Introducing the S&P Kensho Moonshots Index – Next-Generation Innovators

Innovation risk ranks as one of the most significant existential threats faced by companies today. The Fourth Industrial Revolution, and the attendant widespread disruption to the global economy, has significantly amplified an already established trend: accelerating change and the ever-decreasing lifespans of companies, or what the economist Joseph Schumpeter aptly described as ”creative destruction.” To wit, according to Innosight, the average tenure of a company in the S&P 500® is forecast to be just 12 years in 2027, down from 24 years in 2016—many companies are simply unable, or unwilling, to adapt fast enough to stay ahead of the curve.

Given this backdrop of exponential innovation and disruption, it has become more essential than ever for market participants to adopt a quantifiable framework with which to understand and measure innovation—not just in terms of identifying next-generation products and services and the companies producing them (for these, please review the S&P Kensho New Economies), but also to assess a company’s propensity for innovation. This may be considered from three perspectives:

- How “innovation-oriented” the company’s mission and culture are;

- How many resources the company is allocating to innovation; and,

- How successful the company is in executing its innovation strategy.

Using a rules-based, proprietary framework, we have developed innovation factors that quantify each of these elements, providing market participants with a unique and critical tool for navigating the rapidly changing corporate and technological landscape.

The S&P Kensho Moonshots Index is the first in a series of indices to leverage these novel innovation factors. This index seeks to capture the most innovative companies that are still relatively early in their gestation. It consists of the 50 U.S.-listed companies with the highest Early-Stage Innovation Score that produce next-generation products and services. The Early-Stage Innovation Score1 is the product of innovation factors 1 and 2 listed above and provides a quantitative measure for a company’s commitment to innovation, notwithstanding that it may be early in its lifecycle and still in the process of developing its product portfolio. Large companies are also screened out, emphasizing the focus on emerging innovators.

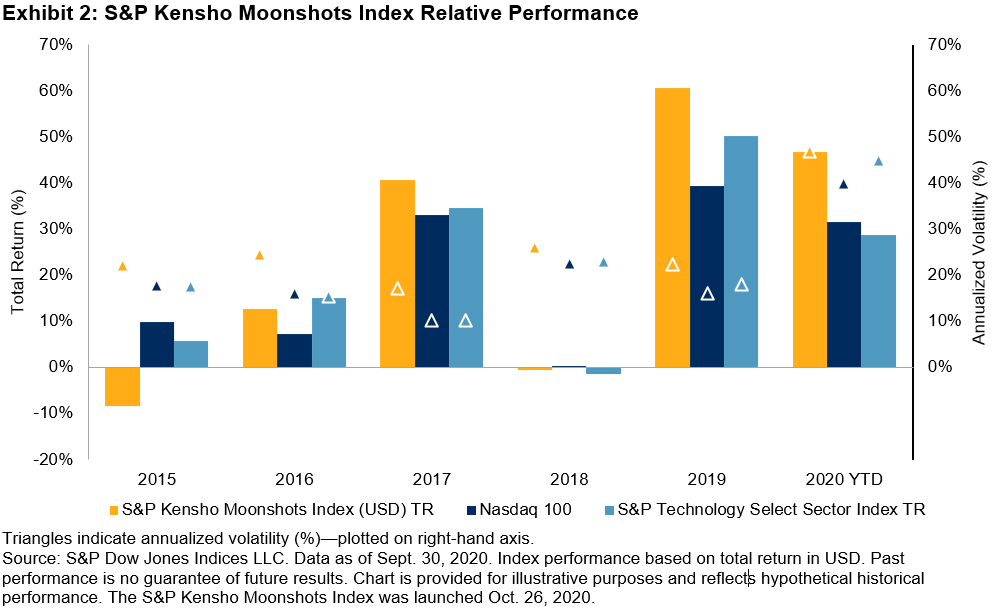

The performance characteristics of the S&P Kensho Moonshots Index (see Exhibit 1), and its relative outperformance, reflect the dynamic nature of its constituents; it is consistent with the higher risk/return profile typically expected, but rarely seen, in private equity or hedge funds.

Exhibit 2 illustrates the consistency of outperformance over the past five years, another quality rarely found in either active or private equity or hedge funds.

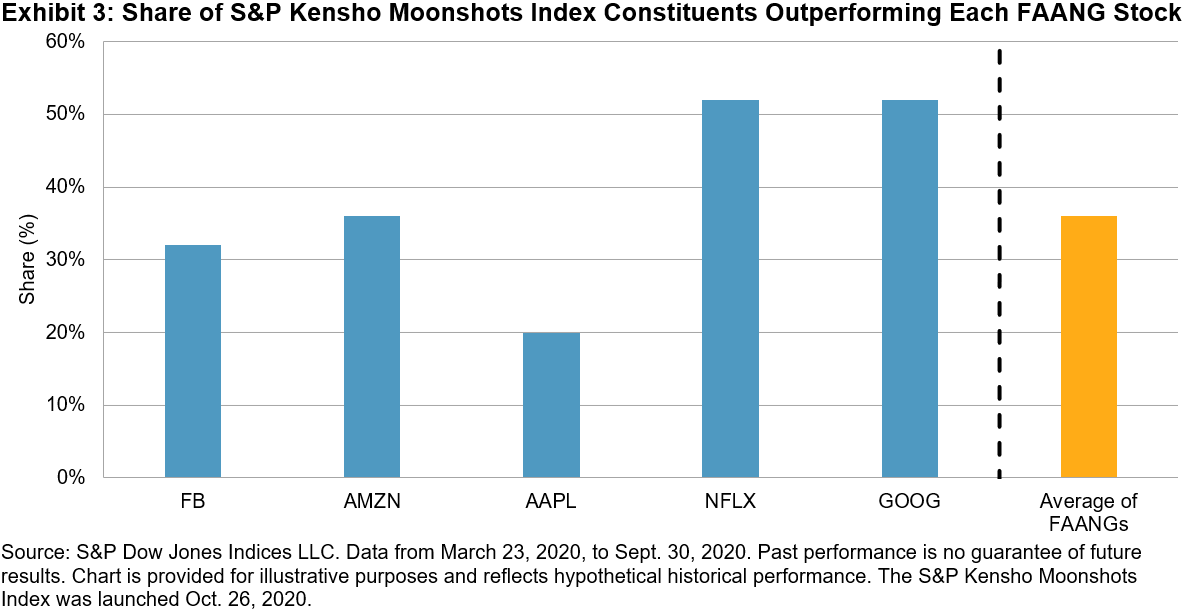

By construction, the S&P Kensho Moonshots Index excludes the mega-cap tech names, instead focusing on the next generation of innovators (90% of constituents have a market capitalization of less than USD 10 billion); it is also equal weighted, limiting concentration risk. While the mega-cap tech companies are often considered the bellwethers of innovation, it is instructive to note that 36% of constituents of the S&P Kensho Moonshots Index outperformed the average returns of the FAANGs since the market bottom on March 23, 2020 (see Exhibit 3).

In part 2 of this blog, we will explore the S&P Kensho Moonshots Index’s focus on smaller companies, how effective it is at identifying those ground-breaking companies, and what happens to them once they leave the index.

The author would like to thank Adam Gould, Senior Director, Research and Quantitative Strategist, S&P Global for his contribution to this blog.

1 To learn more about the Early-Stage Innovation Score, please visit the S&P Kensho Moonshots Index Methodology.

The posts on this blog are opinions, not advice. Please read our Disclaimers.