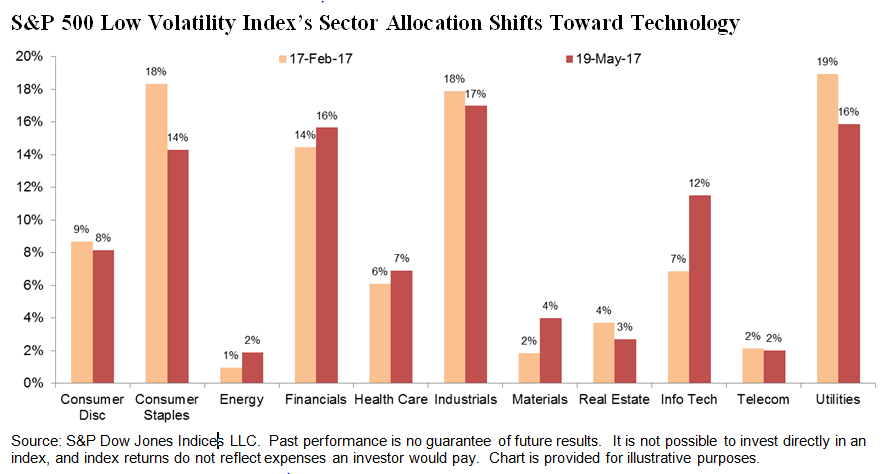

In the latest quarterly rebalance (effective at market close on May 19, 2017), the S&P 500 Low Volatility Index added more weight from the technology sector. The jump from 7% to 12% is the largest increase for any sector. Meanwhile, the index continued to shed weight in Consumer Staples and Utilities, historically the stalwarts of Low Volatility.

Notably, this composition also marks the highest weighting in Technology in the history of the S&P 500 Low Volatility Index. Since the index measures the performance of the 100 least volatile stocks in the S&P 500, it has typically had very little, if any, technology exposure.

That Low Volatility had no weight in Technology just a year ago is also noteworthy. The index’s methodology seeks out low volatility at the stock level, but we often look to the S&P 500 sectors as a loose proxy to gather insight.

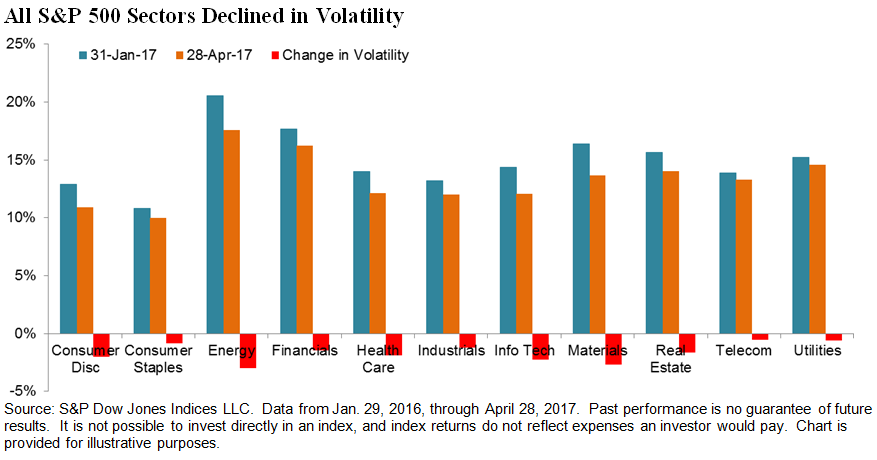

Continuing their recent trend, all 11 sectors of the S&P 500 declined in volatility as compared to three months ago. The biggest decliners were Energy, Materials, Technology and Consumer Discretionary. And since most things are relative, stocks in Consumer Staples and Utilities had to move aside to make room.