Green bonds are bonds created to fund projects with positive outcomes that are directly related to the environment.

They include the following.

- “Use of proceeds” bonds and revenue bonds, which are designated for green projects.

- Green project bonds, the proceeds of which are earmarked for specific projects with positive environmental outcomes.

- Green securitized bonds, which are designated for green projects (specific or otherwise).[1]

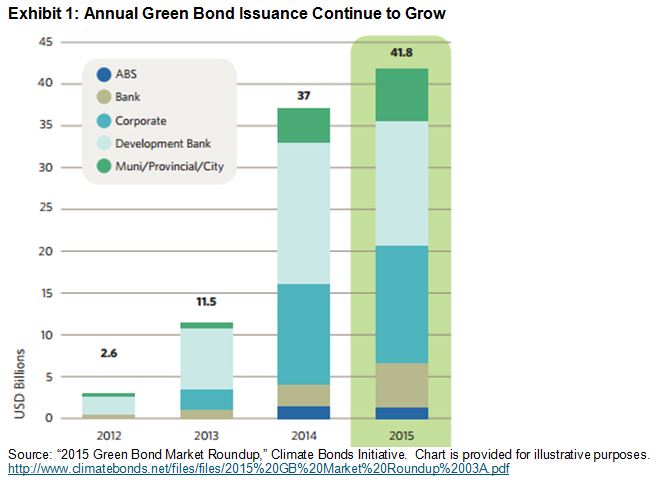

As depicted in Exhibit 1, green bond issuance has grown significantly in recent years.

Additionally, as of the end of September 2016, green bond issuances already totaled USD 50 billion—illustrating that this rapid growth shows no signs of stopping. This upward trajectory is likely due to a few key factors.

- Green bonds are relatively simple and contain traditional debt—there are no specialized cash flows and no financial engineering.

- Multiple coalitions began surrounding the green bond market in 2014, including the Green Bond Principles and three different green bond index launches (including that of S&P Dow Jones Indices). These movements helped spur the green bond market further into the spotlight and spread awareness to market participants.

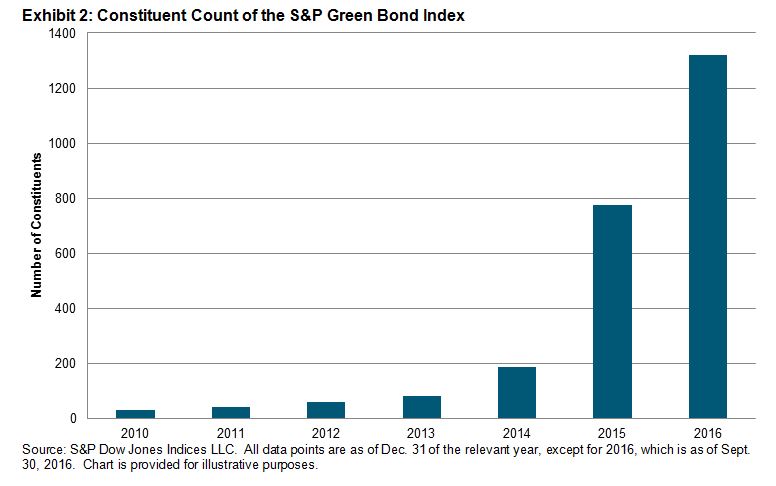

Another prime example of the growth of this market is the increasing constituent count of the S&P Green Bond Index.

The S&P Green Bond Index includes any green-labeled bond, as flagged by Reuters and the Climate Bonds Initiative (CBI), which makes it a superb indicator of the green bond marketplace.

As depicted in Exhibit 2, there were 31 bonds in the index in 2010. As of September 2016, there were 1,320.

Even with this considerable expansion, the green bond marketplace is still flawed. As with many areas of sustainable finance, it still lacks standardization. The CBI has standards in place, but they are non-binding and typically viewed in the marketplace as guidelines rather than hard-line standards.

However, we expect the green bond market to continue to grow. It’s a relatively easy way for market participants to tango with green finance—a prospect even more desirable after the COP 21 “two degree” investment initiative, the G20 Summit goals, and increasing regulations surrounding divestment.

As more and more market participants engage with green bonds, it’s reasonable to expect that regulation will come naturally, as a means to standardize a fast-growing market. After all, the first “climate awareness” bond was only launched in 2007.

[1] “Explaining Green Bonds,” Climate Bonds Initiative. https://www.climatebonds.net/market/explaining-green-bonds

The posts on this blog are opinions, not advice. Please read our Disclaimers.