This morning’s Financial Times highlighted a study of market volatility suggesting that return and volatility are inversely related — that “the correct response to an increase in volatility…is to exit the market.”

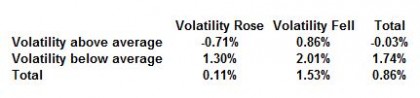

This is certainly true in the short run, as the table below confirms.

In months when the realized volatility of the S&P 500 was above average, the index’s total return was -0.03%. When volatility was below average, the index’s average return was a much-improved 1.74%. And regardless of whether realized volatility was above or below its midpoint, the S&P 500 tends to do much better when volatility is falling rather than rising.

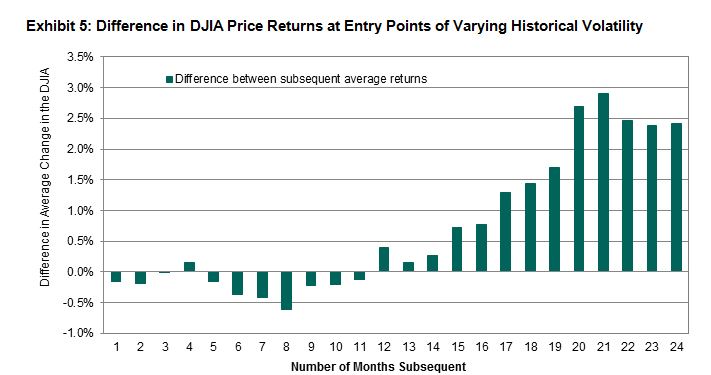

But these are very short-term — indeed, monthly — effects. What happens when we look beyond a one-month holding period? Using the history of the Dow Jones Industrial Average (which extends back to 1896), we calculated returns for holding periods of various lengths, conditioned on whether volatility was above or below the 85th percentile of the distribution. Given what we’ve already observed about the relationship between high volatility and low returns, it’s not surprising that investments made during periods of lower volatility outperform over short holding periods (up to about 11 months). After that, however, fortune favors the bold:

Source: S&P Dow Jones Indices LLC, The Landscape of Risk, 2014. Data from July 1896 to September 2012. Charts and tables are provided for illustrative purposes. Past performance is no guarantee of future results.

The British financier Nathan Mayer Rothschild is reputed to have said “Buy when there’s blood in the streets, even if the blood is your own.” The saying may be apocryphal, but the insight it embodies is real enough. One investor’s short-term risk can be the basis for another’s long-term gain.

The posts on this blog are opinions, not advice. Please read our Disclaimers.