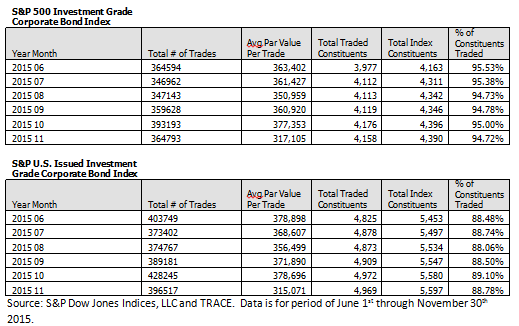

As the liquidity of recent markets have been tested by the impact of low energy prices a look at index design and results may be valuable. Focusing on investment grade corporate bonds we can see dramatic differences in depth of liquidity as a result of index design.

For investment grade corporate bonds two indices tracking these markets have very different liquidity profiles. Let’s compare the liquidity data of the bonds in the S&P 500 Investment Grade Corporate Bond Index to the broader S&P U.S. Issued Investment Grade Bond Index. The S&P 500 Investment Grade Corporate Bond Index provides a view of the performance of corporate bonds issued by the blue chip companies in the iconic S&P 500 Index, other index inclusion criteria including par amount minimums are the same as the broader corporate bond index.

Results:

- More of the bonds in the index are trading each month: During the six month period of June through November 2015 bonds in the S&P 500 Investment Grade Corporate Bond Index had a higher percentage of trading each month: approximately 95% of the bonds in this index traded each month vs. 89% of the bonds in the S&P U.S. Issued Investment Grade Bond Index. Please refer to Table 1 below for the data.

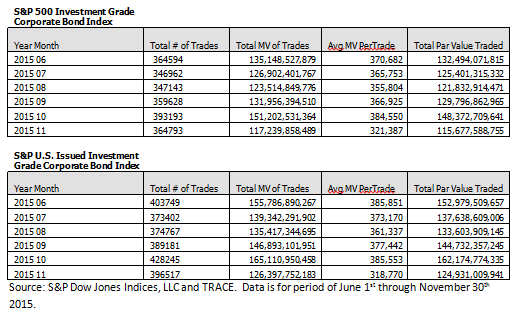

- Fewer bonds but significant representation of the bonds trading: The S&P 500 Investment Grade Corporate Bond Index has fewer bonds than the broader index but the average trade volume of bonds in the index as measured by the number of trades, market value of trades and total market value of trades represent a high percentage of the trading volume of the broader index. Please refer to Table 2 below for the data.

Table 1: Trade Volume: Average Par Value Traded, % of Constituents Traded

Table 2: Trade Volume: Market & Par Value Traded

The data illustrates that tracking the larger entities such as the blue chip companies in the S&P 500 Index results in significantly better liquidity characteristics for the underlying bonds than broader benchmarks.

The posts on this blog are opinions, not advice. Please read our Disclaimers.