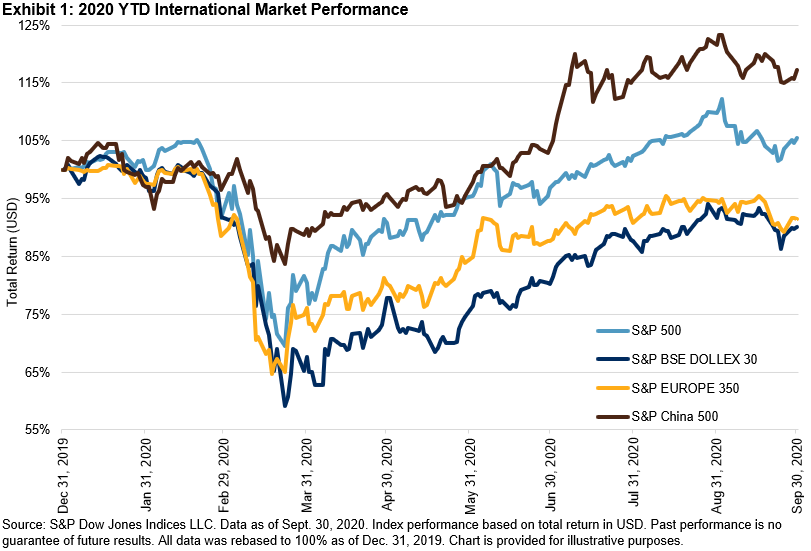

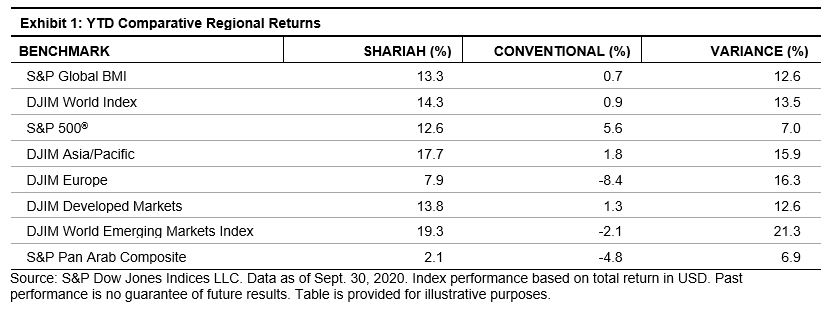

Global equities withstood a slump in the last month of the quarter, ultimately gaining 8.1% in Q3 2020 and entering positive territory YTD, as measured by the S&P Global BMI. Meanwhile, Shariah-compliant benchmarks, including the S&P Global BMI Shariah and Dow Jones Islamic Market (DJIM) World Index, significantly outperformed conventional indices, ultimately gaining an advantage of 13.3% and 14.4% YTD, respectively. The outperformance trend played out across all major regions, with the DJIM World Emerging Markets Index leading the pack, providing an additional 21.3% return above the conventional benchmark.

Sector Performance as a Key Driver

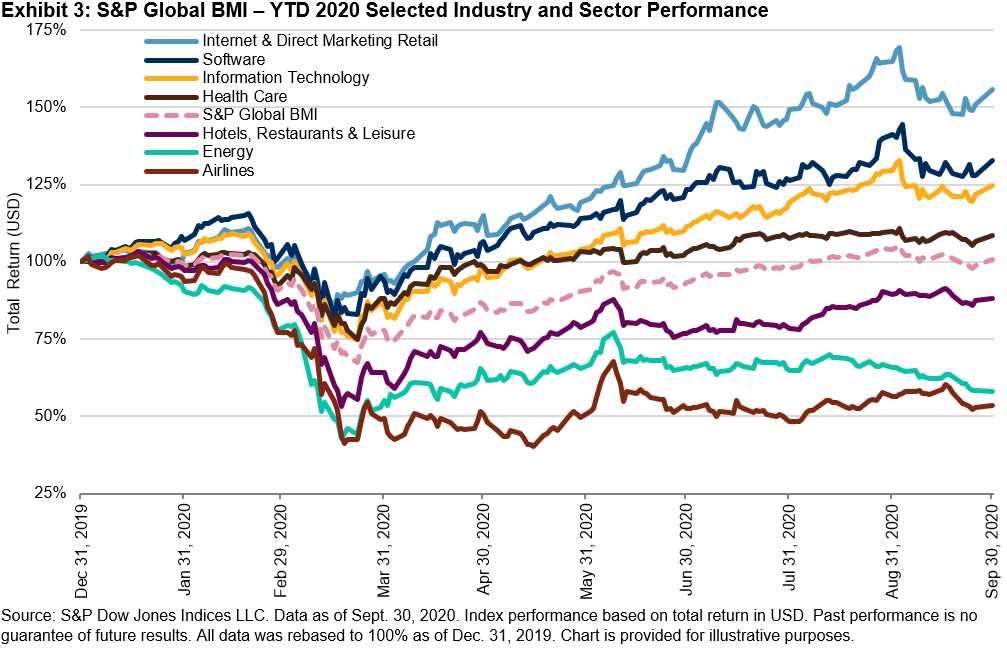

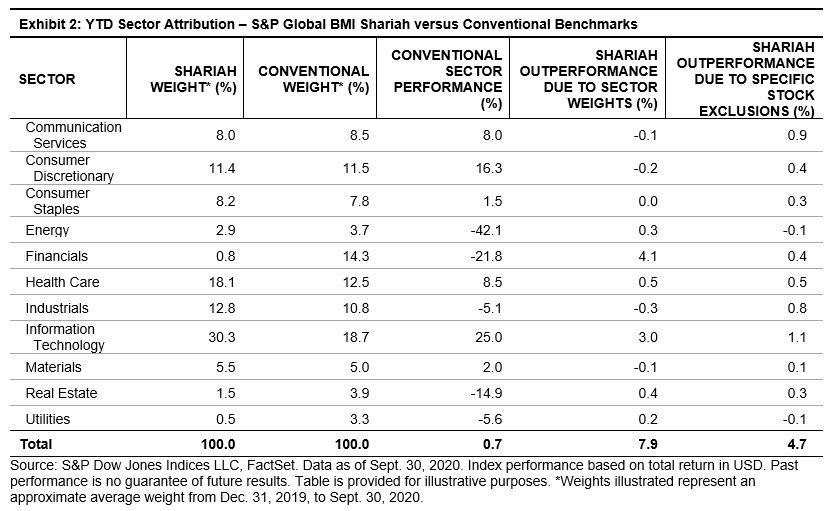

As global equities continued to recover in Q3 2020, sector drivers played an important role in Shariah outperformance as Information Technology—which tends to be overweight in Islamic indices—was the best performer among sectors, while Financials—which is nearly absent in Islamic indices—continued to heavily underperform the broader market. Exhibit 2 demonstrates the effect on returns of over- and underweight sector allocations of the S&P Global BMI Shariah compared to the conventional benchmark.

The majority of the outperformance—7.9% of the 12.6% total outperformance YTD—is explained by differing sector allocations, while 4.7% is explained by stock selection differences within sectors.

MENA Equity in Recovery

Having fallen significantly during Q1 2020, MENA equity performance improved considerably, as the S&P Pan Arab Composite was down 4.8% YTD, a welcome contrast since logging Q1 losses of 23.4%. The S&P Bahrain led the way in the region in Q3, gaining 17.8%, followed by the S&P Saudi Arabia, which gained 13.6%. All MENA country indices remained negative YTD, while the S&P Saudi Arabia was the closest to recovery, down just 0.01% YTD.

For more information on how Shariah-compliant benchmarks performed in Q3 2020, read our latest Shariah Scorecard.

A version of this article was first published in Islamic Finance News IFN Volume 17 Issue 41 dated the 14th October 2020.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

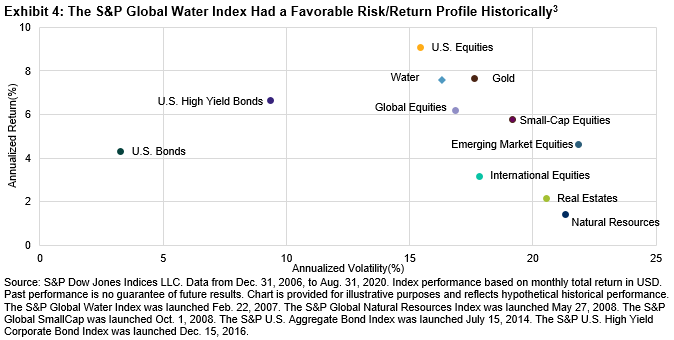

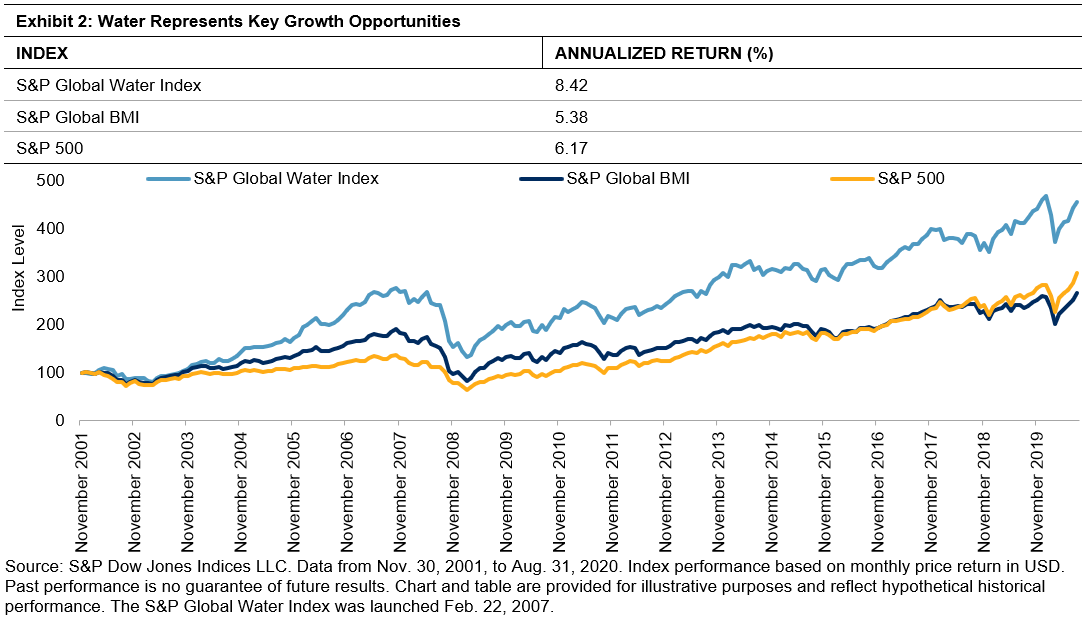

The S&P Global Water Index also provided favorable risk/return characteristics over the long run compared with key traditional asset classes, including real estate, small-cap equities, international equities, emerging market equities, and gold (see Exhibit 4). The favorable long-term risk/return characteristics compared with the

The S&P Global Water Index also provided favorable risk/return characteristics over the long run compared with key traditional asset classes, including real estate, small-cap equities, international equities, emerging market equities, and gold (see Exhibit 4). The favorable long-term risk/return characteristics compared with the