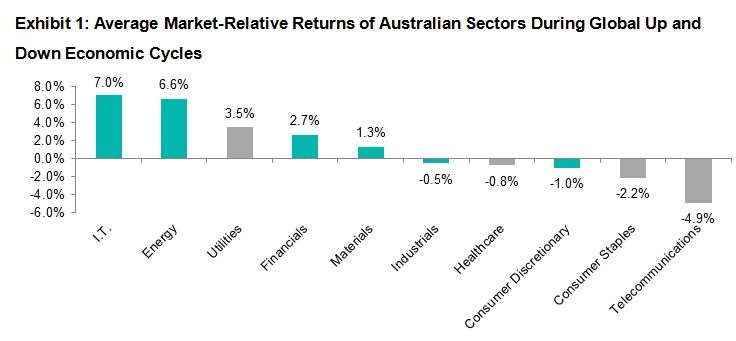

Rotating between cyclical and defensive stocks across economic cycles is a common approach for investors to take advantage of different economic phases. Energy, materials, industrials, consumer discretionary, financials and information technology are traditionally considered cyclical sectors, as stocks in these sectors have tended to be highly correlated to economic cycles. In contrast, consumer staples, healthcare, telecom and utilities are generally thought to be defensive sectors, as their profits and prices have had very low correlation to economic activity.

In our study of Australian equity, we observed that Australian sectors demonstrated much stronger cyclical and defensive characteristics across the global economic cycles when compared with domestic economic cycles. Cyclical sectors broadly outperformed defensive sectors during global economic up cycles, and they underperformed defensive sectors when the global economy slowed. This suggests that the global economy could more strongly influence relative performance between these two types of sectors than the domestic Australian economy can.

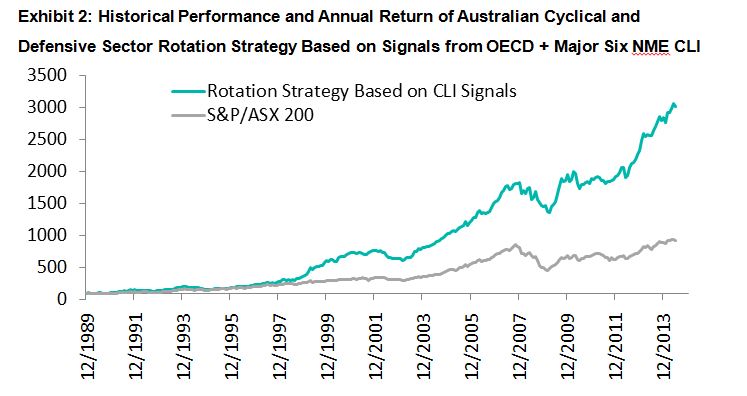

Source: S&P Dow Jones Indices LLC. Sectors highlighted in teal and gray represent cyclical and defensive sectors, respectively. Data from December 1989 to June 2014. Data are based on the S&P/ASX 200 universe (between March 31, 2000, and June 2014) and the S&P Australia BMI universe (prior to March 31, 2000). Global economic up and down cycles are defined by monthly change of the OECD + Major Six NME CLI. Performance of cyclical sectors and defensive sectors is equal-weighted, and stocks within each sector are market cap-weighted. Performance is based on total return in AUD. Charts and tables are provided for illustrative purposes. Past performance is no guarantee of future results.

In Australia, cyclical sectors represent 80% of the total market, based on the S&P/ASX 200. However, cyclical sectors underperformed defensive sectors on average over the entire period between December 1989 and June 2014. They only outperformed defensive sectors on average in seven of the past 24 years. These results suggest that mimicking benchmark sector weighting may not be the most optimal way to maximize portfolio returns.

To exploit the cyclical and defensive nature of Australian sectors, we examined a strategy that alternately invested in cyclical and defensive sectors during global economic up and down cycles, based on the monthly change of the OECD global leading economic indicator. Results showed this simple strategy was profitable over the past two decades with an absolute annualized return of almost 15%, outperforming the benchmark by 5.4% per annum. As 80% of the Australian equity market is dominated by cyclical sectors, outperformance of this rotation strategy was mainly driven by turning to defensive sectors during global economic downturn.