Let’s suppose for a moment that you are given a choice between two hypothetical exchange traded funds (ETFs) tracking the same index. Fund A has an annual management fee of 0.4% while Fund B has an annual management fee of 0.1%. At first glance, Fund B seems like the better option: it offers similar performance at a lower cost.

But you still have to purchase the fund and – at some later point in time – you may wish to sell it. Trading costs can be complicated, but, at least for a small position, we can assume that they are accurately represented by the bid-ask spread for each ETF.

Suppose both Fund A and Fund B have a fair value of $100 per share, but Fund A can be bought for $100.05 a share and sold for $99.95 a share while Fund B can be bought for $100.25 a share and sold for $99.75 a share. Fund A has a $0.10 bid-ask spread, while Fund B has a $0.50 bid-ask spread.

Over the next year, suppose that both funds precisely track an index gain of 10%. Assuming the same spreads, which fund would have given you the best total return after costs if you sold at year-end?

Though Fund A’s management fee was higher, the cost to get in and out of Fund B more than covered the difference. Said another way: Fund A’s liquidity compensated for its higher fee.

Naturally, the relative importance of trading costs and management fees varies with the time for which positions are held. The more one trades, the more important the trading costs will be in determining long-term returns.

A wide range of factors will go into determining the trading costs in an ETF, including whether or not there are other ways to trade exposures linked to the same index – such as other ETFs, or perhaps futures and options linked to the same index.

The chart below compares the average bid-ask spreads in equity-linked ETFs listed in the U.S. over the past year based on data from Bloomberg. We also computed the averages for ETFs linked to S&P DJI Indices, and to the average for ETFs tracking a select few of S&P DJI’s indices that associated to a wide ecosystem of trading vehicles – in particular the S&P 500®, S&P Select Sector indices, and The Dow®.

As the chart shows, products linked to S&P DJI’s indices tend to have lower spreads than average, and products linked to our best-known indices (specifically the S&P 500, DJIA and Select Sector family) are some of the most liquid.

As our most recently published paper illustrates, several of S&P DJI’s indices have developed a deep ‘ecosystem’ of trading and liquidity. Accordingly, users of index-based products may wish to consider the trading volumes associated with the underlying index as an important factor in choosing an appropriate investment allocation.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

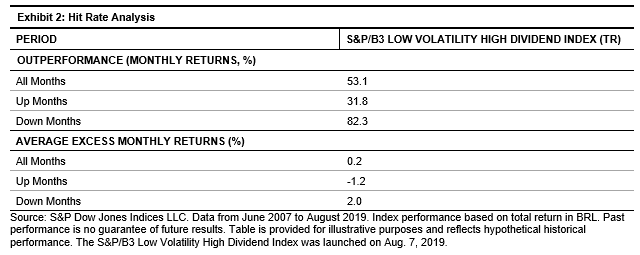

The S&P/B3 Low Volatility High Dividend Index provided downside protection in periods of market turbulence. During all the months in which the benchmark was down between June 2007 and August 2019, the S&P/B3 Low Volatility High Dividend Index outperformed 82.3% of the time and generated a monthly average excess return of 2% over the benchmark.

The S&P/B3 Low Volatility High Dividend Index provided downside protection in periods of market turbulence. During all the months in which the benchmark was down between June 2007 and August 2019, the S&P/B3 Low Volatility High Dividend Index outperformed 82.3% of the time and generated a monthly average excess return of 2% over the benchmark.

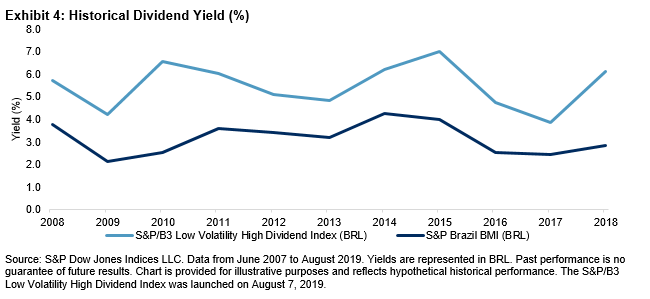

The S&P/B3 Low Volatility High Dividend Index was also able to generate higher yield than the S&P Brazil BMI. Over the studied period, the S&P/B3 Low Volatility High Dividend Index had an average historical yield of 5.5%, compared with 3.1% for the benchmark.

The S&P/B3 Low Volatility High Dividend Index was also able to generate higher yield than the S&P Brazil BMI. Over the studied period, the S&P/B3 Low Volatility High Dividend Index had an average historical yield of 5.5%, compared with 3.1% for the benchmark.

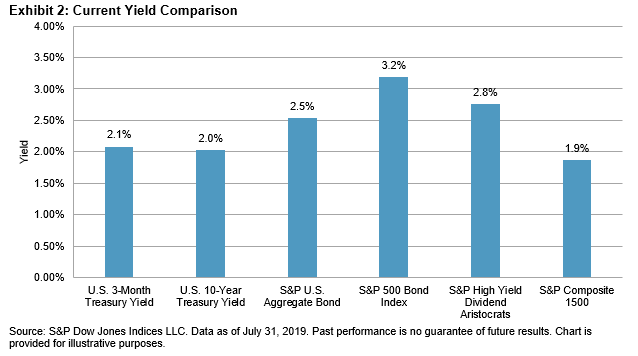

For comparison purposes, Exhibit 2 lists recent yields of selected securities and indices. As of July 31, 2019, the S&P High Yield Dividend Aristocrats had a dividend yield of 2.8%, which was higher than the yields of the other securities and indices shown, with the exception of the

For comparison purposes, Exhibit 2 lists recent yields of selected securities and indices. As of July 31, 2019, the S&P High Yield Dividend Aristocrats had a dividend yield of 2.8%, which was higher than the yields of the other securities and indices shown, with the exception of the