Worried that maybe you missed the possible bottom of commodities after the S&P GSCI Total Return lost 7.5% in January, posting its sixth worst January in history since 1970? It’s possible there is still time even after the S&P GSCI TR posted (on Feb. 3, 2015) not only the 35th best day, up 4.13%, in its history since Jan. 6, 1970 (11,370 days ago), but the index posted a 3-day gain of 10.03%. This is only the 5th time in history the index has posted a 3-day gain over 10%.

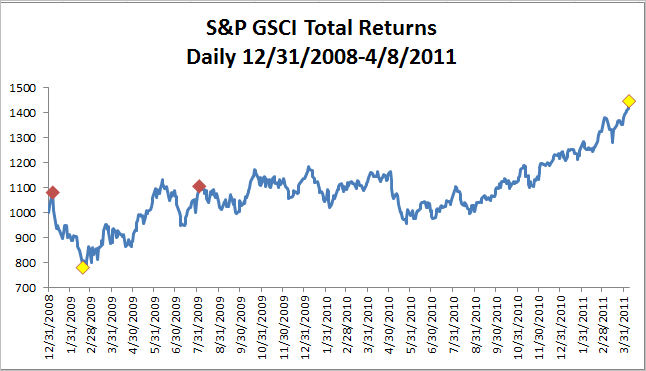

August 3, 2009 ended the last 3-day period the index gained over 10%, up 10.64%. Also in 2009, January 5th ended the largest 3-day gain of 14.31%. The chart below shows return following these spikes. Notice there was a 26.7% drop from Jan. 5 to Feb.18 of 2009 before a 41.7% gain through Aug. 3 of that year. The S&P GSCI TR continued to increase 30.8% until its peak on April 8, 2011.

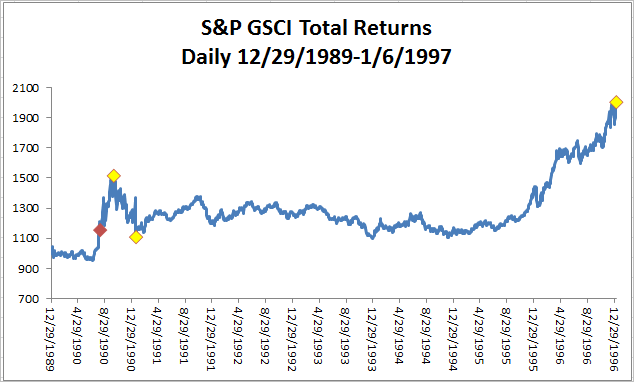

The other two 3-day periods the index gained more than 10% ended on August 6th and 7th in 1990, posting returns of 13.65% and 10.83%, respectively. Notice after this period, the index peaked on Oct. 9, 1990 gaining an additional 25.2% after the historically big 3-day rise. Subsequently it fell 26.8% through Jan. 18, 1991 before rising 80.7% through Jan. 6, 1997.

The posts on this blog are opinions, not advice. Please read our Disclaimers.