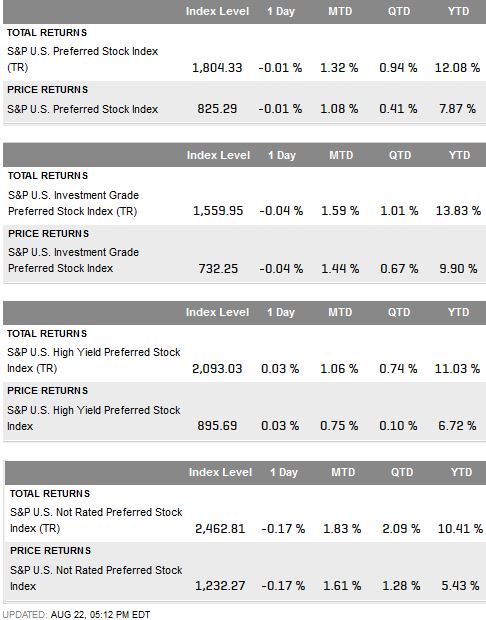

In August the yield of the S&P/BGCantor Current 10 Year U.S. Treasury Index dropped by 23 basis points from 2.56% to 2.33% where it closed out the month. Holding the 10-year alone returned 2.19% for the month and has returned 8.42% year-to-date on a total rate of return basis.

TIPS or Treasury Inflation Protection Securities also have performed well year-to-date. The S&P 10 Year U.S. TIPS Index has returned 8.69% year-to-date. The performance of the 10-year TIP was slow in June and July, but picked up in August returning 0.61%.

U.S. investment grade corporate bonds as measured by the S&P U.S. Issued Investment Grade Corporate Bond Index returned 1.38% in August and have returned 7.05% year-to-date. The pace of return is similar to 2012 when the index returned 8.86%. When comparing the rating segments of the index, AAA bonds returned 1.70% for the month, the same return as BB bonds. These bonds have returned 8.01% year-to-date.

The S&P U.S. Issued High Yield Corporate Bond Index had a strong August returning 1.47% for the month. August’s return makes up for the -1.31% performance in July and is second to the February rally of 1.92% though not enough to outpace investment grade year-to-date.