Bond values will, definitionally, fall when interest rates rise. However, different types of bonds have differing characteristics.

The chart below shows the annual performance of the S&P 500 Bond Index and the S&P/BG Cantor 7-10 US Treasury Bond Index. (The S&P/BG Cantor 7-10 US Treasury Bond Index is the treasury index most similar to the S&P 500 Bond Index in duration and yield.) Notably, the performance of corporate debt and Treasuries diverged in the 2008 financial crisis and the recovery thereafter.

As between the S&P 500 Bond index and the S&P/BG Cantor 7-10 US Treasury Bond Index, the former is much more correlated to the S&P 500, 0.256 versus -0.194, respectively. This is not surprising, since corporate debt carries a higher risk than Treasuries. When crisis is such a threat that corporations’ survival is at peril then naturally debt issued by corporations will also be in danger of default.

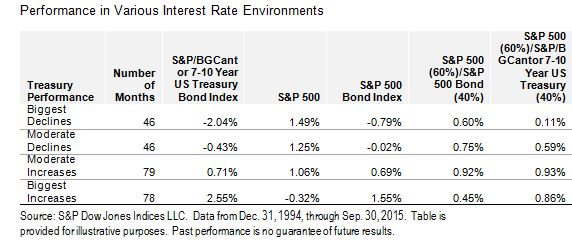

The two bond indices also had varying performance profiles in increasing and declining interest rate environments. Between 1995 and 2015, the months when Treasuries delivered their worst performance were the months when corporate bonds outperformed Treasuries by the largest spread (see table below). We divided the 249 months in this period into modified quartiles based on whether the S&P/BGCantor 7-10 Year US Treasury Bond Index was positive or negative and then further divided those months equally into the biggest and moderate changes in each direction. In the worst quartile for Treasuries, an average monthly decline of 2.04%, the S&P 500 Bond Index’s average decline was only 0.79%, an outperformance of 1.24%. In those same months, an archetypal 60/40 allocation with corporate bonds yielded outperformance of 0.49% versus one with Treasuries.

Heightened sensitivity to anticipated interest rate increases is understandable. However, the impact of interest rate changes varies with different types of bonds. Historically, when interest rates rose, their effect on corporate bonds have been muted compared to that of Treasuries. Similarly, a balanced allocation incorporating corporate bonds has offered more protection relative to Treasuries during these times.

The posts on this blog are opinions, not advice. Please read our Disclaimers.