ESG momentum shows no signs of stopping, with sustainable fund assets nearing USD 2 trillion, following record inflows in Q1.1 Pressure on firms to perform in sustainability rankings has never been higher, as Wall Street’s hottest topic gets hotter still. But what firms benefit from all this heat? From the assets flowing into S&P 500® ESG Index related products,2 it seems the balance of power may be shifting. At least for the foreseeable future, Sustainability is King (or Queen). So, by almost royal decree, here are the results of the 2021 S&P 500 ESG Index annual rebalance.

What’s changed? First, the methodology itself—with the introduction of a new thermal coal screen last September following public consultation. Even though the index still aims to offer similar overall industry group weights to the S&P 500, with sustainability enhancements—rather than reduce carbon exposure, per se—it experienced a welcome decrease of 12% in carbon intensity since the last annual rebalance.3

ADDITIONAL INDEX-LEVEL METRICS

A broader sustainability lens reveals that the index achieved an S&P DJI ESG Score improvement of 8% (at the index level), representing 23% of the overall ESG-improvement potential, given the sustainability characteristics of the starting universe.4 Within the underlying E, S, and G dimensions, the sustainable counterpart to the S&P 500 realizes numerous tangible enhancements, all while providing similarly broad U.S. equity exposure. Due to the depth and breadth of topics covered in the S&P Global Corporate Sustainability Assessment that underpins the S&P DJI ESG Scores, there are too many to demonstrate here, though a sample is provided in Exhibit 1. Such improvements are even more pronounced within industry groups, given the industry-specific nature of S&P DJI ESG Scores.5

CONSTITUENT SELECTION

What of the constituents? As of the 2021 rebalance, 315 constituents made it into the S&P 500 ESG Index, as 190 constituents were not included (79 were ineligible and 111 were eligible but not selected). As per the S&P 500 ESG Index methodology, companies might not qualify because they are: (a) ineligible according to certain ESG exclusionary criteria; or (b) simply not selected, even if they are eligible, because of poorer relative S&P DJI ESG Score performance than their index industry group peers. Exhibit 2 highlights how the S&P 500 translated into the composition of S&P 500 ESG Index in 2021.

As for major changes, Exhibit 3 highlights the biggest new additions and drops in terms of market capitalization. Other household names that made it into the sustainable index include Ford Motor Crop, News Corp, Marriott, and Etsy. Meanwhile, Lumen Technologies, L Brands, UDR, and Sealed Air Corp were among those that were removed despite being eligible, due to relatively poor S&P DJI ESG Score performance than their peers. Other names, such as Atmos Energy, Allegion, and Fortune Brands Home & Security were dropped because they fell to within the bottom 25% of S&P DJI ESG Score rankings among their global GICS industry group peers, rendering them ineligible. In addition, Johnson & Johnson, 3M, and Dupont remained on the exclusion list, as they have not yet completed the penalty period for their involvement in material public controversies.7

Interestingly, though the rebalance generates ample turnover, 74 constituents of the S&P 500 have consistently not met the rules-based selection criteria of the ESG index since it launched in January 2019 (see Exhibit 4). Conversely, 207 companies have managed to maintain their position in the sustainable index since its launch (see Exhibit 5).

RESULTS & PERFORMANCE

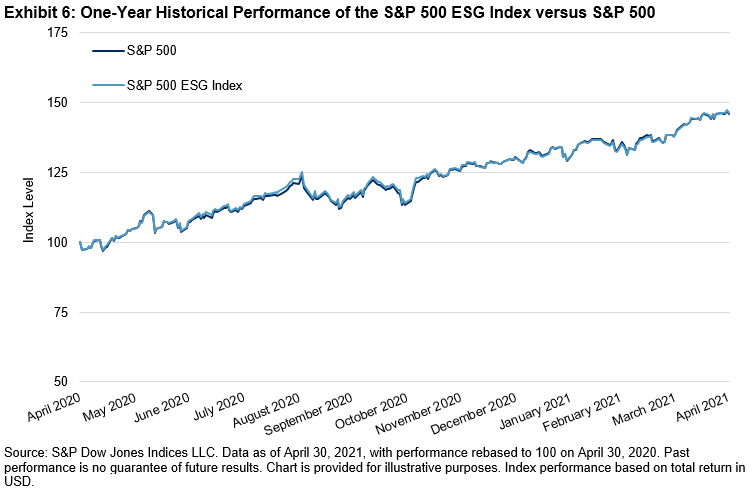

Despite containing just 75% of the S&P 500 market capitalization, the aforementioned sustainability improvements were achieved with only 1.11% of tracking error and excess returns of 0.67% over the past five years—in part, helping to dispel the myth of an inherent sustainability versus performance tradeoff. However, since the five-year return includes back-tested history that was built before the index was launched, it is worth paying special attention to the live performance record over the past one year, when it exhibited excess returns of 0.42% and 1.83% of tracking error (see Exhibit 6).

But can this outperformance be explained away by other factors?

PERFORMANCE ATTRIBUTION: A STORY OF SELECTION

Performance attribution primarily reveals a story of selection. It was generally because of the stocks selected according to their sustainability credentials, rather than differences in sector exposure, that appear to have driven this excess return. Indeed, this should come as no surprise, as the methodology lends itself by design to a broadly sector-neutral outcome. Thus, the outperformance was not all necessarily due to significant overexposure to Tech and underexposure to Energy, as many might assume.

FACTOR EXPOSURE: SPOT THE DIFFERENCE

A closer look at the underlying factor exposure also reveals that the factor tilts are in fact quite similar to the S&P 500, save for a minor discrepancy in its exposure to larger firms.9 These similarities are consistent with the ESG index’s objective to provide a similar level of risk and return. As such, the absence of any sizeable unintended factor exposure cannot entirely explain this difference either—suggesting other “forces” are still potentially at work.

CONCLUSION

Though the aim of the S&P 500 ESG Index is not to outperform but provide exposure and performance broadly in line with the benchmark, these results show that a rules-based selection process, driven by ESG principles, has yielded greater exposure to high-performing companies. And so, without other explanatory challengers to usurp the performance throne, long may the reign of our sustainability monarch continue.

APPENDIX A

APPENDIX B

1 Source: https://www.morningstar.com/lp/global-esg-flows

2 As of March 30, 2021, there is USD 4 billion of AUM in ETFs tied to the S&P 500 ESG Index, with more than half a billion USD of net new inflows in Q1 2021 alone.

3 Calculated as the percentage difference between the weighted average carbon intensity (WACI) of the S&P 500 ESG Index as of the rebalance dates in 2020 and 2021, measured in metric tons of CO2e per USD 1 million of revenues using S&P Global Trucost data.

4 The realized ESG potential depicts how much of the S&P DJI ESG Score improvement was achieved by the ESG index, relative to the maximum possible improvement that could in theory have been attained by investing solely in the single highest-ranked company by S&P DJI ESG Score. While diversification requirements would render this approach undesirable in practice, it is nevertheless an interesting metric to contextualize the S&P DJI ESG Score improvement relative to the starting characteristics of the benchmark universe. For example, in markets where companies are generally sustainable to begin with, it is harder to obtain a substantial S&P DJI ESG Score increase without incurring a sizeable loss of diversification or higher levels of tracking error.

5 Due to the industry-specific nature of the S&P DJI ESG Scores, driven by a materiality-weighted scoring framework, the aggregate S&P DJI ESG Score improvement metrics vary considerably by sector. For example, the S&P DJI ESG Score improvement for the Materials sector and Real Estate sectors both came to approximately 11%; whereas the improvement among the IT and Health Care sectors both came to approximately 6%, relative to the S&P 500. However, it is among the underlying ESG indicators where we find the greatest discrepancies in performance between industry groups, though the methodology accounts for too many data points (600-1,000 data points per company) to feasibly showcase here.

6 As the methodology prevents companies removed for this reason (at the discretion of the Index Committee) from reentering the index for one full calendar year.

7 See Appendices A and B for a detailed explanation of these changes.

8 S&P DJI ESG Scores are normalized by industry group and thus designed to be read as percentiles. For example, a company score of 70 means that this company has a higher score than 70% of its peers within its industry group. This allows for a comparison of relative rankings of companies across different industry groups, despite the industry-specific nature of S&P DJI ESG Scores.

9 This is unsurprising due to the generally positive correlation between sustainability performance and firm size, as visibility, access to resources, and operating scale are typically associated with large firms.

The posts on this blog are opinions, not advice. Please read our Disclaimers.