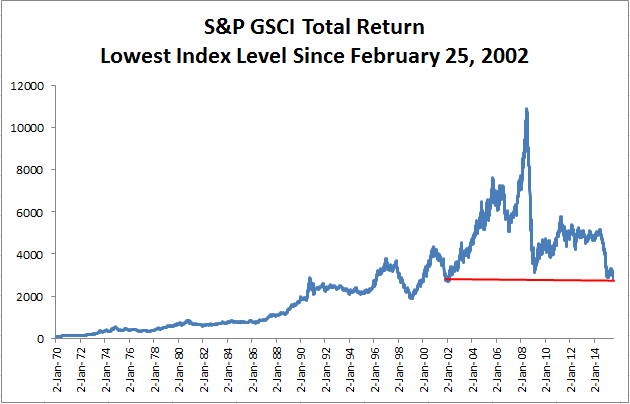

The S&P GSCI has lost 13.6% month-to-date through July 27, 2015, bringing its level to the lowest since February 25, 2002. It has now exceeded the bottom of the 2008 global financial crisis. Please see the chart below:

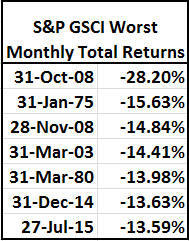

Thus far, July 2015 is the seventh worst performing month in the history of the S&P GSCI that goes back to January 1970. It is one of the worst months in more than 45 years or 547 months. Please see the table below for the six months that fared worse:

Every single one of the 24 commodities is negative for the month except lean hogs, which is just barely positive by 18 basis points BUT only when taking into account the positive roll yield; otherwise that is negative too, by 14.5%. Throughout the history of the index, 23 commodities have been negative together in a month only once in September 2008 and all 24 were negative together only once in the following month of October 2008. The single performer in September 2008 was gold, clearly different from today.

If the index were to fall back to the bottom before 2002, that happened on December 21, 1998, it has another 32% to fall. As the Wall Street Journal points out in this article, global growth is a major concern.

The posts on this blog are opinions, not advice. Please read our Disclaimers.