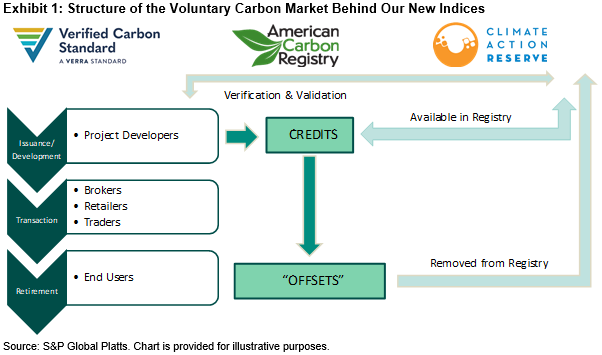

The S&P GSCI Nature-Based Global Emissions Offsets and the S&P GSCI Global Emissions Offsets are the first two indices launched by S&P DJI that are based on voluntary carbon markets. The first compliance-based index, the S&P GSCI Carbon Emissions Allowances (EUA) was launched two years ago and tracks the EUA futures based on the European Union’s emissions trading system. Our two new indices bring transparency to a fast growing and highly important new commodity directly tied to the green transition. In contrast to compliant markets like EUAs, voluntary carbon markets are not government mandated, but go through stringent verification and validation channels to ensure underlying projects do indeed have an impact—whether that be reforestation, avoided deforestation, renewable energy, or carbon capture, among others. The S&P GSCI Nature-Based Global Emissions Offsets tracks the CBL Nature-Based Global Emissions Offset (NGO) futures underpinned by the Verified Carbon Standard registry. The S&P GSCI Global Emissions Offsets tracks the CBL Global Emissions Offset (GEO) futures, allowing delivery from CORSIA-eligible carbon offset credits from all three registries displayed in Exhibit 1.1 Both futures contracts are traded at the CME.

The underlying futures contracts from the CME are some of the newest offerings in the carbon market. The speed with which liquidity has built in these contracts echoes the uptake in Bitcoin futures during 2021. Similar to other carbon markets and several other commodities late last year, the voluntary carbon markets experienced significant price appreciation as liquidity and interest drove prices higher. As of Feb. 22, 2022, these two new indices returned more than 200% within only a few months of trading on the underlying futures contracts (see Exhibit 2).

There is significant demand for liquid alternatives in the current market environment, especially for options that allow market participation in the energy transition. Due to the low daily correlations to other carbon markets and other major assets classes, voluntary emissions offsets may offer diversification and potential reduction of overall portfolio risk. Exhibit 3 highlights the low correlations these two new indices demonstrate compared to the European compliance scheme, as well as broad commodities and equities.

Regardless which path the global energy transition takes, transparent and liquid carbon markets are an essential component. There are many hurdles to overcome in this multi-generational shift in global energy consumption, but currently lower-cost resolutions like voluntary carbon markets could continue to gain importance as the most frictionless solution for many market participants. For more information, visit our commodities investment theme page and check out S&P Global Platts’ energy transition resources.

1https://verra.org/project/vcs-program/

https://www.climateactionreserve.org/how/voluntary-offset-program/

The posts on this blog are opinions, not advice. Please read our Disclaimers.