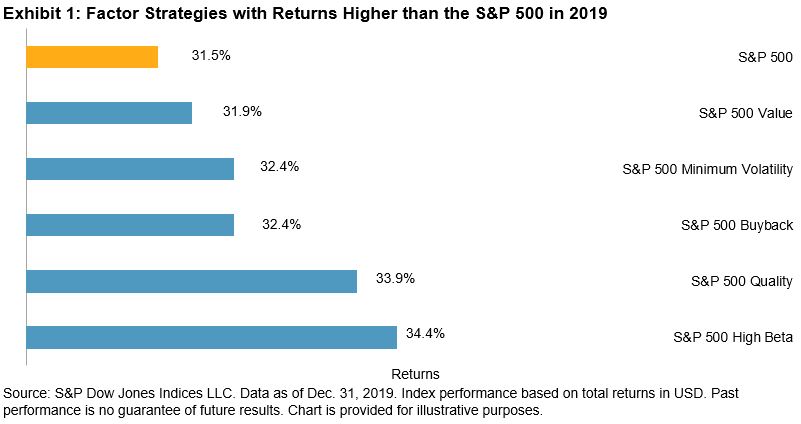

While the iconic S&P 500® is one of the world’s best known benchmarks, the S&P Composite 1500 (comprising the S&P 500, S&P MidCap 400®, and S&P SmallCap 600®) covers a broader spectrum of the capitalization of the U.S. equity market. Though the S&P 500 is often used as a measuring stick for large-cap fund performance (and rightly so), the S&P Composite 1500 can be a more appropriate benchmark for funds that are not limited to large-cap stocks.

The performance differences between the S&P 500 and the S&P Composite 1500 are not large, never fluctuating outside a 150 basis point annual spread from 2001 through 2018. The tight tracking is expected; the S&P Composite 1500 is also a market cap based index and as such, the S&P 500 would be the predominant sub index, typically accounting for more than 85% of the S&P Composite 1500. But almost without fail, the direction of the spreads of the S&P Composite 1500 are in sync with those of the S&P SmallCap 600 when measured against the S&P 500. When small caps outperform, the S&P Composite 1500 typically beats the S&P 500, and vice versa.

Our SPIVA scorecards measure the performance of active funds against an appropriate passive benchmark. The S&P Composite 1500’s wider capitalization range makes it an appropriate benchmark for multi cap funds as well as all general domestic funds. In both cases, fund managers underperformed the S&P Composite 1500 in 12 of the 18 years observed—and things have looked particularly bleak in each of the last five years. While 2019 results are not available yet, based on market dynamics, we’d expect the average active manager to underperform again.

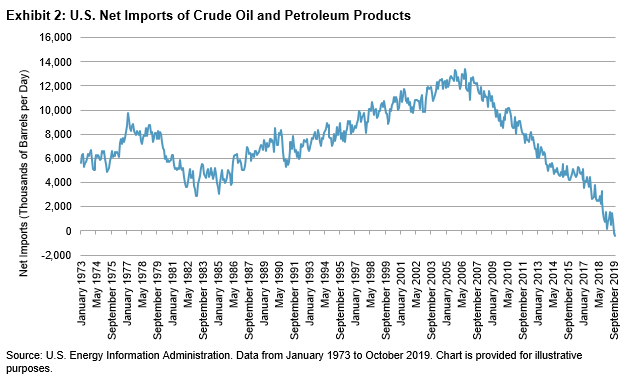

Taking market performance as a measure, there has been little visible dent to investors’ confidence from the most recent geopolitical flare up. Have market participants, irrespective of asset class, grown complacent to geopolitical risks, or have they decided that the overall threat to the global economy of further incremental deterioration in U.S.-Iranian relations and more broadly, Middle Eastern stability, is relatively contained?

Taking market performance as a measure, there has been little visible dent to investors’ confidence from the most recent geopolitical flare up. Have market participants, irrespective of asset class, grown complacent to geopolitical risks, or have they decided that the overall threat to the global economy of further incremental deterioration in U.S.-Iranian relations and more broadly, Middle Eastern stability, is relatively contained?