The news that Berkshire Hathaway purchased a billion dollars of Apple stock sparked questions – Will S&P DJI re-classify Apple as a value stock? How are stocks divided between growth and value? Among growth and value, which is ahead year-to-date?

Currently S&P DJI classifies Apple as a growth stock. Growth-value classifications are reviewed annually in December based on a quantitative analysis of financial factors. Whether Apple’s classification is changed depends on the how the numbers add up when the next review is done.

Each stock is assigned a value score and a growth score. The value score is based on the book-to-price, earnings-to-price and sales-to-price ratios. The growth score is based on momentum over 12 months; the changes in earnings per share and the growth of sales per share, each over the last three years. Scores are normalized to make the numbers comparable. Then the stocks in the S&P 500 are ranked by the ratio of their growth score to their value score. The first third of the rankings – highest ratio of growth to value – are growth stocks, the last third – lowest ratio of growth to value – are value stocks and the middle third are apportioned between growth and value based on their scores.

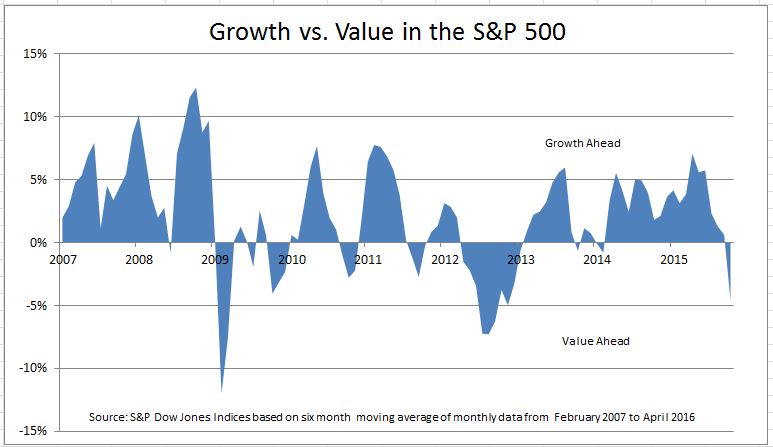

The result is the S&P 500 Growth index and the S&P 500 Value index. These can be used to tell which style lead, or lagged, during past market moves. The chart compares the performance of the growth and value indices since early 2007 when Apple announced the first iPhone. The shaded area shows the percentage change in the growth index over the last six months less the percentage change in the value index over the same six month period. Above the horizontal axis growth is winning, below the axis value is winning.

The indices also let analysts benchmark a stock against other stocks with similar characteristics. The second chart compares Apple to both the S&P 500 Growth and S&P 500 Value. The data are re-based to a common starting point of 100 in February 2007. The chart uses a logarithmic scale so that both Apple (which rose by 10 times) and the indices (which rose by a lot less) can be shown on the same page. Apple outpaced both growth and value. Of course, past performance is no guarantee of the future and whether Apple is growth or value at the next review remains to be seen.

A detailed description of the growth and value indices is in S&P U.S. Style Indices Methodology available on www.spdji.com

The posts on this blog are opinions, not advice. Please read our Disclaimers.