Just over four months after its launch (on Nov. 8, 2021), the S&P/BVL Peru General ESG Index experienced its first annual rebalancing, effective after the market close on the last business day of April 2022.

The S&P/BVL Peru General ESG Index is the first index of its kind in the Peruvian market, measuring the performance of Peruvian companies from the headline S&P/BVL Peru General Index that meet high standards of sustainability criteria.

The Peruvian stock exchange (BVL) recognizes and rewards companies that qualify for the S&P/BVL Peru General Index by granting them a discount on BVL and Cavali fees as an incentive to improve their S&P DJI ESG Scores.

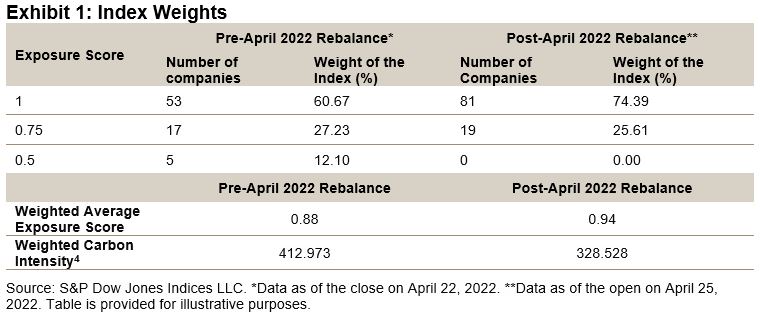

For those who are not familiar with the methodology, we summarize it in Exhibit 1.

We start by excluding from the universe (the S&P/BVL Peru General Index) what the methodology classifies as contrary to general ESG values; then we select all companies whose S&P DJI ESG Score is equal to or greater than the universe median score. The companies are then weighted according to their float-adjusted market capitalization (FMC), subject to certain concentration limits.

The index is rebalanced once per year, effective after the market close of the last business day of April, and has a reweight after the close of the last business day of October. As of the 2022 rebalance, 17 out of 29 constituents made it into the S&P/BVL Peru General ESG Index, as three new participants were added and one was removed.

The S&P DJI ESG Score of the S&P/BVL Peru General ESG Index increased from 52.68 to 62.27, an improvement of 9.58 points; considering that the maximum attainable ESG score of the S&P/BVL Peru General Index is 95.86, the ESG realized potential was 22%.

In its short existence, the performance of the S&P/BVL Peru General ESG Index exhibited different results compared to its benchmark (see Exhibit 4).

CONCLUSION

The S&P/BVL Peru General ESG Index is designed to measure the performance of securities in the S&P/BVL Peru General Index that sustainability criteria. As sustainable investment themes garner more interest, companies that incorporate ESG considerations have the potential to benefit in terms of public perception.

The posts on this blog are opinions, not advice. Please read our Disclaimers.