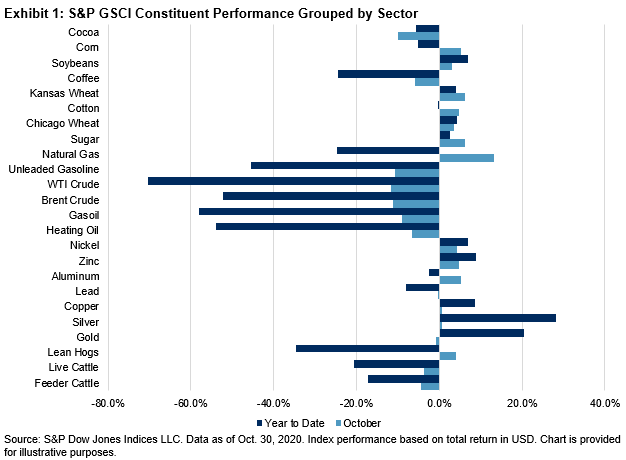

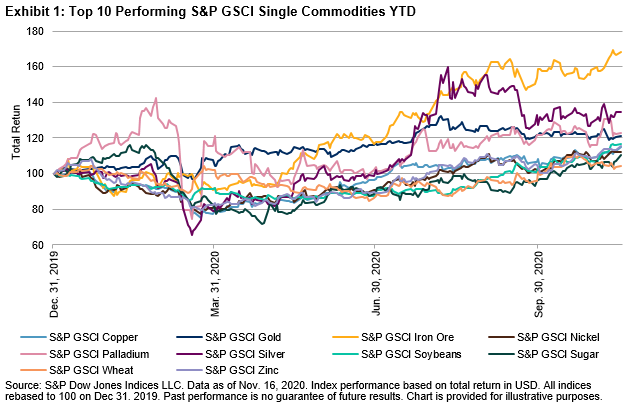

When discussing global economic recoveries, China is usually at the forefront of the conversation. As of Nov. 16, 2020, metal commodities with an industrial focus were the outperformers YTD. China is the world’s top industrial metal destination. Exhibit 1 shows the top 10 performing commodities tracked by S&P DJI. Seven metal commodities made it to the top 10. Recent rebounds in economic data points like PMIs and Industrial Production point to an increased appetite from China for these industrial commodities compared to what was witnessed during the doldrums of the COVID-19 global lockdown earlier this year, as well as any time over the last two years.

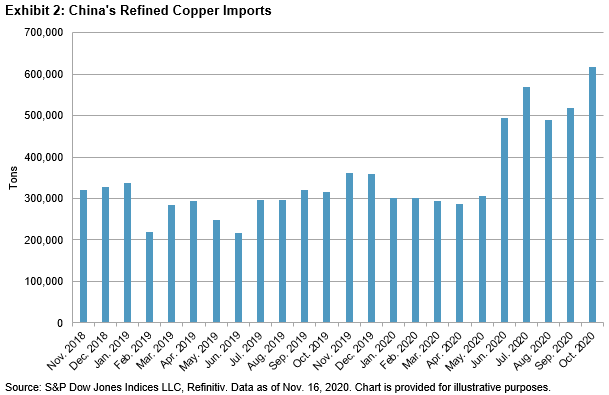

The S&P GSCI Iron Ore outperformed all other commodities, up 68.19% YTD. Chinese steel production and stockpiling played a big role in the demand for iron ore. With its higher industrial use, silver has outshined gold so far, with a 34.39% YTD return compared to 20.87% for the latter. The five LME-based commodities making up the S&P GSCI Industrial Metals are performing admirably, with the S&P GSCI Copper up 14.77% YTD. China’s demand for copper picked up considerably this year starting in June, and it remained elevated through the end of October. With two months of the year left, China has already imported a YTD record high 5.6 million tons of copper, outpacing 2015 by several thousand tons.

China’s increased appetite for feed grains pushed several major agriculture commodities to multi-year highs, as livestock populations rebounded impressively this year after last year’s decimation from African Swine Fever. In a previous blog, we highlighted the reasons behind the S&P GSCI Soybeans strong YTD performance. Its use as a source of feed appealed to Chinese buyers, especially as the commodity traded near five-year lows earlier this year and the U.S.-China trade war showed signs of a resolution; China committed to a record high level of purchases of U.S. soybeans this sowing season. China is on pace to shatter all previous grain purchasing records. More recently, local corn prices in China were pushed to record highs. A domestic shortfall of corn stocks led China to go on a buying spree over the last few months.

Despite attempts by the Communist People’s Party to become more self-sufficient in the grain markets, this year demonstrated how reliant they are on key commodity markets. China’s 14th Five-Year Plan clearly exposed which commodities they will focus on over the next five years. As China enters a new stage of development, this latest five-year plan shows the country’s determination to position itself as a world leader in emerging technologies, with more novel commodities like rare earth metals being a growing focus.

S&P DJI offers a suite of broad and single-commodity indices tracking commodity prices around the world. Explore our Commodities Indices to find out more about the strategies and insights we offer.

The posts on this blog are opinions, not advice. Please read our Disclaimers.