General elections (president, senate, and chamber of deputies) are around the corner. The eyes of every Mexican and many people around the globe are on the Mexico-Brazil match of the World Cup—wait, that is another story.

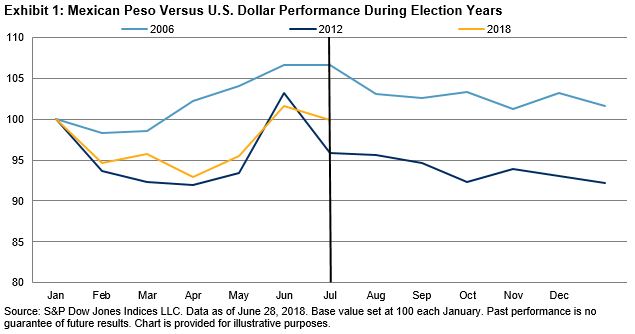

Nobody knows what the outcome of the elections will be. We have seen different events where the polls were wrong (for instance, Mexico beating Germany in the match on June 17, 2018). However, the market incorporates these expectations in many ways, one being the currency. Exhibit 1 shows how the Mexican peso performed before and after the past two elections (2006 and 2012) compared with the U.S. dollar.

We can see that before the elections, the tendency in 2012 and 2018 was similar, and after the elections in 2006 and 2012, the tendency was an appreciation of the currency. We know that the elections are not the only factor moving the Mexican peso—for example, in 2018 due to the NAFTA, it has shown a lot of volatility.

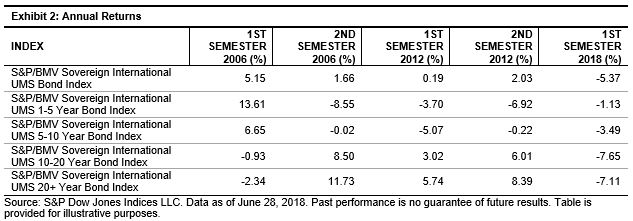

Exhibit 2 shows how the S&P/BMV Sovereign International UMS Bond Indices, which are designed to measure the performance of Mexican government securities issued outside of Mexico in U.S. dollars, performed before and after the elections.

In 2018, the elections have not been the only factor affecting the Mexican peso. The Mexican Central Bank has followed the U.S. Fed’s policy decisions and moved up the overnight interbank interest rate 50 bps to stand at 7.75%. In 2012, the rate was steady at 4.50%.

Any outcome on Sunday, June 30, 2018, will surely have an impact on Mexico. By nightfall, we may have a newly elected president, but at 9:00 am (local time) on Monday, July 2, 2018, Mexico will play against Brazil in the World Cup. Looks like attention to the news to see how the elections went will have to be shared with the match!

The posts on this blog are opinions, not advice. Please read our Disclaimers.