Liquidity may be defined as the ability to buy or sell a bond within a reasonable period of time and at a reasonable price. A simple way to compare two bonds is through the use of Trade Reporting and Compliance Engine (TRACE) daily volume data. The data represents the daily aggregation of each reported trade throughout the day. The existence of reported volume data can be indicative of the frequency of trading. For example, if a bond has volume data for 20 of the last 22 trading days, then it trades relatively frequently—nearly every day. The volume data itself can also indicate the size in which it trades daily. For two bonds, we can compare the turnover rate, defined as the total volume traded in 22 days as a percentage of the amount outstanding. For example, a bond may be considered more liquid relative to another one if a larger portion of its total outstanding is traded over a one-month period.

In addition to considering volume and frequency, the daily price change or bid-offer spreads can be key indicators, particularly over periods of acute stress. If a large holding of an asset is sold quickly but at a significant loss, it may not be liquid. More granular data, such as intraday trade details (size and bid-offer spread), could help improve the analysis of relative bond liquidity.

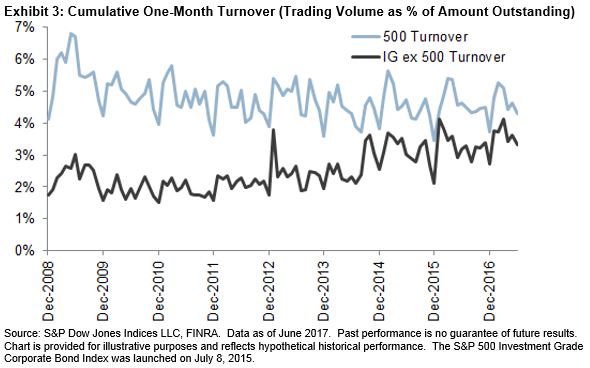

In this post, we focus on the simpler approach of comparing frequency and turnover to assess relative liquidity. We compare the S&P® 500 Investment Grade Corporate Bond Index to U.S. investment-grade (IG) corporate bonds excluding the S&P 500 issues.

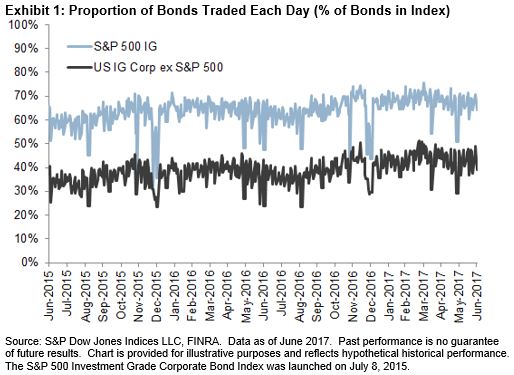

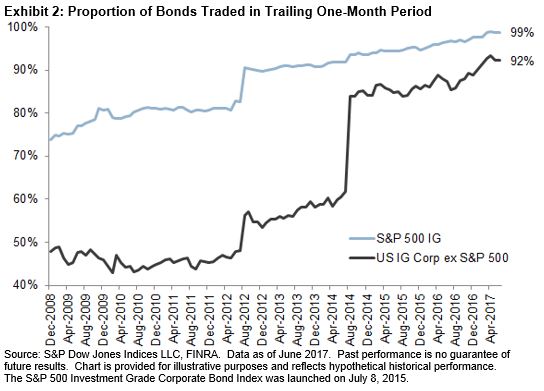

The constituents in the S&P 500 Investment Grade Corporate Bond Index trade more frequently than the U.S. IG corporate bonds ex-S&P 500. Over the past two years, on average, 64% of the bonds in the S&P 500 Investment Grade Corporate Bond Index traded every day versus 39% in the U.S. IG corporate bonds ex-S&P 500 (see Exhibit 1). Over the same period, 96% of the bonds in the index traded at least once each month versus the U.S. IG corporate bonds excluding the S&P 500 at 88% (see Exhibit 2).

The constituents of the S&P 500 Investment Grade Corporate Bond Index turn over about 30% faster than other U.S. IG corporate bonds. Despite an improvement in trading volume for the non-S&P 500 bonds since 2008, turnover still lagged the S&P 500 bonds. Exhibit 3 shows the trend in volume as a percentage of amount outstanding (turnover rate). Most recently, it would take about 22 months (4.5% per month) to turn over the entire USD 3.8 trillion S&P 500 Investment Grade Corporate Bond Index universe, while it would take eight months longer (2.7% per month) to turn over the USD 0.89 trillion that makes up the U.S. IG corporate bonds excluding the S&P 500.