The S&P U.S. High Yield Low Volatility Corporate Bond Index[1] is designed as a low volatility strategy in the high yield bond universe. The index aims to deliver higher risk-adjusted returns than the underlying broad-based benchmark through mitigating uncompensated credit risk. The back-tested index performance demonstrated the efficacy of the low volatility strategy, with reduced return volatility and drawdowns in stressed markets (please refer to our previous research paper).

In 2017 and the first three quarters of 2018, high yield credit spreads continued grinding lower, reflecting persistent yield chasing (see Exhibit 1). On Jan. 26, 2018, the option-adjusted spread (OAS) for the S&P U.S. High Yield Corporate Bond Index reached its tightest level since the 2008 financial crisis, at 266 bps. However, in Q4 2018, global risk assets sold off sharply amid concerns over global trade and slowing economic growth. The S&P U. S. High Yield Corporate Bond Index’s OAS widened by 174 bps as the S&P 500® declined by -14%.

How did the S&P U.S. High Yield Low Volatility Corporate Bond Index perform during the recent market turmoil? In this blog, we show that in the latest spread widening, the low volatility strategy outperformed the broad-based underlying universe, with the outperformance being driven by spread positioning.

Exhibit 2 displays the stress scenario analysis for the S&P U.S. High Yield Low Volatility Corporate Bond Index since 2000. During the Q4 2018 and early January 2019 sell-off, when the broad market high yield bond index OAS widened by 199 bps from trough to peak, the S&P U.S. High Yield Low Volatility Corporate Bond Index outperformed the broad-based S&P U.S. High Yield Corporate Bond Index by 1.2%, while the latter suffered a loss of 4.1%. Other periods of market stress are also included that point to the defensive nature of the S&P U.S. High Yield Low Volatility Index.

Exhibit 2 displays the stress scenario analysis for the S&P U.S. High Yield Low Volatility Corporate Bond Index since 2000. During the Q4 2018 and early January 2019 sell-off, when the broad market high yield bond index OAS widened by 199 bps from trough to peak, the S&P U.S. High Yield Low Volatility Corporate Bond Index outperformed the broad-based S&P U.S. High Yield Corporate Bond Index by 1.2%, while the latter suffered a loss of 4.1%. Other periods of market stress are also included that point to the defensive nature of the S&P U.S. High Yield Low Volatility Index.

Exhibit 3 details the monthly relative returns from October 2018 to August 2019. Cumulatively, the S&P U.S. High Yield Low Volatility Corporate Bond Index outperformed the broad-based universe by 1.75%, with positive performance during 7 out of the 11 months over the studied period. Most of the outperformance came from credit spread positioning, confirming that uncompensated credit risk mitigation could improve the performance of a low volatility strategy.

[1] For information about the methodology, please refer to https://spdji.com/documents/methodologies/methodology-sp-us-high-yield-corporate-bond-strategy-indices.pdf.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

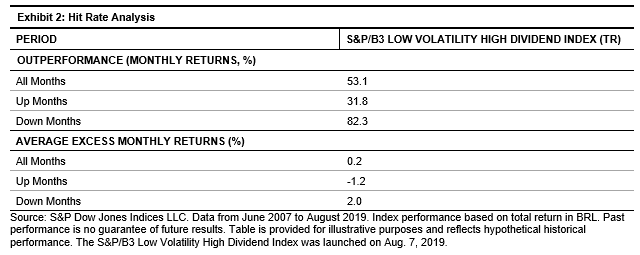

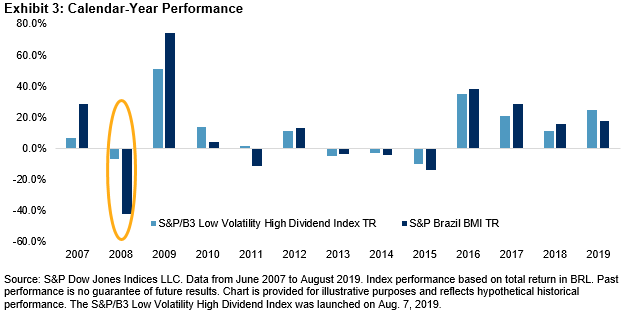

The S&P/B3 Low Volatility High Dividend Index provided downside protection in periods of market turbulence. During all the months in which the benchmark was down between June 2007 and August 2019, the S&P/B3 Low Volatility High Dividend Index outperformed 82.3% of the time and generated a monthly average excess return of 2% over the benchmark.

The S&P/B3 Low Volatility High Dividend Index provided downside protection in periods of market turbulence. During all the months in which the benchmark was down between June 2007 and August 2019, the S&P/B3 Low Volatility High Dividend Index outperformed 82.3% of the time and generated a monthly average excess return of 2% over the benchmark.

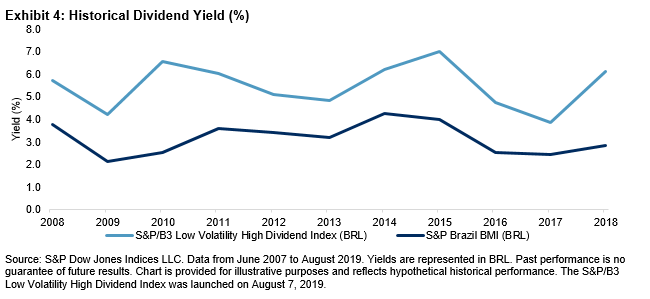

The S&P/B3 Low Volatility High Dividend Index was also able to generate higher yield than the S&P Brazil BMI. Over the studied period, the S&P/B3 Low Volatility High Dividend Index had an average historical yield of 5.5%, compared with 3.1% for the benchmark.

The S&P/B3 Low Volatility High Dividend Index was also able to generate higher yield than the S&P Brazil BMI. Over the studied period, the S&P/B3 Low Volatility High Dividend Index had an average historical yield of 5.5%, compared with 3.1% for the benchmark.