In 2020, the 21st rebalancing of the Dow Jones Sustainability Indices (DJSJ) occurred; however, this is the first time it has taken place solely under the umbrella of S&P Global (after S&P Global’s acquisition of RobecoSAM’s ESG Ratings business in January 2020). It also marked a new step forward toward greater transparency and insight, as S&P Global announced to companies that they would be receiving a new level of granularity in their results—scores on up to 120 individual questions and metrics in the Corporate Sustainability Assessment (CSA). The 2020 CSA saw a number of key updates to the methodology, including the addition of specific questions on plastic waste, revised questions on ESG-focused products and services in the financial industry, and the extension of information security questions to a broader set of industries. These topics reflect the shifting landscape of investor interest as it relates to ESG and challenge companies to think about emerging topics as they begin to materialize in the form of new risks or opportunities. While we saw strong improvements in some areas, we also saw that companies across many industries continue to struggle on topics such as cybersecurity. From a governance perspective, fewer than 20% of companies across all industries have board members with relevant cybersecurity or IT experience. New questions introduced in the pharmaceuticals industry highlighted that few companies publicly report on information related to fair drug pricing, another topic that is certainly likely to gain increased attention as a result of the ongoing global health crisis.

This year, despite the ongoing global challenges, we saw an increase of nearly 19% in the number of companies completing the CSA, bringing the total number of CSA participants to 1,386. This is the highest number in the DJSI’s more than 20 years of history and the biggest year-over-year increase, ever. Reassuringly, we saw growth across all regions, despite the different local economic and political challenges that companies faced. Reflecting on past years, it would seem that crises serve as a strong driver to bolster sustainability agendas. Between 2008 and 2009, we saw an increase in company participation of nearly 15%, the second highest record in DJSI history. Interestingly, the Financial sectors drove much of this growth. In 2020, the Real Estate and Financial sectors demonstrated the highest growth rate—a clear sign that ESG is at the top of the agenda for financial institutions as they brace for new regulations and requirements for ESG disclosure—at both the company level and in their ESG product portfolios.

For more detailed information on this year’s DJSI rebalance and key highlights from the CSA, please read our insight. For more detailed information and findings from this year’s results, please read our Annual Scoring & Methodology Review.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

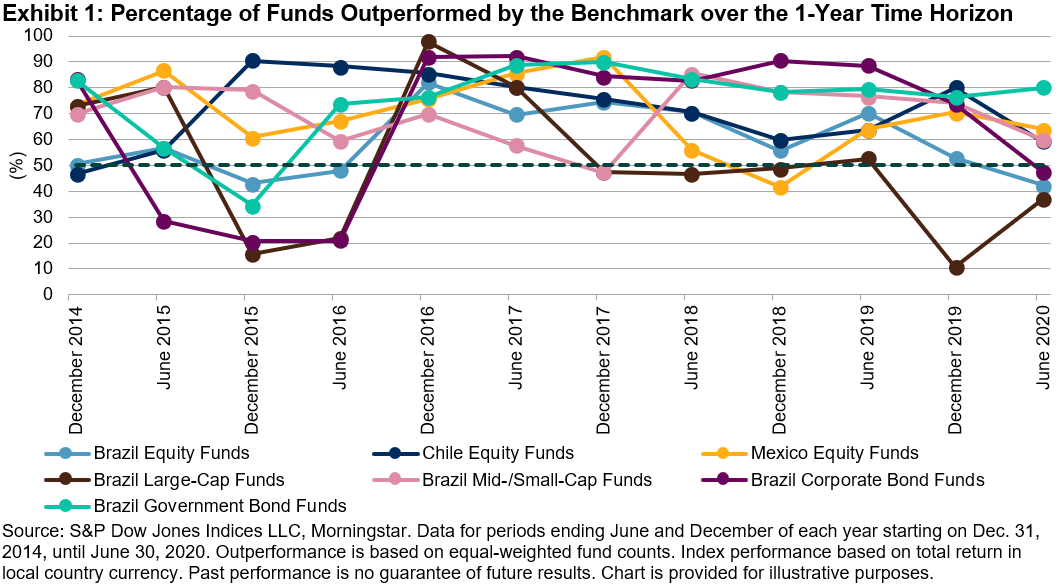

However, when compared with a longer time horizon, say a three-year period, we see that the percentage of active managers outperforming goes down.

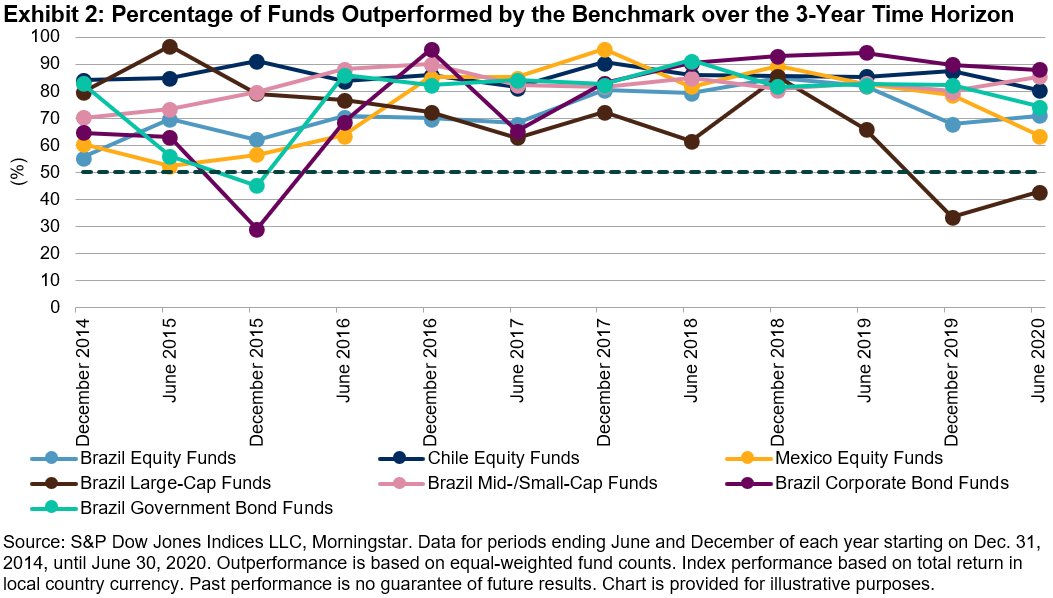

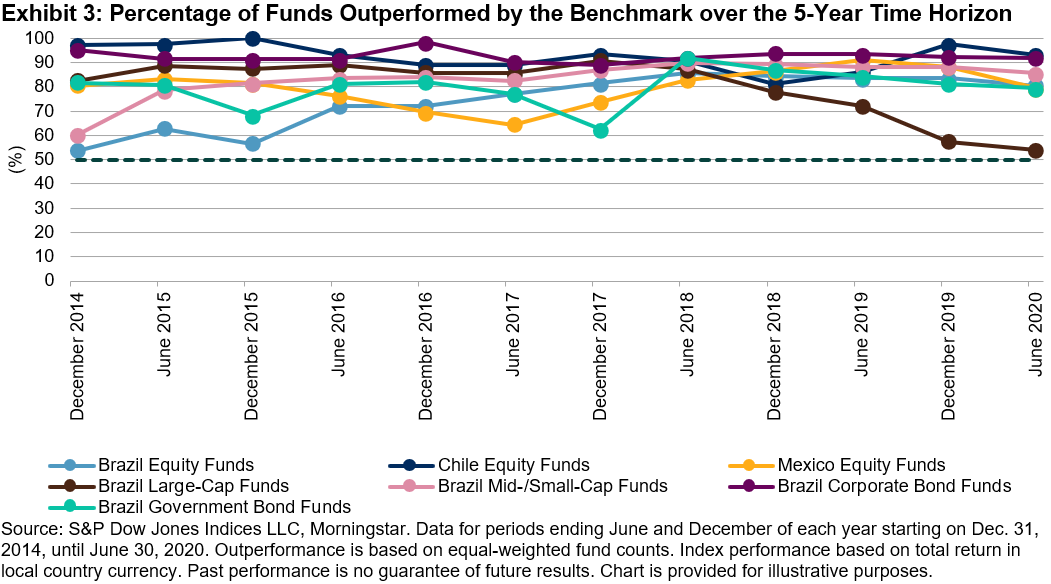

However, when compared with a longer time horizon, say a three-year period, we see that the percentage of active managers outperforming goes down. And when considering even longer time periods, like across a five-year period, the majority of active managers in all categories for all three countries were outperformed by their benchmarks.

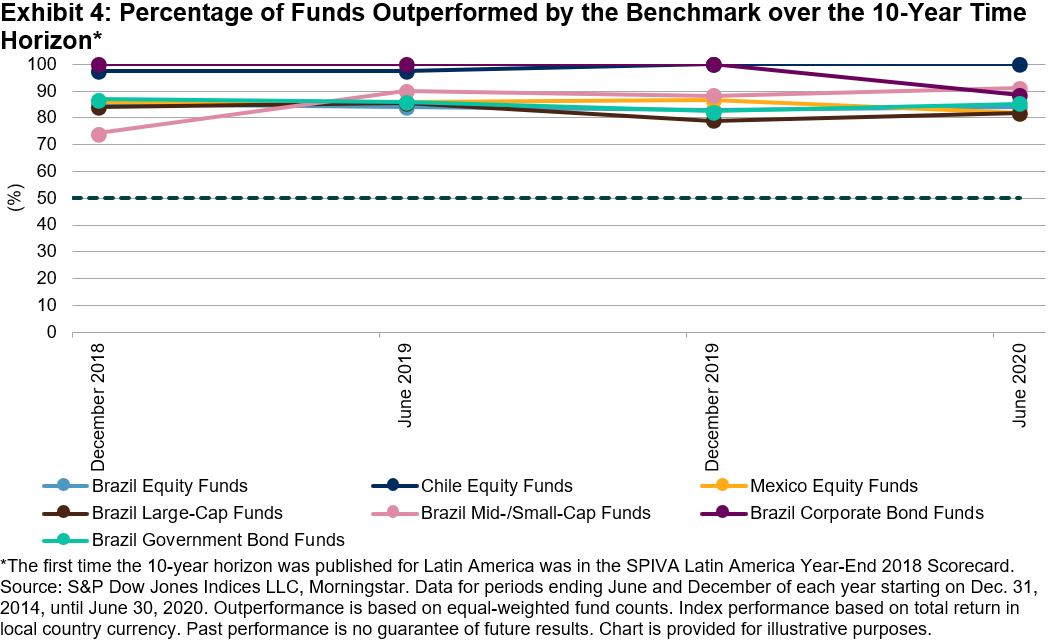

And when considering even longer time periods, like across a five-year period, the majority of active managers in all categories for all three countries were outperformed by their benchmarks. Lastly, for the 10-year period observed, the percentage of funds outperformed by their benchmarks converged in a range above 70%.

Lastly, for the 10-year period observed, the percentage of funds outperformed by their benchmarks converged in a range above 70%. As evidenced by the SPIVA scorecards, the majority of active managers underperform most of the time, especially across long-term horizons, demonstrating how difficult is to consistently beat the benchmark.

As evidenced by the SPIVA scorecards, the majority of active managers underperform most of the time, especially across long-term horizons, demonstrating how difficult is to consistently beat the benchmark.