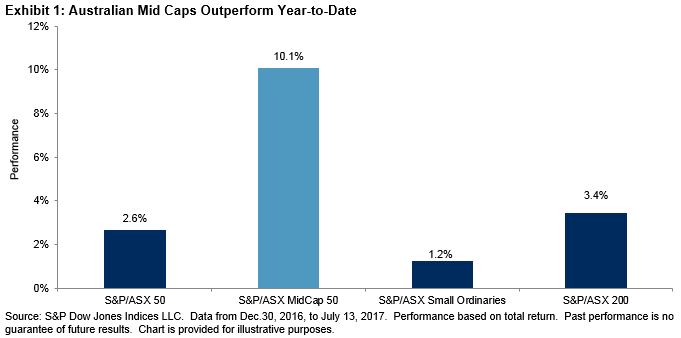

We have previously taken a dive into performance differences between Australian market cap segments and observed that mid caps offer a “sweet spot” for market participants. Year-to-date, this message continues to resonate—the S&P/ASX MidCap 50 has returned 10.1% as of July 13, 2017. Meanwhile, corresponding large-, small-, and broad market indices have returned measurably less (see Exhibit 1).

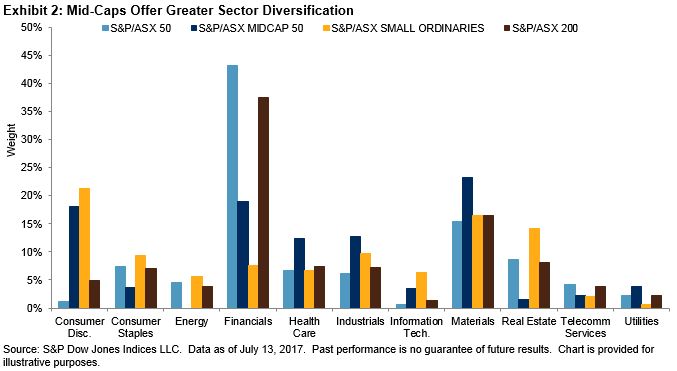

Examining some differences between the indices, the S&P/ASX MidCap 50 has a more diverse sector representation than the large-cap and broad market Australian benchmarks, which are dominated by banks. As shown in Exhibit 2, the financials sector makes up 43% of the S&P/ASX 50, while only representing 19% of the S&P/ASX MidCap 50. The mid-cap and small-cap indices also have higher proportions of exposure to consumer discretionary stocks, while The S&P/ASX Mid-Cap 50 has higher allocations to health care, industrials, and materials than the other market cap indices.

Due to large allocations to financials among large-cap and broad market indices, these segments have been more negatively affected by new bank levies. These levies aim to tax the liabilities of the country’s five largest banks, which account for 36% of the value of the S&P/ASX 50 and are subsequently excluded from mid-cap and small-cap indices. Amid these forces, Australia’s financial sector, as measured by the S&P/ASX 200 Financials, has underperformed the broad market, limited to a gain of 1.8% for the year.

Meanwhile, despite having relatively diversified sector exposures and a lower allocation to the financials sector, small-cap stocks still lag the other market cap segments year-to-date.

The mid-cap segment of the Australian stock market is often overlooked and underappreciated. Pure mid-cap investing is not common, and often, mid- and small-cap companies are lumped together for investment purposes, diluting the unique characteristics of mid-sized companies. Those looking for an edge in Australian equities might note that mid caps tend to offer a unique balance between the high growth (and therefore higher risk) of small caps and the stability (but slower growth) of large caps, which has led to meaningful outperformance year-to-date.

The posts on this blog are opinions, not advice. Please read our Disclaimers.