The S&P Style Indices and S&P Pure Style Indices take distinct approaches in differentiating between value and growth factors. In past blogs,[1] we examined how differences in index construction can affect the performance of the indices in both series over a long-term investment horizon. In this blog, we examine how the suite of pure style and style Indices behave in various market and style cycles.

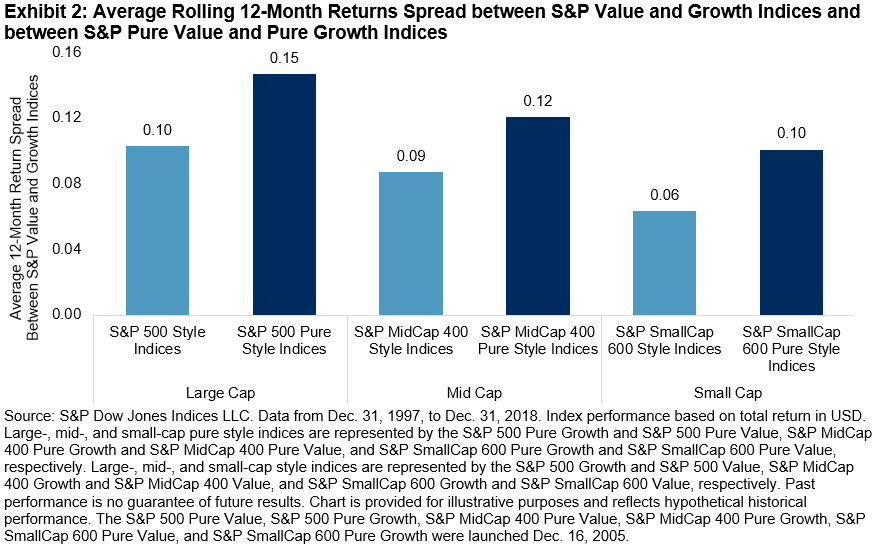

When looking at the correlation of value and growth pairs for both sets of indices (see Exhibit 1), we see that the pure style indices exhibited lower correlations between value and growth than their traditional style counterparts. In other words, there was a higher correlation spread between pure style indices than the traditional style indices. The relative performance of value and growth indices moves in cycles over time, thus market participants could potentially make tactical adjustments to take advantage of short-term deviations in relative value. Exhibit 2 illustrates the style return spread (value minus growth) for the large-cap, mid-cap, and small-cap style and pure style indices.

The relative performance of value and growth indices moves in cycles over time, thus market participants could potentially make tactical adjustments to take advantage of short-term deviations in relative value. Exhibit 2 illustrates the style return spread (value minus growth) for the large-cap, mid-cap, and small-cap style and pure style indices.

During periods when one style was favored over the other, the return spreads of the pure style indices were markedly wider than the style indices across all cap sizes. Also, the pure style indices typically had higher performance in the direction of the favored style (see Exhibit 3). Therefore, the greater discriminatory power of the pure style indices may allow for more effective style rotation strategies and hedging tools.

Over the study period, when value was in favor, pure value outperformed value the majority of the time across all size segments. However, when growth style was in favor, we find that results were mixed. In large caps, growth outperformed pure growth slightly more often (52% to 48%), while the average excess return of pure growth versus growth was positive (0.16). In mid caps, pure growth did better than growth more often, while growth did slightly better than pure growth in small caps.

The asymmetric performance of the pure style indices indicates that they may have more sensitivity to market movements than the style indices. We next compute the betas of pure style and style to their respective benchmarks (see Exhibit 4).

On average, the traditional style indices each had betas close to one, meaning the style indices generally moved in the same direction and magnitude as the respective benchmark. This points to the standard style indices potentially being a suitable choice for strategic long-term equity market exposure, with a slight tilt to the desired style.

The pure style indices all had average betas higher than one. Therefore, in an up market, pure style indices could be expected to do better than the style indices. Conversely, in down markets, pure style indices may underperform their style counterparts.

Market participants may look to use growth and value together in a portfolio, tilting to one side based on their views. In an upcoming post, we will analyze the effect of combining value and growth at varying weights in hypothetical portfolios.

[1] https://www.indexologyblog.com/2019/01/15/pure-style-indices-a-finer-tool-with-higher-style-focus/

https://www.indexologyblog.com/2019/01/30/reviewing-sp-pure-style-indices-from-a-sector-perspective/

The posts on this blog are opinions, not advice. Please read our Disclaimers.