From the end of 2013 there has been a 10.2% increase in the number of issues paying a dividend in the S&P SmallCap 600. Initiating a dividend represents a broad commitment of future earnings, to which companies need to be very sure of their future cash-flow. On an index market-size level, SmallCap yields remains at the lower end of the spectrum, as the traditional growth characteristics (and priority) plays out more than the income component. However, comparisons on an issue level within the size classifications show a much closer relationship of yields, with size not being a significant differentiator. Starting with recent growth in SmallCap payers, and the history of payers to continue to pay and increase, SmallCaps issues appear to be trending up, and if the trend continues, eventually, the index level characterizes will change.

S&P SmallCap600 dividend stats:

- 324 of the 600 pay a regular cash dividends

- The weighted index yield is 1.34%, with the 324 payers yielding 2.24%

- The average market value is $1.24 billion, with the average market value of dividend payers being $1.37 billion

- 182 payers have a dividend rate less than 50% of their 12 month net GAAP income, with 235 being less than 75%

- 18 issues have increased their cash dividend payment for at least 20 consecutive years, with 19 more increasing it for at least 10 years

- 176 have paid cash dividends for at least 10 consecutive years, with 231 paying for at least 5 consecutive years

- Based on the current dividend rate, 202 issues will pay more than they paid in 2014; 255 paid more in 2014 than 2013 and 139 paid more in 2013 than 2012

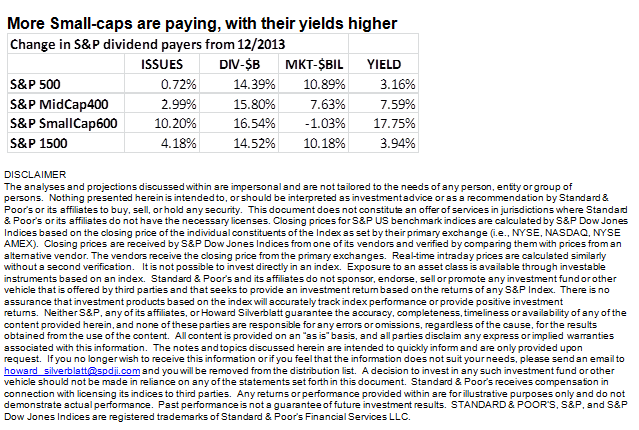

More Small-caps are paying, with their yields higher

Four SmallCaps in the S&P High Yield Dividend Aristocrats

SmallCaps have underperformed, which also has helped yields

The posts on this blog are opinions, not advice. Please read our Disclaimers.

{kind=link}