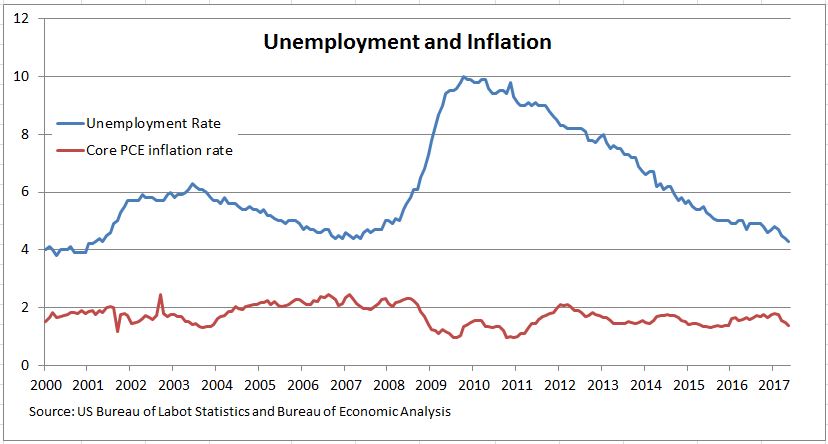

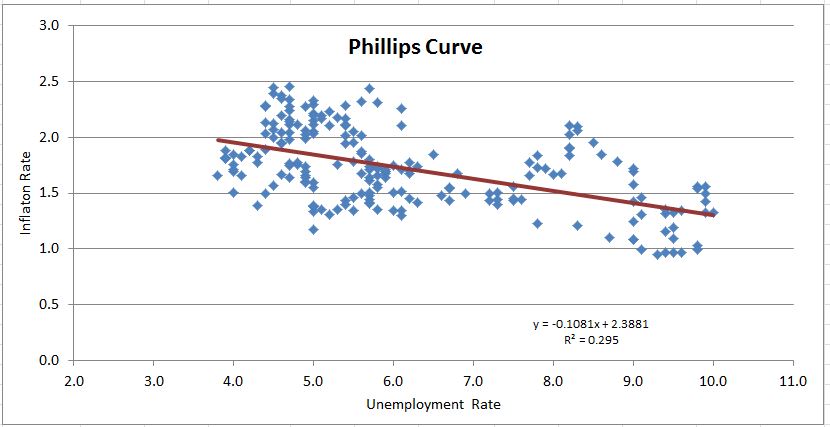

With the French election ending in the defeat of Le Pen, one more risk factor has been removed from the table and low volatility has returned. In Q2, the CBOE Volatility Index (VIX®) fell below 10 seven times, and the closing level of 9.75 on June 2, 2017, was the lowest since 1993. Do these low VIX levels predict a rising stock market? Is it time to long VIX derivatives?

VIX measures the expected volatility of the S&P 500® over the next 30 days using S&P 500 (SPX) options. Since stocks tend to fall much faster than they rise, a high VIX level, or a high implied volatility of SPX options, tends to indicate falling stock prices. However, the opposite does not always hold true in a low volatility environment, as stocks may either rise or fall. Low VIX levels only indicate that the market is quiet and that people are not willing to pay a lot for short-dated protection.

Although VIX is just one year older than Justin Bieber and we don’t have enough data points to draw any conclusion that is statistically significant, we can still take a look at the 16 days during which VIX went below 10. Our observations are:

- Falling VIX does not necessarily lead to rising equity markets;

- VIX spot tends to rise due to its mean reverting property; and

- With the VIX futures curve in contango, market participants can incur losses if they have a long position in VIX futures when VIX levels are extremely low.

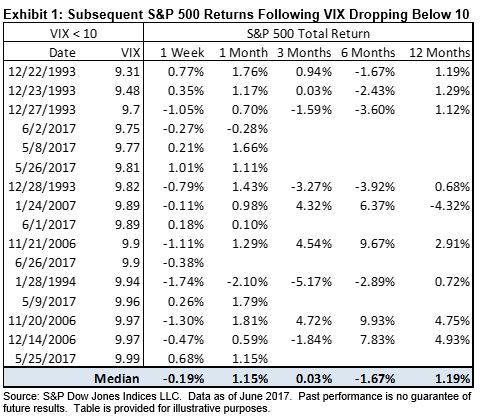

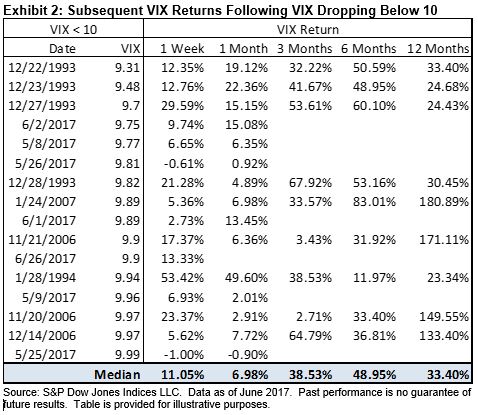

Exhibit 1 shows the 16 days in history during which VIX hit below 10, along with the subsequent returns of the S&P 500 over near-, mid-, and long-term periods following the drops. The immediate performance of the equity market is mixed; the S&P 500 had about a 50/50 chance of going up and down—in other words, it’s a random coin toss. The 1-, 3-, 6-, and 12-month returns are also not convincing for a strong bull market. In fact, we noticed that the 9.89 reading on Jan. 24, 2007, was followed by the 2008 financial crisis only ~18 months later. Overall, one can argue that low VIX levels have told us virtually nothing about stock market returns in the past.

Low VIX levels are usually followed by a positive VIX return, because VIX usually fluctuates around its local mean (see Exhibit 2). As long as sub-10 does not become the new normal, VIX will most likely pull itself back into the double-digit region.

However, a low VIX level is not a sign of taking a long position in VIX derivatives.

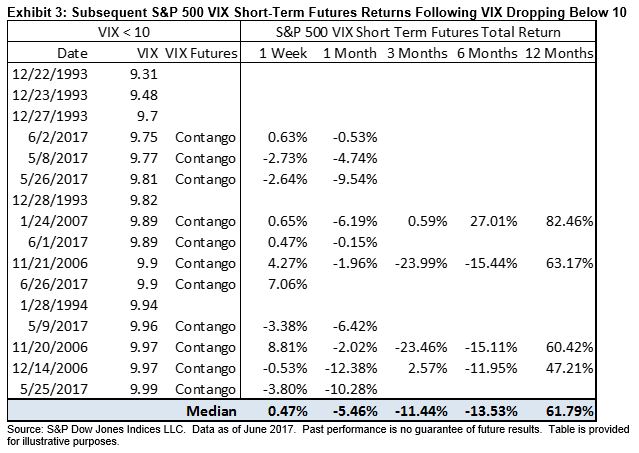

Given that VIX is not tradable, market participants might consider using derivatives such as VIX futures to access volatility. In the past, when VIX had hit below 10, VIX futures were always in contango, with the futures contracts more expensive than the spot. That means market participants with a long position in VIX futures incurred losses. Imagine a market participant holding a long futures position when VIX goes under 10. Upon the expiration of the current futures, he/she may choose either to let the futures expire or roll to the next contract. In the former case, the futures price drops as it converges to the spot; in the latter case, he/she has to pay the price difference in roll to the next futures contract.

Exhibit 3 shows the same 16 days during which VIX hit below 10, along with the subsequent returns of the S&P 500 VIX Short-Term Futures Index, which simulates a hypothetical rolling position from first-month VIX futures to second-month futures to maintain a long VIX futures of one-month constant maturity. Because VIX futures were not available in 1993 and 1994, we do not report the hypothetical returns. For all of the other 11 occurrences, the futures curves were all in contango. Although one-week performance was mixed, in the subsequent month following VIX dropping below 10, the S&P 500 VIX Short-Term Futures Index posted negative returns.

Volatility in the U.S. equities market has dissipated, as market participants brushed aside unknowns from healthcare bills, tax reform, and financial regulation. Low VIX numbers witnessed in Q2 indicate that financial markets may be settling into a low volatility region. However, history has shown that low VIX levels are not necessarily followed by a rising market in the near future. More importantly, although VIX spot tends to rise due to its mean reverting property, volatility investors should consider the deep contango associated with low VIX spot, which, contrary to the “buy the dip” principle, may suggest selling VIX derivatives rather than buying.

The posts on this blog are opinions, not advice. Please read our Disclaimers.