Commodities markets resumed their upward trajectory in June. The S&P GSCI was up 4.4% for the month and up 13.3% YTD. The Dow Jones Commodity Index (DJCI) was up 3.1% in June and up 6.9% YTD, reflecting its lower energy weighting. A recovery in petroleum prices and an impressive rally in gold were the main drivers of the broad commodities indices’ performance over the month.

In the oil markets, bearishness regarding the state of the global economy was tempered by fears regarding a possible disruption of oil exports from the Gulf region and prospects for a renewed production deal from OPEC. Tanker attacks in the Strait of Hormuz and the Gulf of Oman over the course of June undermined global shipping security and escalated the dispute between the U.S. and Iran over its nuclear program. The S&P GSCI Petroleum ended the month up 7.2%. At the start of July, a deal was reached between members of the OPEC Plus group to extend the existing oil output cuts of 1.2 million barrels per day for nine months.

The S&P GSCI Industrial Metals reversed its course from the prior two months, rising 2.0% in June. Over the first six months of the year, the S&P GSCI Nickel rose an impressive 19.1%; the rally was largely attributed to the long-term prospects for the use of nickel in electric vehicles and falling exchange-held inventories, and was in spite of the fact that the well-documented supply gap in the refined nickel market is expected to shrink over the second half of the year. The S&P GSCI Iron Ore moved significantly higher, by 14.9% in June, due to another drop in port inventories and additional Chinese government stimulus. An agreement between Trump and Xi Jinping to restart trade talks following a meeting at the G20 Summit also contributed to the strong performance.

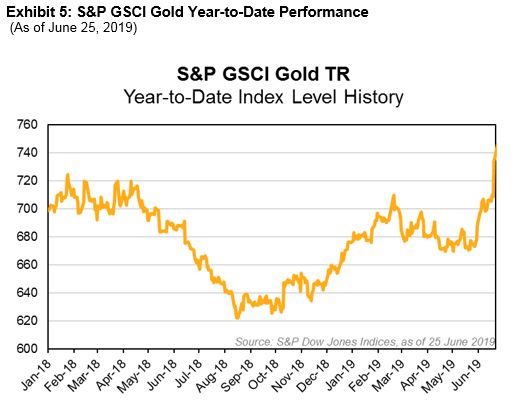

The other metal to record double digit percentage gains was the S&P GSCI Palladium, which jumped 15.7% in June due largely to investor demand and is now close to reaching an all-time high. The S&P GSCI Gold increased 8.0% for the month. The exhilaration that was associated with the strength of the global economy a year ago has been replaced with growing financial market turbulence, a plethora of geopolitical flashpoints, and a string of economic releases that have fallen short of expectations. It would appear that few central banks wish to find themselves on the wrong side of the U.S. Fed, suggesting that lower interest rates are on the horizon. Gold tends to perform well in these circumstances.

The S&P GSCI Agriculture ended the month up only 0.3%, with some of the recent weather-induced exuberance taken out of the grains market on the last day of the month, following the release of the USDA’s Acreage Report. The S&P GSCI Coffee was up 2.2% in June, with prices buoyed by the threat of a cold snap in Brazil, which could pose a threat to crops.

The rollercoaster ride continued in the lean hogs market, with the S&P GSCI Lean Hogs down 10.0% in June. The latest U.S. hogs and pigs report indicates that pig and pork supplies in 2019 will be well above last year’s levels. The June 2019 hog inventory was up 4% year-over-year and the breeding herd expanded by 1%. This is the highest June 1 inventory of all hogs and pigs in the U.S. since estimates began over 50 years ago. At the same time, U.S. pork exports to China have been lackluster due to the ongoing trade spat between the two nations, and despite the devastation caused to the Chinese domestic industry by African swine flu.

The posts on this blog are opinions, not advice. Please read our Disclaimers.