While the S&P 500 Utilities index has been one of the weakest in the S&P 500 index in 2015, in the third quarter it was a bright spot. As global economic concerns increased, we think investors found the domestic focused, stable dividend, and earnings provided by the sector appealing. While the Federal Reserve’s possible increase in the Fed funds rate could have an adverse effect, the 10-year Treasury yield has fallen back to approximately 2.0%. The average dividend for the S&P 500 utilities sector constituent was 3.9%.

The utilities index was down 8.6% year to date through September, worse than the 6.7% for the S&P 500 index. However, in the third quarter, the sector’s 4.4% increase was a stark contrast to the 6.9% decline for the broader market.

From a profit perspective, according to Capital IQ consensus estimates, the utilities sector is expected to post earnings growth of 0.9% for the third quarter of 2015 and 1.7% for all of 2015, both ahead of the S&P 500 index that is weighed down by energy and more multinational sectors such as consumer staples. The utilities sector is projected to increase EPS/earnings 7.0% in 2016, below the 10% for the S&P 500.

The utilities sector is known for maintaining relatively high payout ratios compared with the broader market. Since earnings growth may be constrained compared with sectors that introduce new products, such as health care or information technology, utilities tend to offer investors a higher dividend due to their relatively steady cash flows, and as an incentive to buy utilities shares.

According to S&P Capital IQ Equity Analyst Christopher Muir, payout ratios for the utilities sector have been higher than the S&P 1500. The five-year average payout ratio of 69.0% for the sector is more than double that of the S&P 1500.

Muir foresees continued high levels of capital spending by the industry, both on regulated and unregulated investments. Regulated capital spending includes spending on infrastructure replacement, new transmission and distribution facilities and lines, and regulated power plants, including new nuclear units currently under construction.

Unregulated spending will mostly focus on new natural gas-fired combined-cycle power plants, and investment in solar and wind generation is also likely.

While investors pulled money out of utilities sector ETFs in the first half of 2015, the sector had the second most inflows during the third quarter, behind energy. There are eight U.S. utility sector ETFs, though their exposures are distinct.

—————————————————————————————————–

S&P Capital IQ operates independently from S&P Dow Jones Indices.

The views and opinions of any contributor not an employee of S&P Dow Jones Indices are his/her own and do not necessarily represent the views or opinions of S&P Dow Jones Indices or any of its affiliates. Information from third party contributors is presented as provided and has not been edited. S&P Dow Jones Indices LLC and its affiliates make no representations or warranties of any kind, express or implied, regarding the completeness, accuracy, reliability, suitability or availability of such information, including any products and services described herein, for any purpose.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

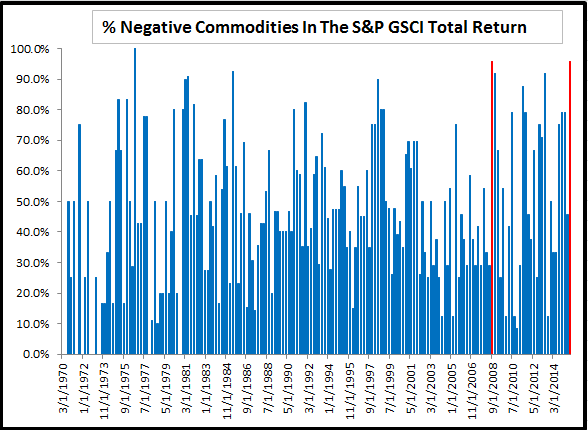

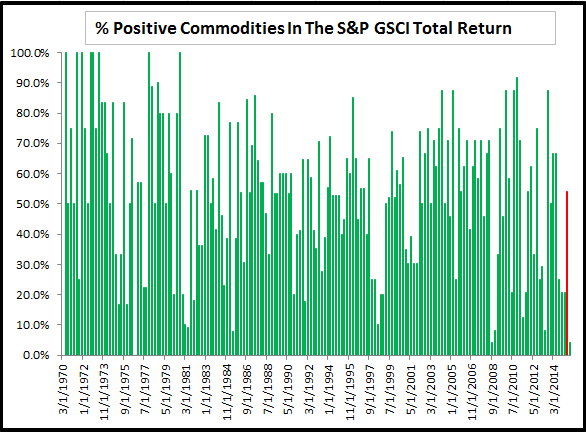

Source: S&P Dow Jones Indices

Source: S&P Dow Jones Indices Source: S&P Dow Jones Indices

Source: S&P Dow Jones Indices