With the stock market in the midst of a historic slump, many investors may be looking to alternatives to protect against a prolonged downturn. The S&P Strategic Futures Indices are designed to measure the performance of passively constructed, liquid, and transparent solutions by spreading risk evenly across global futures markets utilizing a long/short trend-following strategy to deliver results with little correlation to traditional markets. The recent performance of these indices has reflected their usefulness in providing liquidity and capital preservation during broad market downturns (see Exhibit 1).

The unlevered risk of these indices has historically been nearly half that of U.S. equities (see Exhibit 2).

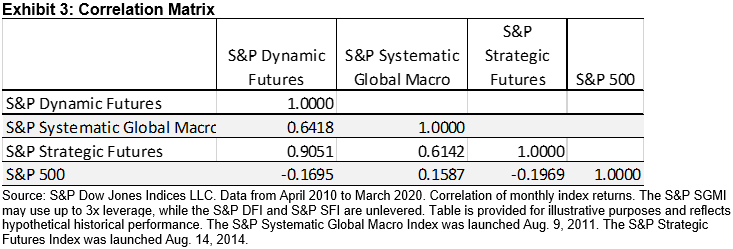

The S&P Systematic Global Macro Index (SGMI) has had a relatively modest correlation to the S&P 500®, while the S&P Dynamic Futures Index (DFI) and the S&P Strategic Futures Index (SFI) have been negatively correlated to equities (see Exhibit 3). Low and negative correlations can make these strategies attractive to investors looking to diversify their portfolios and preserve capital during periods of broad equity market stress.

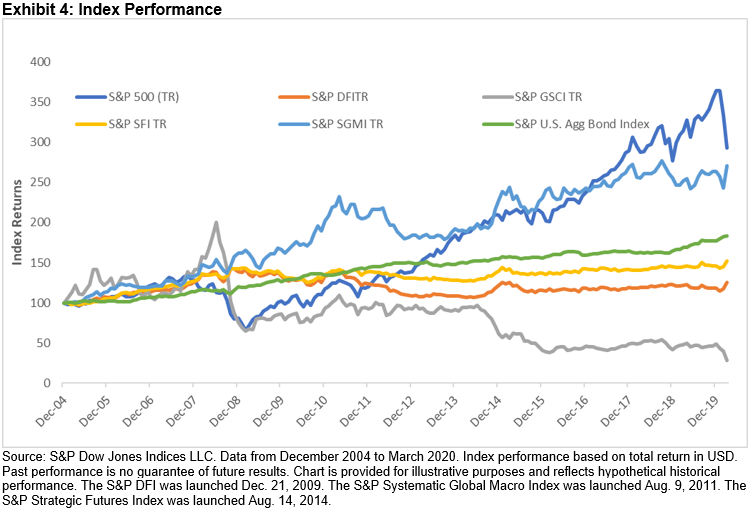

While the absolute performance of the S&P Managed Futures Indices was modest over most of the past decade, their performance during equity market drawdowns has been admirable. During the drawdown of close to 50% in the S&P 500 during the global financial crisis, all three indices rallied, and the same has occurred in the first quarter of 2020 (see Exhibit 4).

There are a number of advantages of passive managed futures strategies. Passive strategies may offer an enhanced level of liquidity and lower fees as compared with active managed futures strategies and other alternative strategies, such as real assets and private equity. The transparent, rules-based approach of passive managed futures strategies also improves the ease with which investors can track and benchmark relative performance. Style drift has become a major concern of investors in the managed futures space; many fear managers have made changes to their investment processes over recent years to improve short-term performance relative to the bullish equities market. Passive managed futures solutions based on an index eliminate the risk of style drift.

Finally, from a benchmark perspective, the S&P Strategic Futures Indices seek to represent the performance of a pure strategy, not the fund of fund approach adopted by other benchmarks that combine the actual performance of individual managed futures strategies.

The posts on this blog are opinions, not advice. Please read our Disclaimers.