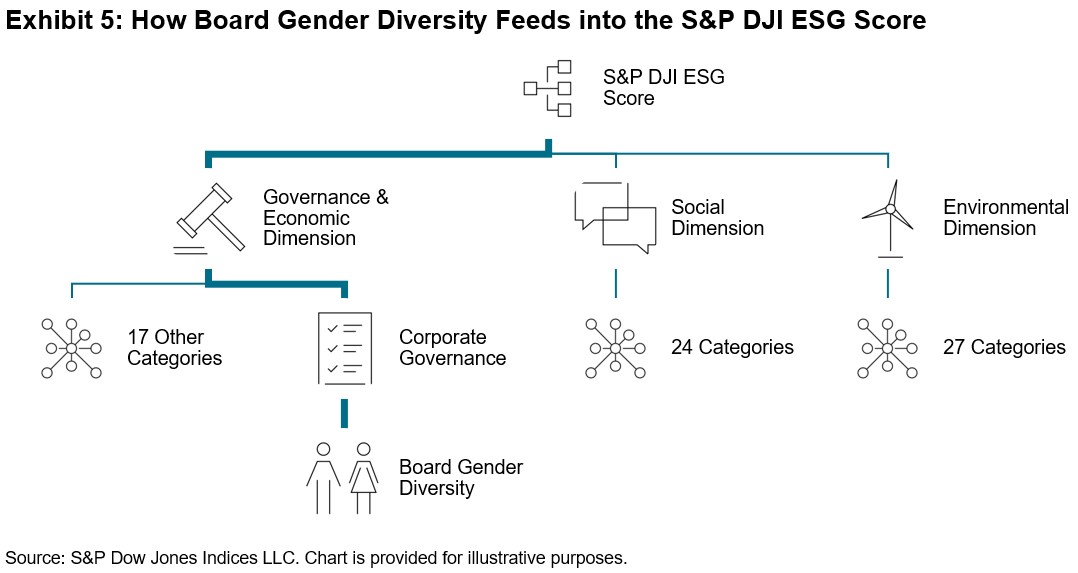

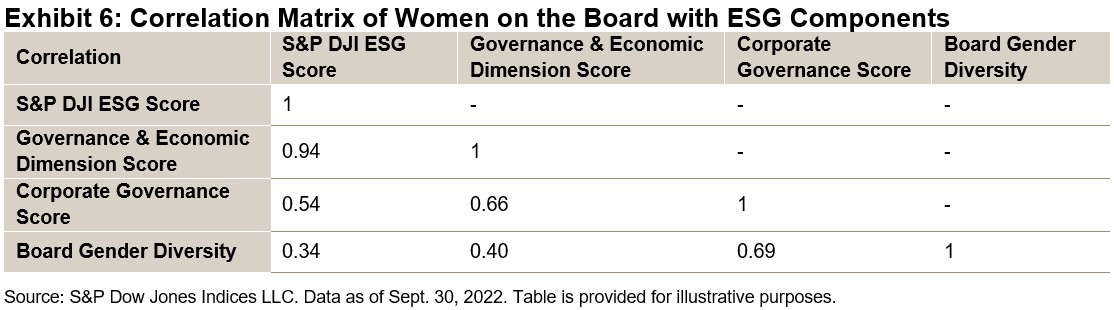

Exhibit 6 demonstrates the influence that women on boards of directors can have on each dimension of a firm’s S&P DJI ESG Score. Even at the overall ESG score level, board gender diversity still plays a part in a company’s overall sustainability rating.

Exhibit 6 demonstrates the influence that women on boards of directors can have on each dimension of a firm’s S&P DJI ESG Score. Even at the overall ESG score level, board gender diversity still plays a part in a company’s overall sustainability rating.