In recent years, governments have become increasingly aware of the perils of greenhouse gases and have aimed to penalize the source of pollution while looking to incentivize low-carbon technologies. In addition, investors are now considering an organization’s future financial position to discount potential write-downs of assets and the effect on revenues, costs, cash flows, and capital expenditure associated with adhering to policy changes that factor in climate risks. The global market for environmental, social, and governance (ESG) exchange-traded funds (ETFs) alone is expected to expand from USD 25 billion to more than USD 400 billion within a decade.[1] In Japan, sustainable investments grew fourfold between 2016 and 2018.[2]

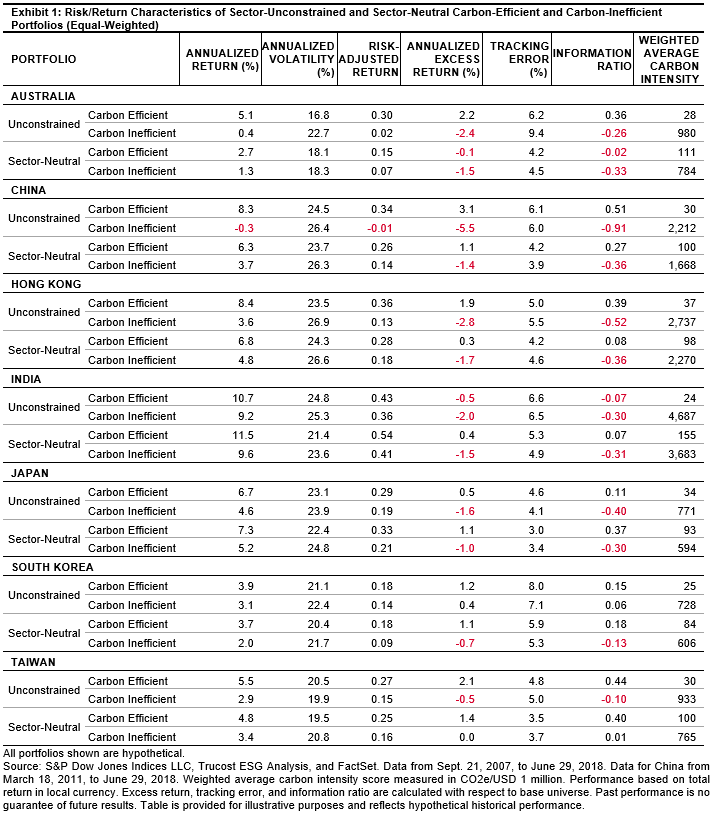

In our recently published research paper, Integrating Low Carbon and Factor Strategies in Asia, we studied the performance of carbon-efficient and carbon-inefficient portfolios with sector-neutral and unconstrained approaches in seven Asian markets—Australia, China, Hong Kong, India, Japan, South Korea, and Taiwan. In each market, we ranked all companies in the base universe by their carbon intensity scores. The tertile (one-third) of the base universe with the lowest and highest carbon intensity scores constituted the unconstrained carbon-efficient and carbon-inefficient portfolios, respectively. Similarly, in the sector-neutral approach, carbon-efficient and carbon-inefficient portfolios were composed of the tertile of stocks with the lowest and highest carbon intensity scores from each sector, respectively.[3] We analyzed the performance of equal-weighted (see Exhibit 1) and float-market-cap-weighted baskets (see Appendix E of the research paper).

In the paper, we concluded that carbon-efficient portfolios resulted in a significant reduction to weighted average carbon intensity scores without sacrificing returns across Asian markets over long time horizons. We also observed that the carbon-efficient portfolios outperformed their respective carbon-inefficient portfolios across the seven markets on absolute and risk-adjusted bases over the entire studied period (see Exhibit 1).

In the unconstrained approach, the carbon-efficient portfolios had much lower weighted average carbon intensity scores than their respective carbon-inefficient portfolios, with carbon intensity reductions between 95.6% and 99.5% across all markets. The highest return spreads and volatility reductions were seen in China, Australia, and Hong Kong.

With sector constraints in place, the weighted average carbon intensity score reductions between the carbon-efficient and carbon-inefficient portfolios ranged from 84.3% to 95.8% across markets. China, Japan, and Hong Kong recorded the highest excess return spreads and reductions in volatility.

Furthermore, compared with the base universe, the carbon-efficient portfolios tended to deliver positive information ratios, while the carbon-inefficient portfolios had negative information ratios in most markets in the unconstrained and sector-neutral approaches.

As expected, the differences in carbon intensity scores, the return spread, and volatility reduction between the carbon efficient and carbon-inefficient portfolios were much more pronounced in the unconstrained approach. The tracking error of unconstrained carbon-efficient portfolios was relatively higher (4.6%-8.0%). However, in the sector-neutral approach, the tracking error of the carbon-efficient portfolios tended to be much lower (3.0%-5.9%).

[1] Thuard, Johan, Harvey Koh, Anand Agarwal, and Riya Garg, “Financing the Future of Asia: Innovations in Sustainable Finance,” April 2019.

[2] Kodaira, Ryushiro and Matsumoto, Hiroko, “After fending off eco-warriors, Asia Inc find ‘ESG’ investors hard to ignore,” Nikkei Asian Review, June 12, 2019.

[3] For a detailed methodology of the research, please refer to Integrating Low Carbon & Factor Strategies in Asia.

The posts on this blog are opinions, not advice. Please read our Disclaimers.