The long-term impact of the COVID-19 pandemic on commodities markets is not yet known. There have undoubtedly been short-term impacts on supply and demand, ranging from a collapse in oil demand to supply disruptions at individual mines as a result of COVID-19 infections among mine employees.

The longer-term implications of these demand and supply shocks, while uncertain, will likely follow a well-trodden path that eventually leads to market equilibrium. What is less clear is the long-term impact on the commodity investment landscape. The negative price action in the WTI crude oil futures market in April 2020 may well force investors to rethink the standard narrative around investing in commodities.

For investors, it is extremely difficult to access the return streams of physical commodities traded in the spot market. The closest approximation is a strategy that invests in rolling front-month futures contracts. That is exactly what the S&P GSCI Crude Oil does. The headline S&P GSCI series of indices follows a rolling schedule that ensures that futures positions roll to the following month’s contract well before the expiration of the current contract. This ensures that investors do not hold any exposure as a futures contract enters expiration, which is particularly important for commodity futures that allow for physical settlement.

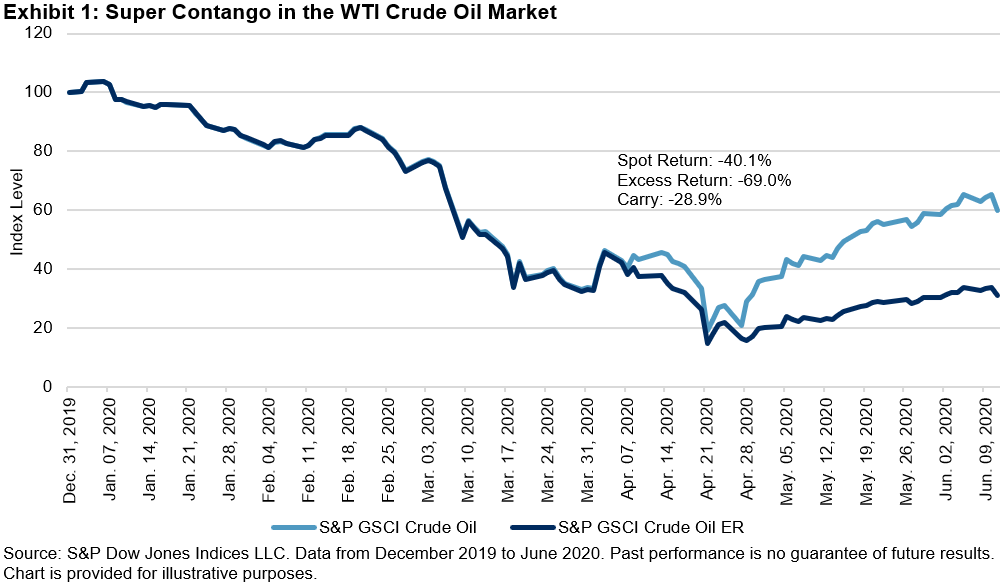

With that in mind, we examined the events that took place in the oil market in April and early May 2020. The S&P GSCI Crude Oil had already rolled into the June contract when the May WTI crude oil futures contract closed at USD -37.63 per barrel on the penultimate day of trading. The front-month rolling S&P DJI Commodities Indices that included WTI crude oil therefore did not directly contend with negative prices. Instead, they fell prey to the super contango in the WTI crude oil market.

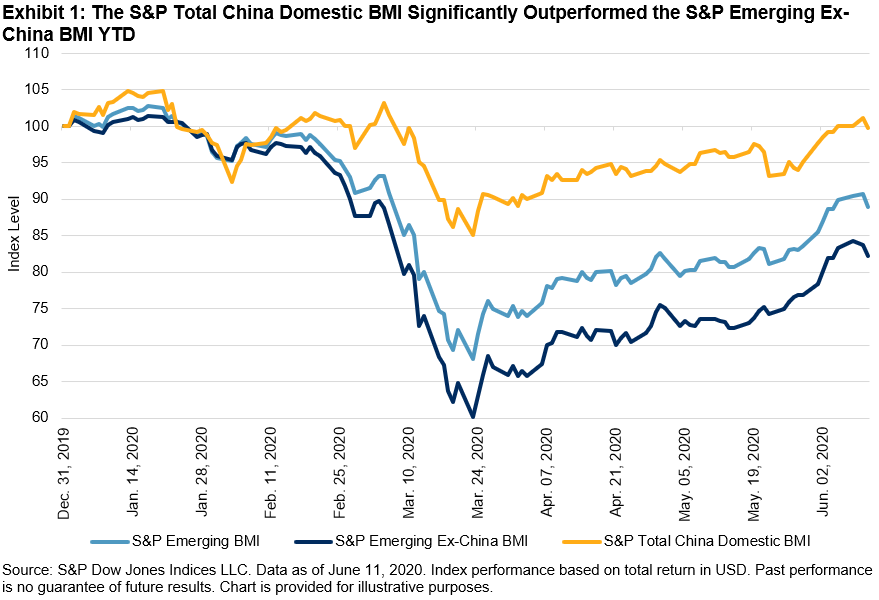

When a futures curve is in contango, investors pay to roll futures contracts. Commonly referred to as a negative roll yield, contango results in a significant drag on index performance. Super contango occurs when the spot price for a commodity trades substantially below the futures price. Super contango usually occurs when storage space becomes scarce due to excess supply—meaning that the cost of carry (the cost of storing a physical commodity) increases. Exhibit 1 presents the impact of super contango on the WTI crude oil market by illustrating the difference in performance between the S&P GSCI Crude Oil spot return and the S&P GSCI Crude Oil Excess Return (ER) since the beginning of 2020.

The overarching lesson for investors from the oil market is that there are additional risks when investing in products that replicate price movements on a futures curve. The risk is particularly acute in extreme conditions when returns associated with the underlying product become magnified as futures prices react to market conditions.

In short, market participants need to be aware of the unique return streams associated with futures-based investment strategies, especially the investment implications of holding long-only commodity positions at the front of the futures curve during periods of extreme market stress.

The posts on this blog are opinions, not advice. Please read our Disclaimers.