Ever since the launch of the first ethical investment fund by Friends Provident in 1984, socially responsible investing has continued to grow. Global assets under management reached EUR 13.6 trillion in 2012, and mutual fund assets in Europe increased by 19% over just two years, from EUR 199.9 billion in 2010 to EUR 237.9 billion in 2012.

The increasing popularity of sustainability investing can be ascribed to the fact that investors are increasingly aware of the impact of their actions on their surrounding environment and also to the findings of recent academic research which showed that socially responsible companies tend to outperform on a variety of financial metrics in the long term. For instance, Statman (2005) concluded that returns of socially responsible indices were generally higher than those of the S&P 500®. More recent research, written by Eccles et al. (2011), showed that high-sustainability firms dramatically outperformed low-sustainability firms in terms of both the stock market and accounting measures.

Dow Jones Sustainability Indices: An Overview

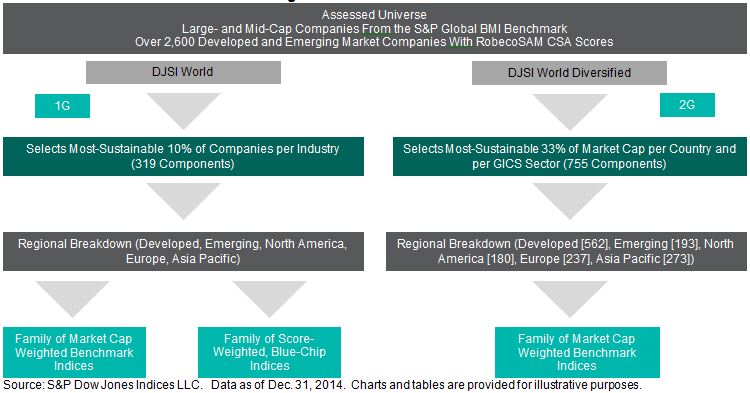

Launched in 1999, the Dow Jones Sustainability™ World Index (the DJSI World) was the first global sustainability index and is highly recognized within the investment community. One of the reasons why the DJSI series has gained widespread acceptance among practitioners lies in the reliability of the analytical inputs used to construct the index. These inputs are provided by RobecoSAM, a renowned investment specialist focused exclusively on sustainability investing. In addition to the DJSI, S&P Dow Jones Indices and RobecoSAM have developed the Dow Jones Sustainability Diversified Indices, which have a broader universe and a lower tracking error to the benchmarks.

S&P Carbon Efficient Indices

S&P Dow Jones Indices has also developed a series of carbon-efficient indices to address investor desire to support environmentally friendly companies and reduce carbon-related risks. The S&P Carbon Efficient Indices select the companies with the least carbon footprint per unit sales of each of the companies within the universe, based on the data compiled by Trucost, an independent specialist research provider.

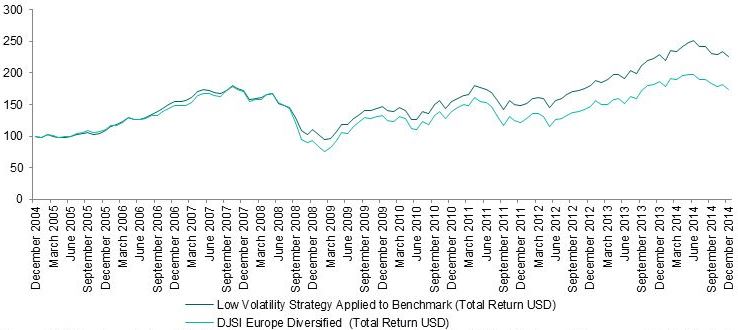

Case Study: Applying Strategies to Sustainability Indices

This case study examines whether low volatility strategies may apply to sustainability benchmarks and we have created a simulation that involves selecting the 100 least-volatile stocks from the DJSI Europe Diversified Index every 6 months. The results show that, compared to the benchmark, the annualised excess performance of the strategy is 2.8%, with a corresponding decrease in volatility of 17.5%. This suggests that traditional equity strategies may apply equally well to a sustainability benchmark as to a traditional benchmark.

For more information about this, please read.

The posts on this blog are opinions, not advice. Please read our Disclaimers.