What a year 2016 was—from concerns about slowing down of the Chinese economy and a surprise vote by the UK to exit the EU to a continued trend of low-to-negative interest rates among major economies globally, demonetization in India, the shocking victory of Donald Trump in the U.S. presidential election, and finally, the U.S. Federal Reserve ending the year with a hike of 25 bps in short-term interest rates. Throughout the year, market participants kept asking “what next?”

While global markets, as measured by the S&P Global BMI, were up 8.84% for the year, if U.S. equities’ 12.61% return is excluded, the gain was 4.95%. The S&P Developed BMI and S&P Emerging BMI posted positive total returns of 8.6% and 11.30%, respectively.

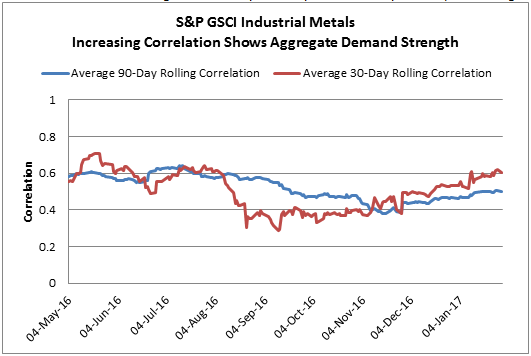

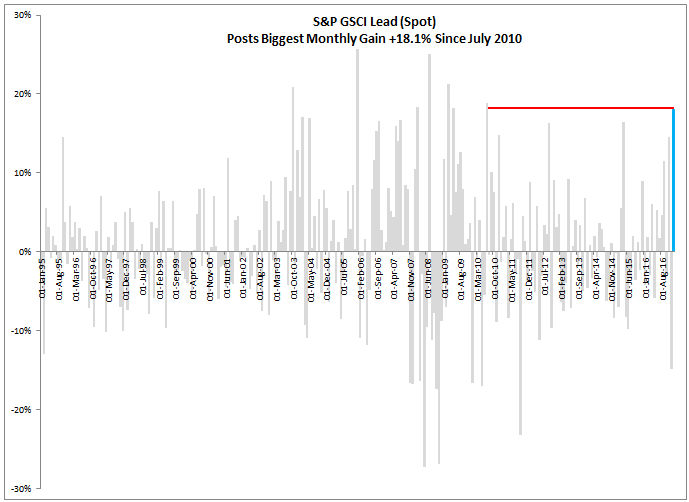

Backed by a rally in crude oil and metal prices globally, the S&P GSCI (the first major investable commodity index) gained 11.37% in 2016.

Indian Equities

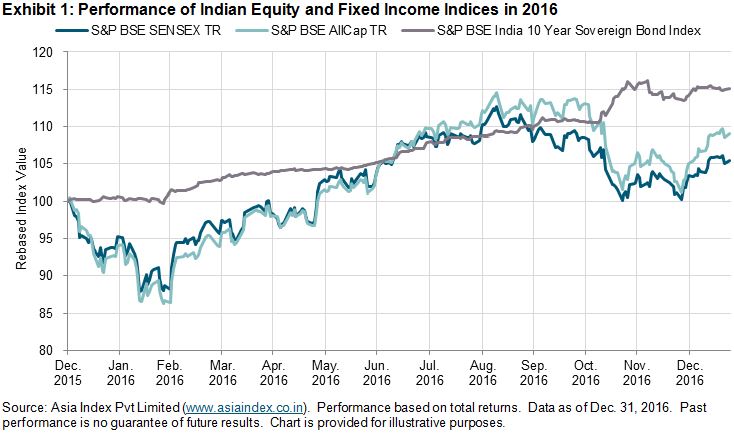

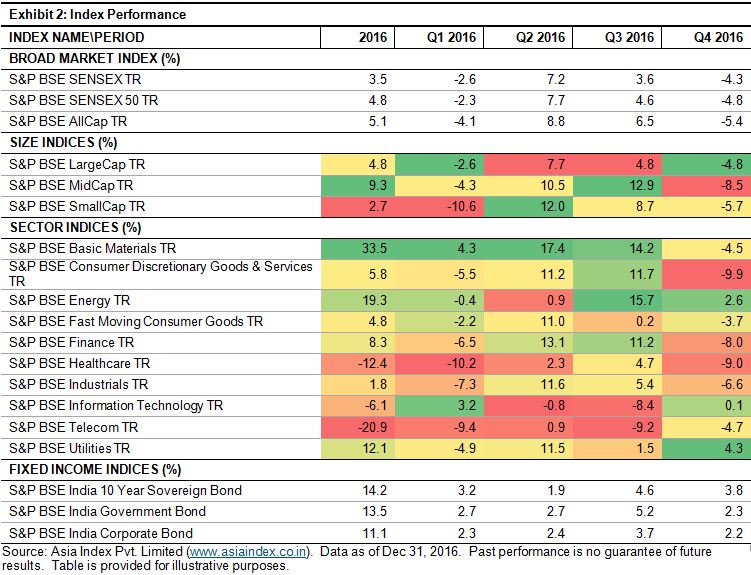

Despite various negative events, Indian equities gained in 2016. Backed by a normal monsoon, low inflation, falling key lending rates, an under-control fiscal deficit, and a relatively stable currency, India’s bellwether index, the S&P BSE SENSEX, and the S&P BSE AllCap (India’s benchmark index) ended the year with total returns of 3.5% and 5.1%, respectively. The majority of their gains for the year were achieved during the second and third quarters, as most of the key benchmark indices ended positive during those two quarters (see Exhibit 1).

The S&P BSE MidCap was the best-performing size index, with a total return of 9.3%, while the S&P BSE SmallCap continued to be worst-performing size index, with a total return of 2.7% in 2016.

Among key BSE sector indices, the S&P BSE Basic Materials posted the highest total return for the year, with 33.5%, due to increase in global commodity prices. A cash crunch caused by demonetization hurt the S&P BSE Consumer Discretionary Goods & Services the most, as during Q4 2016 it posted the worst total return of -9.9%. 2016 was one of the worst years for the S&P BSE Telecom since the financial crisis, with a total return of -20.9%.

Indian Fixed Income

Compared to calendar year 2015, Indian bond market posted higher returns in 2016 due to falling interest rates. The S&P BSE India Government Bond Index and the S&P BSE India Corporate Bond Index posted positive returns of 13.5% and 11.1%, respectively. The S&P BSE India 10 Year Sovereign Bond Index posted an impressive total return of 14.2%, outperforming the S&P BSE SENSEX by more than 10.7% in 2016.

Outlook

Among other things, market participants may want to keep an eye on the upcoming budget, the Goods and Services Tax implementation, the Reserve Bank of India’s view of future interest rate movements and inflation, global commodity prices, and the U.S. Federal Reserve’s potential decision to further increase interest rates. Although demonetization is expected to have a short-term negative impact on the GDP growth rate, it is expected to help expand the formal economy, due to a push for digitization.

The posts on this blog are opinions, not advice. Please read our Disclaimers.