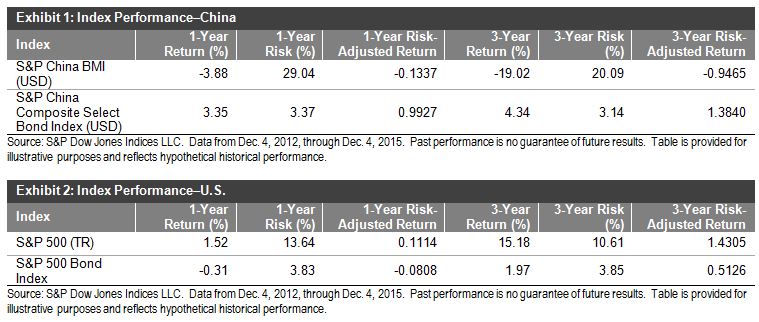

China’s onshore bond market recorded strong growth in the first 11 months of 2015 and its total return has increased 6.98% year-to-date (YTD), as measured by the S&P China Bond Index. The S&P China Composite Select Bond Index, an investable index that tracks the performance of Chinese sovereign bonds, agency bonds and bonds issued by Central State-Owned Enterprises (CSOEs) rose 7.00%; the USD index that accounted for currency fluctuation gained 3.04% in the same period.

The one-year volatilities of Chinese bonds were 2.13% in CNY and 3.38% in USD. The volatility of Chinese bonds is low when compared with the equity market; the volatility of Chinese equities over the past one- and three-year periods was more than tenfold that of Chinese bonds. Chinese bonds have consistently outperformed Chinese equities, both in terms of total return and risk-adjusted return (see Exhibit 1).

Looking at the performance of the U.S., we have similar findings. The volatility of U.S. equities over the past one- and three-year periods was approximately three times that of U.S. bonds, as tracked by the S&P 500® Bond Index. The S&P 500 Bond Index seeks to measure the performance of U.S. corporate bonds issued by constituents in the iconic S&P 500. Though the total return of U.S. bonds may be lower, the risk-adjusted returns of U.S. bonds were comparable to those of U.S. equities over the past year (see Exhibit 2).

Based on this information, we can conclude two key observations in both U.S. and Chinese markets.

- These bond markets have substantially lower volatility than their respective equity markets.

- These bond markets have historically delivered comparable, if not better, risk-adjusted returns than their respective equity markets.