Despite looming threats to global trade, emerging market stocks are a staple of diversified equity portfolios. Emerging countries are a diverse group, accounting for about 28.8% of real world GDP (measured in 2005 U.S. dollars) as of Nov. 12, 2018, according to FactSet. The comparable figure for U.S. production is 25.4%. Year-over-year growth in real GDP was 5.1% for emerging countries and 3.0% for the U.S. Extrapolating these figures 20 years into the future would increase the share of global GDP from emerging countries to about 42%, while the U.S. would remain at approximately 25%.

In spite of their economic footprint, emerging countries’ stocks account for about 10% of global market capitalization, while U.S. stocks account for about 54%. That said, U.S. market value is fully represented in benchmarks, while that of emerging countries is not. Inclusion of emerging market equities is constrained by foreign ownership limits and a lack of complete access. China is the most significant case, but index providers are generally moving toward inclusion of locally listed Chinese shares over time as foreign access opens up. As a result, available emerging market capitalization is set to increase, enhancing diversification and expanding the global investment opportunity set. U.S. investors who ignore this trend will implicitly accept greater drift from the global investment opportunity set over time.

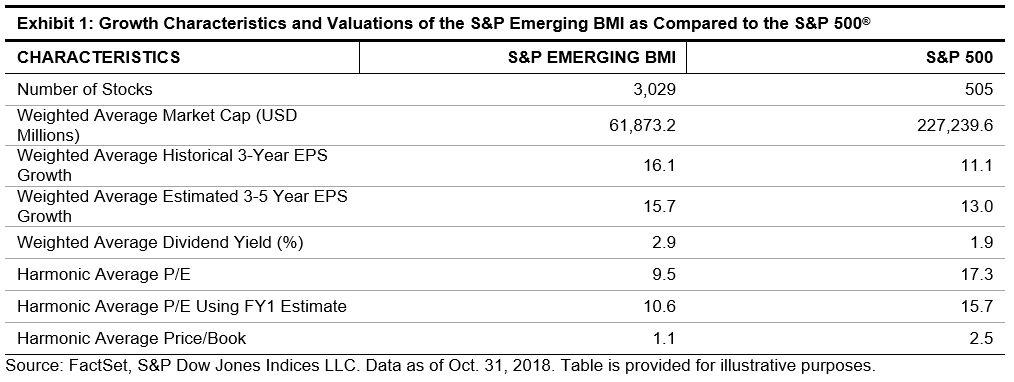

In addition to being a growing proportion of the investment opportunity set, emerging equities may offer compelling growth and value. As shown in Exhibit 1, relative to U.S. stocks, emerging market stocks offer higher earnings growth and dividend yield, coupled with lower valuation ratios.

For USD investors, value may also be present in emerging market currencies. In the long run, the growing economic significance of emerging market countries is consistent with potential currency appreciation. Yet currency market participants react to short-term risks just as they do in other markets. Recent currency weakness detracted from the returns of the S&P Emerging BMI (USD) versus the same index hedged to USD (see Exhibit 2).

To be sure, uncertainties abound in emerging market equities, including political risk, market risk, and currency risk. However, bearing such hazards may be the cost of earning a long-term return premium. Taking account of the expanding global investment opportunity set and relative attractiveness of emerging markets, in terms of growth potential and valuation, suggests that U.S. market participants who seek exposure to the equity risk premium could be disadvantaged if they under-allocate to emerging market stocks.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

Low volatility’s success was not unique to the U.S. Exhibits 3 and 4 show that similar trends occurred globally, particularly in the emerging markets and Asia, regions that have experienced turmoil for most of this year. The

Low volatility’s success was not unique to the U.S. Exhibits 3 and 4 show that similar trends occurred globally, particularly in the emerging markets and Asia, regions that have experienced turmoil for most of this year. The