This is the second in a series of blog posts relating to the in depth analysis of performance differential between the S&P SmallCap 600 and the Russell 2000.

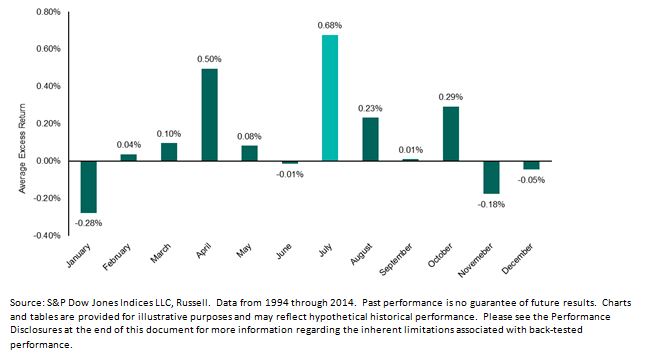

Numerous studies have been conducted on Russell’s annual reconstitution process in June, particularly regarding the downward price pressure placed on the Russell 2000. As winners from the Russell 2000 move up to the Russell 1000, and losers from the Russell 1000 move down to the small-cap index, small-cap fund managers are forced to sell winners and buy losers, thereby creating negative momentum.

To study this effect, we examine the average monthly excess returns for each calendar month from 1994 through 2014. It is seen that the S&P SmallCap 600 has an average monthly excess return of +0.68% for the month of July vs. the Russell 2000, with a statistically significant t-stat of 2.54. These results indicate that there may be a strong relationship between the Russell 2000 annual rebalancing in June and the negative excess returns in the following month.

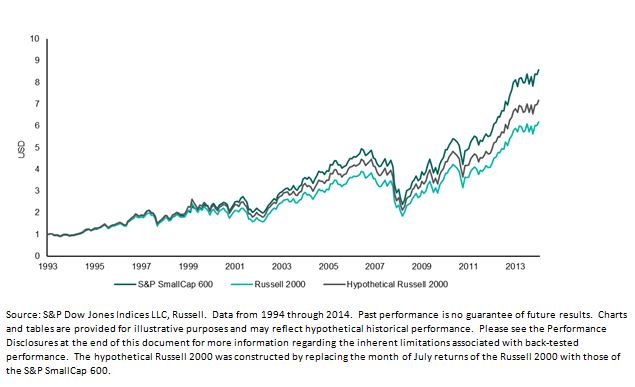

In an attempt to control for the July reconstitution effect, a hypothetical index was created where the monthly returns are represented by the Russell 2000, with the exception of July being represented by the S&P SmallCap 600. From 1994 through 2014, the difference in an investment of USD 1.00 into each the Russell 2000 and the S&P SmallCap 600 amounts to USD 2.41 (USD 6.18 and USD 8.59 respectively). The same investment in the hypothetical index results in USD 7.17, USD 1.42 lower than the S&P SmallCap 600. Therefore, only a portion of the excess returns may be attributed to the July reconstitution effect, with the rest of the difference coming from other factors.