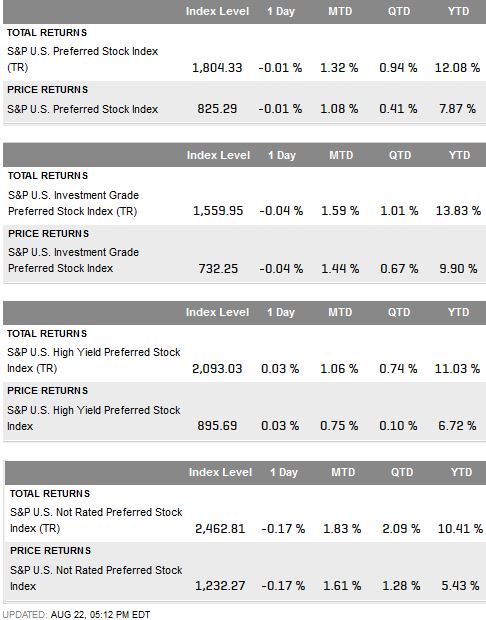

Preferred securities as measured by the S&P U.S. Preferred Stock Index have returned 12.08% year-to-date. The performance of this index has outpaced both the S&P U.S. Issued Investment Grade Corporate Bond Index (6.49%YTD) and the S&P U.S. Issued High Yield Corporate Bond Index (5.5% YTD).

The recent development of three new sub-indices to the S&P U.S. Preferred Stock Index breaks out this index by credit rating. Separating the index by the lowest of the three rating agencies creates the sub-indices of S&P U.S. Investment Grade Preferred Stock Index, S&P U.S. High Yield Preferred Stock Index and the S&P U.S. Not Rated Preferred Stock Index. High yield represents 54% of the parent index while investment grade issuers are 38% and non-rated issuers are 8% by market weight. Though all three sub-indices are performing well, the investment grade index is in the lead with a total return of 1.59% MTD and 13.83% YTD.

Source: S&P Dow Jones Indices, data as of 8/22/2014

The posts on this blog are opinions, not advice. Please read our Disclaimers.