While substantial literature exists on dividend investing in developed markets, there is little research on emerging market dividend strategies, in particular for Latin America. S&P Dow Jones Indices surveyed the emerging market dividend payers in 2014 and found that Latin America constituted about 19% of the total global dividend payers.[1] As such, Latin American markets are capable of supporting dividend-based strategies.

In countries like Brazil, Mexico, Chile, and Peru, benchmark providers already offer passive dividend indices as a way to measure performance and provide exposure to dividend-paying stocks. We now expand the investment concept to the Colombian market.

As a starting point, we analyzed the historical dividend payers using the S&P Colombia BMI as the underlying universe, based on 10 years of dividend payment history. We found that on average, 92% of the constituents paid dividends at least once during the trailing calendar year, translating to roughly 97% of the index market cap (see Exhibit 1).

When we looked at the total amount of dividends paid by GICS® sectors (see Exhibit 2), Financials was the largest sector by absolute amount of dividends paid. This was not surprising, as the sector represented 48% of the universe’s floating market cap, on average.

The average dividend yield in Colombia over the trailing 10-year horizon was 2.84%,[2] and the top three dividend yield contributing sectors were Financials (1.4%), Energy (0.7%), and Utilities (0.2%, see Exhibit 3). While Financials had the biggest outsize contribution to yield in the past four years, its contribution actually varied when we went back further in history. Furthermore, we found that Energy used to contribute much more in previous years (2009-2014) compared with recent periods (2016-2018).

When we looked at the historical average number of dividend paying companies by sector, we saw that sectors such as Energy and Communication Services had only one security (see Exhibit 4). The Energy sector in particular raised concentration issues, as its sole constituent had high average dividend yield (5.8%).

With 16 companies paying dividends in 2018, dividend-based strategies in Colombia are possible. However, any construction of such strategies would need to consider potential single-stock and sector concentration issues.

[1] https://spindices.com/documents/research/research-a-field-guide-to-emerging-market-dividends.pdf

[2] The average dividend yield is calculated as a weighted average of the index weight and one-year trailing dividend yield.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

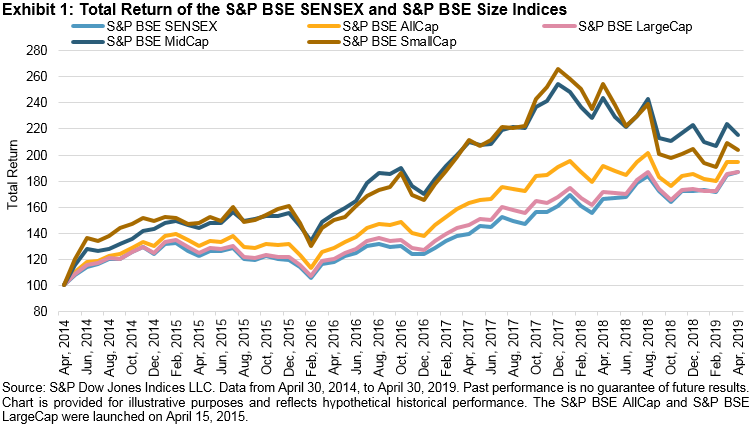

Exhibit 2 provides the five-year absolute returns of the S&P BSE AllCap Series. Among the sub-sector indices in the S&P BSE AllCap, the

Exhibit 2 provides the five-year absolute returns of the S&P BSE AllCap Series. Among the sub-sector indices in the S&P BSE AllCap, the