The impact of fees on investment returns is a widely studied and much debated topic. Over the past decade, as index-linked, lower-cost passive investing has taken hold, fees have become a greater focus. In recent years, there have been several studies published examining the impact of fees on performance.

The U.K’s Financial Conduct Authority (FCA), which has long been concerned that investors are charged high fees for active funds that closely track index performance, has published a number of reports calling for fee transparency. Last month, the European Securities and Markets Authority (ESMA) published a study[1] that showed that actively managed equity funds have higher fees than passively managed equity funds, leading to lower performance on a net-of-fees basis for active funds.

Following the ESMA study, a recent article in the Financial Times[2] argued along similar lines that more mutual funds underperformed their benchmarks than institutional accounts in the same category in the long term, primarily due to higher fees.

The question then arises, to what degree do fees vary between institutional and retail accounts for a given investment style?

To quantify the fee discrepancy between retail and institutional accounts, we compiled the fees analysis using data from institutional managed accounts and mutual funds as of Dec. 31, 2017. For institutional managed accounts, we looked at managers that reported both gross-of-fees returns and net-of-fees returns and calculated the difference as the fee. For mutual funds, we used the expense ratio to represent the fees.

We then calculated the median fee charged in each category (see Exhibit 1).[3] In general, institutional managed accounts charged roughly 60%-75% of the fees charged by mutual funds. Among the four equity investment styles we analyzed, the median fee of institutional large-cap strategies was roughly two-thirds of similar large-cap mutual funds. Similarly, the median institutional emerging market and global equity strategies had fees 33 bps lower than their retail counterparts.

The gap between institutional accounts and mutual funds widened in fixed income. High-yield institutional accounts, for example, charged 39 bps less on average than their mutual fund peers, and the median fee was only 59% of the median fee being charged by retail high-yield funds.

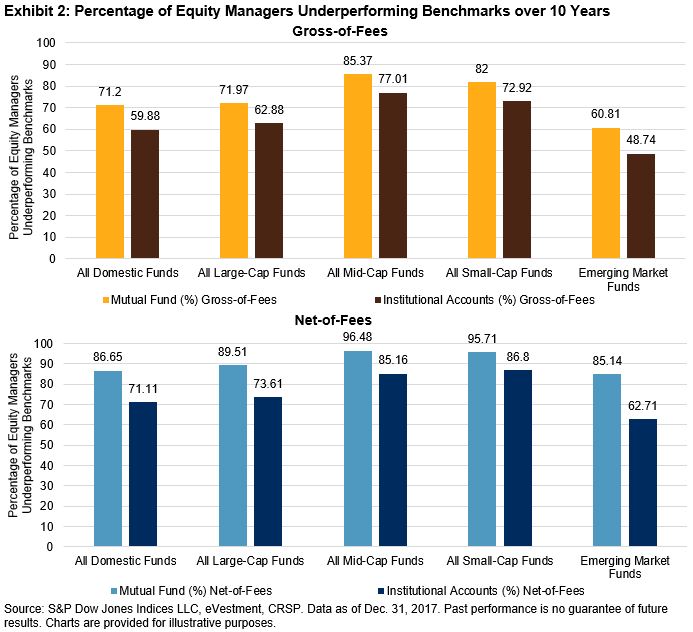

The impact of fees is prominent when we compare the strategy’s relative performance against its respective benchmark. For example, over the last 10 years, the S&P Composite 1500® outperformed 11 percentage points (71% versus 60%) more domestic mutual funds than domestic institutional accounts on a gross-of-fees basis, and the gap widens to 16 percentage points (87% versus 71%) on a net-of-fees basis (see Exhibit 2).

Fee impact is further magnified in less liquid or less efficient markets. In emerging markets, on a gross-of-fees basis, 12 percentage points (61% versus 49%) more mutual funds underperformed their benchmarks compared with institutional counterparts; on a net-of-fee basis, the gap almost doubled to 22 percentage points (85% versus 63%).

Our analysis is consistent with ESMA’s conclusion that costs are higher for retail compared with institutional investors across asset classes and domiciles. Actively managed retail funds may provide a slightly better gross performance than passively managed funds, but the margin is small and may diminish after fees are accounted for.

[1] https://www.esma.europa.eu/sites/default/files/library/esma50-165-731-asr-performance_and_costs_of_retail_investments_products_in_the_eu.pdf

[2] https://www.ft.com/content/b92a78a3-1409-376c-81b4-86b58a2b2e9d

[3] We used the same categories as those provided in the Financial Times article.

The posts on this blog are opinions, not advice. Please read our Disclaimers.