In a prior post, we reviewed the risk and returns of portfolios with different equity and fixed income combinations. We saw that while equities outperformed fixed income during the period studied, fixed income had a higher risk-adjusted return ratio (annualized return divided by annualized risk). Due to the low return correlation between the two asset classes, compared with when viewed in isolation, the blended portfolios resulted in two notable observations: 1) higher risk-adjusted returns for the 10/90 and 20/80 equity/bond combinations, and 2) higher absolute returns for the portfolios ranging from 30/70 to 90/10 equity/bond mixes.

In this post, to better comprehend the drivers of return and risk for the allocations, we calculated the marginal contribution to total portfolio risk for each asset class. Computationally, the marginal contribution of asset to total portfolio risk can be defined as:[1]

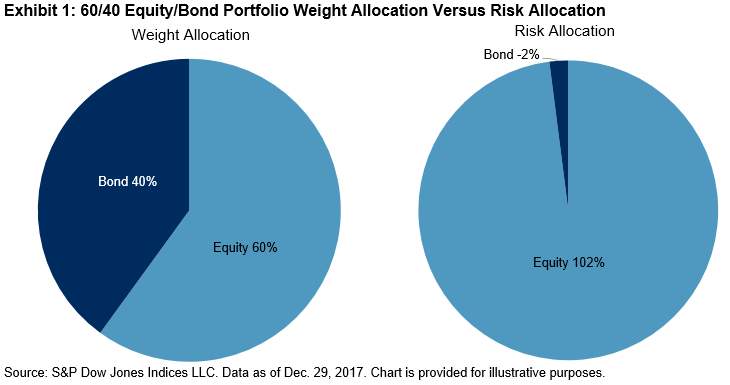

We calculated the contribution to portfolio risk from 2000 to 2017 for each asset class and Exhibit 1 shows the average annual risk contributions for the 60/40 equity/bond portfolio.

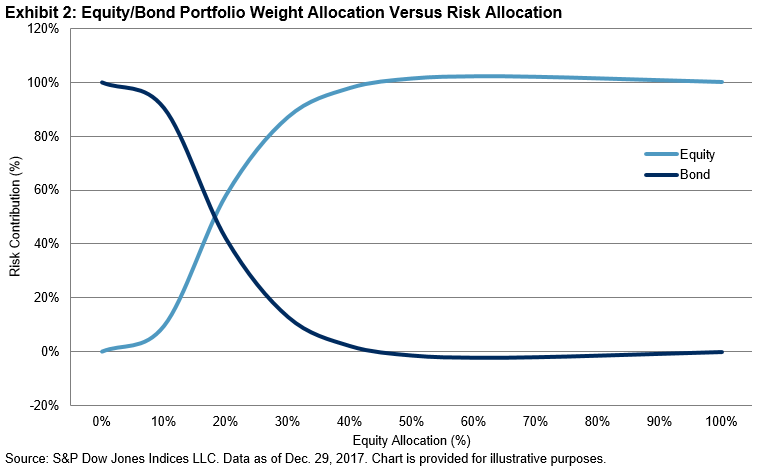

For the classic 60/40 equity/bond portfolio, we see that the risk contribution for each asset class did not align with the weight allocations. While 60% weight was allocated to equities, the average contribution to risk was 102%, thus an average of -2% for bonds. The results show the importance of considering asset class volatility and their covariance. To understand how risk contributions change as weight allocations move from 0%-100% in equity (and 100%-0% in fixed income), Exhibit 2 shows the annual averages.

There is a clear non-linear relationship between the change in weight and the change in risk contribution. With equities being more volatile than bonds and the return correlation between the two being low, as the allocation to equities increases, its risk contribution to total portfolio volatility increases at a quicker pace. In the end, the point where the two asset classes most likely contribute equally would be at the 20/80 equity/bond mix.

Exhibits 1 and 2 in this post allow us to conclude that the risk contribution of asset classes can be meaningfully different from their weight allocations in a portfolio. In following posts, we will build upon the findings in this post and construct a basic three-asset risk parity strategy and compare it with an equal-weight portfolio.

[1] = weight of asset i, σp = portfolio volatility, βi = beta of asset i to the portfolio, Cov(σi,σp) = covariance of asset i to portfolio, and σp2 = portfolio variance.

The posts on this blog are opinions, not advice. Please read our Disclaimers.